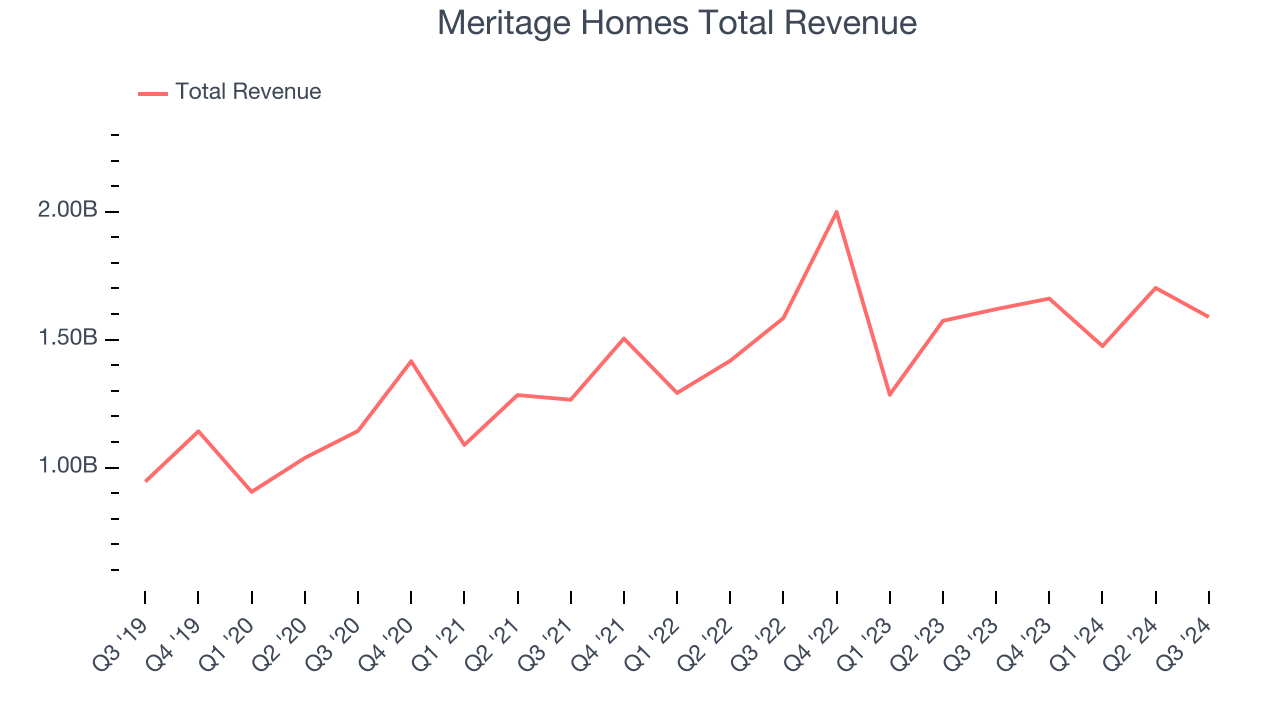

Homebuilder Meritage Homes (NYSE: MTH) met Wall Street’s revenue expectations in Q3 CY2024, but sales fell 1.9% year on year to $1.59 billion. On the other hand, next quarter’s revenue guidance of $1.55 million was less impressive, coming in 99.9% below analysts’ estimates. Its non-GAAP profit of $5.34 per share was 7.2% above analysts’ consensus estimates.

Is now the time to buy Meritage Homes? Find out by accessing our full research report, it’s free.

Meritage Homes (MTH) Q3 CY2024 Highlights:

- Revenue: $1.59 billion vs analyst estimates of $1.59 billion (in line)

- Adjusted EPS: $5.34 vs analyst estimates of $4.98 (7.2% beat)

- Revenue Guidance for Q4 CY2024 is $1.55 million at the midpoint, below analyst estimates of $1.58 billion

- Adjusted EPS guidance for Q4 CY2024 is $4.35 at the midpoint, below analyst estimates of $4.71

- Gross Margin (GAAP): 175%, up from 26.9% in the same quarter last year

- Free Cash Flow was -$100 million, down from $94.23 million in the same quarter last year

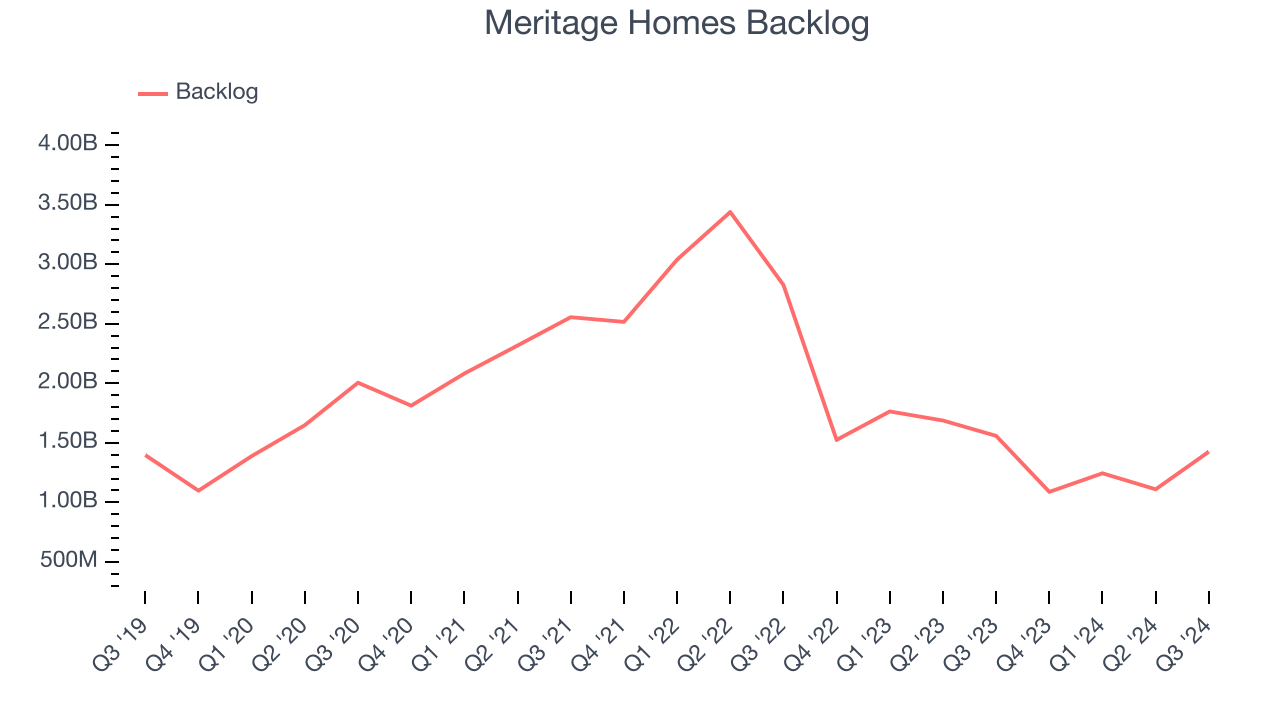

- Backlog: $1.43 billion at quarter end, down 8.5% year on year

- Market Capitalization: $6.70 billion

"Our solid third quarter 2024 results reflected the pivot in our strategy to affordable, quick-turning move-in ready homes, which generated $1.6 billion of home closing revenue and our highest third quarter closing volume," said Steven J. Hilton, executive chairman of Meritage Homes.

Company Overview

Originally founded in 1985 in Arizona as Monterey Homes, Meritage Homes (NYSE: MTH) is a homebuilder specializing in designing and constructing energy-efficient and single-family homes in the US.

Home Builders

Traditionally, homebuilders have built competitive advantages with economies of scale that lead to advantaged purchasing and brand recognition among consumers. Aesthetic trends have always been important in the space, but more recently, energy efficiency and conservation are driving innovation. However, these companies are still at the whim of the macro, specifically interest rates that heavily impact new and existing home sales. In fact, homebuilders are one of the most cyclical subsectors within industrials.

Sales Growth

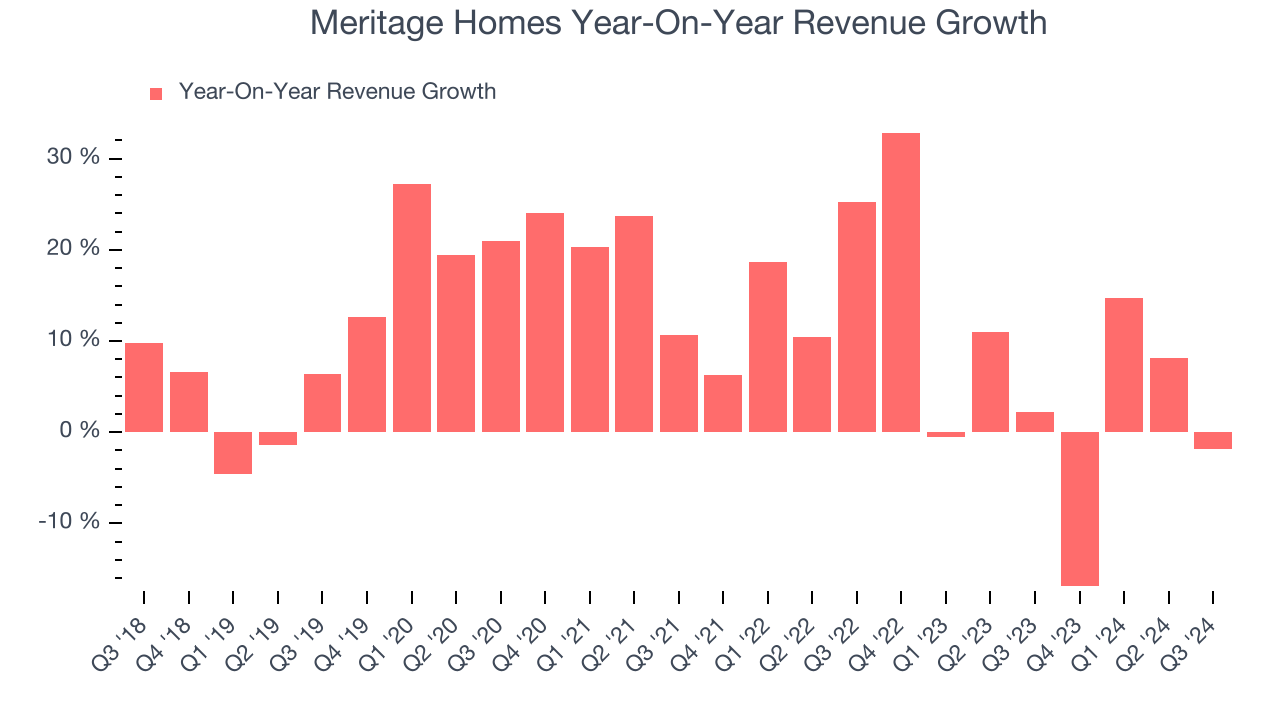

A company’s long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Luckily, Meritage Homes’s sales grew at an excellent 12.7% compounded annual growth rate over the last five years. This is a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Meritage Homes’s recent history shows its demand slowed significantly as its annualized revenue growth of 5.3% over the last two years is well below its five-year trend.

Meritage Homes also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Meritage Homes’s backlog reached $1.43 billion in the latest quarter and averaged 34.8% year-on-year declines over the last two years. Because this number is lower than its revenue growth, we can see the company hasn’t secured enough new orders to maintain its growth rate in the future.

This quarter, Meritage Homes reported a rather uninspiring 1.9% year-on-year revenue decline to $1.59 billion of revenue, in line with Wall Street’s estimates. Management is currently guiding for a 99.9% year-on-year decline next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates the market believes its products and services will face some demand challenges.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

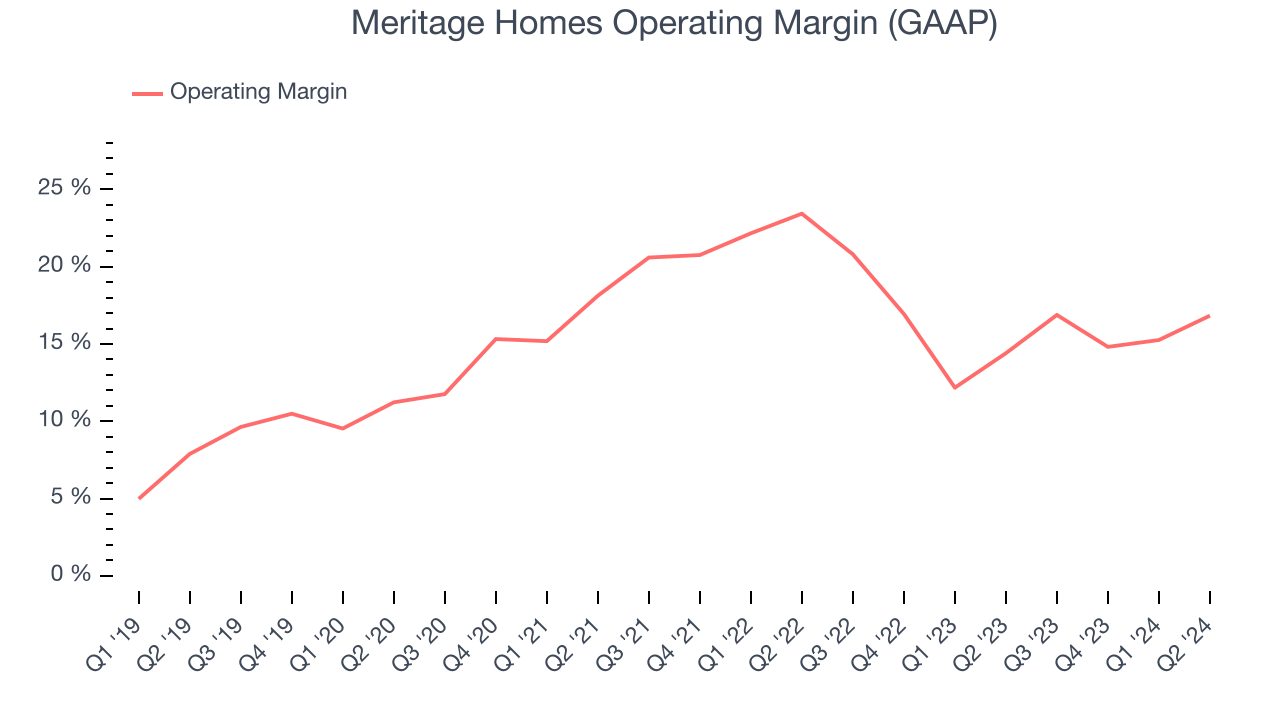

Meritage Homes has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 16.5%. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Meritage Homes’s annual operating margin rose by 5.2 percentage points over the last five years, as its sales growth gave it immense operating leverage.

Earnings Per Share

Analyzing revenue trends tells us about a company’s historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

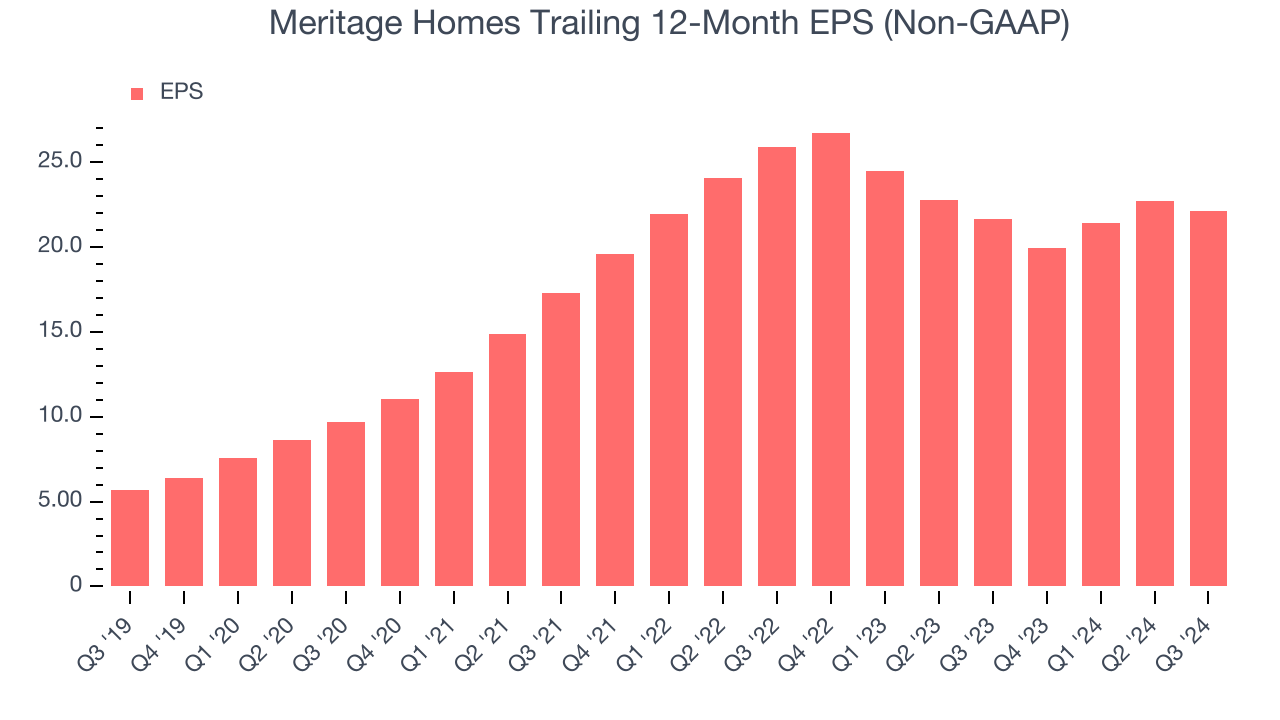

Meritage Homes’s EPS grew at an astounding 31.3% compounded annual growth rate over the last five years, higher than its 12.7% annualized revenue growth. This tells us the company became more profitable as it expanded.

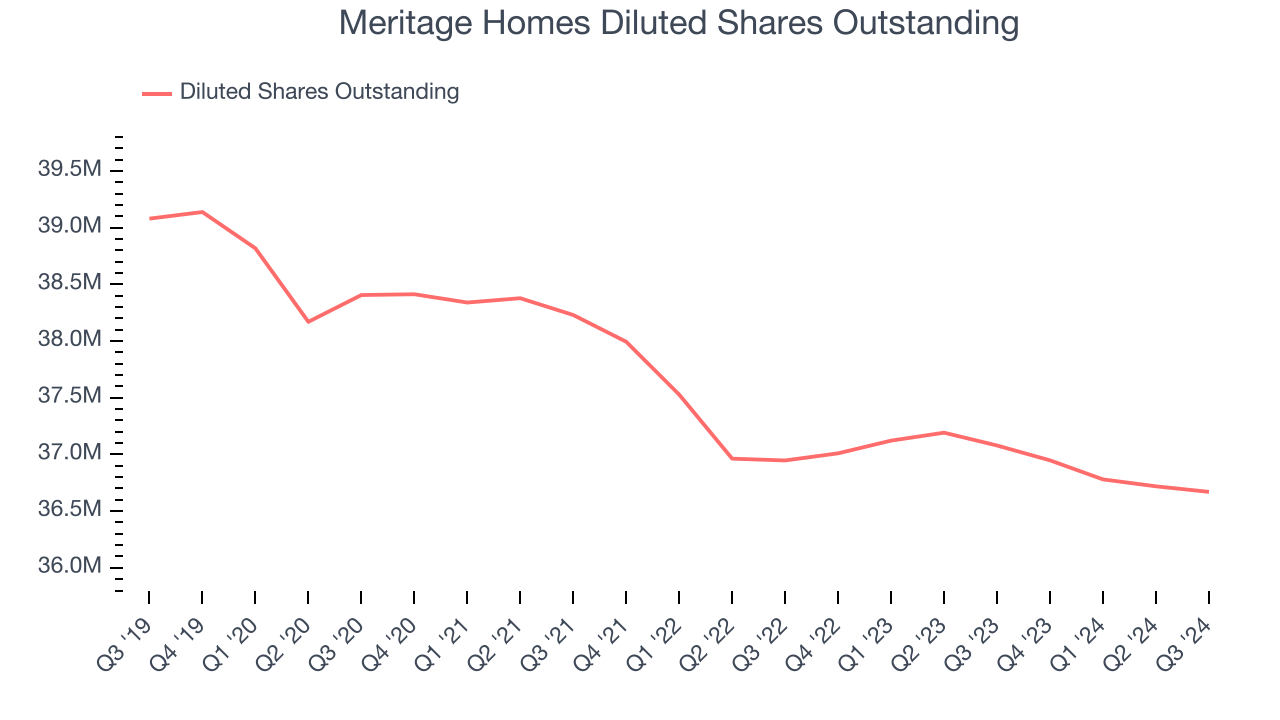

We can take a deeper look into Meritage Homes’s earnings to better understand the drivers of its performance. As we mentioned earlier, Meritage Homes’s operating margin expanded by 5.2 percentage points over the last five years. On top of that, its share count shrank by 6.2%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Meritage Homes, its two-year annual EPS declines of 7.6% mark a reversal from its (seemingly) healthy five-year trend. We hope Meritage Homes can return to earnings growth in the future.In Q3, Meritage Homes reported EPS at $5.34, down from $5.98 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 7.2%. Over the next 12 months, Wall Street expects Meritage Homes’s full-year EPS of $22.10 to shrink by 7.2%.

Key Takeaways from Meritage Homes’s Q3 Results

We were impressed by how significantly Meritage Homes blew past analysts’ backlog expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed and its EPS guidance for next quarter fell short of Wall Street’s estimates. Zooming out, we think this was a decent quarter featuring some areas of strength, but the outlook is weighing on shares. The stock traded down 1.9% to $177.12 immediately following the results.

Should you buy the stock or not?We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.