Over the past six months, AutoZone’s stock price fell to $3,470. Shareholders have lost 6.1% of their capital, which is disappointing considering the S&P 500 has climbed by 11.5%. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Given the weaker price action, is now the time to buy AZO? Find out in our full research report, it’s free.

Why Are We Positive On AutoZone?

Aiming to be a one-stop shop for the DIY customer, AutoZone (NYSE: AZO) is an auto parts and accessories retailer that sells everything from car batteries to windshield wiper fluid to brake pads.

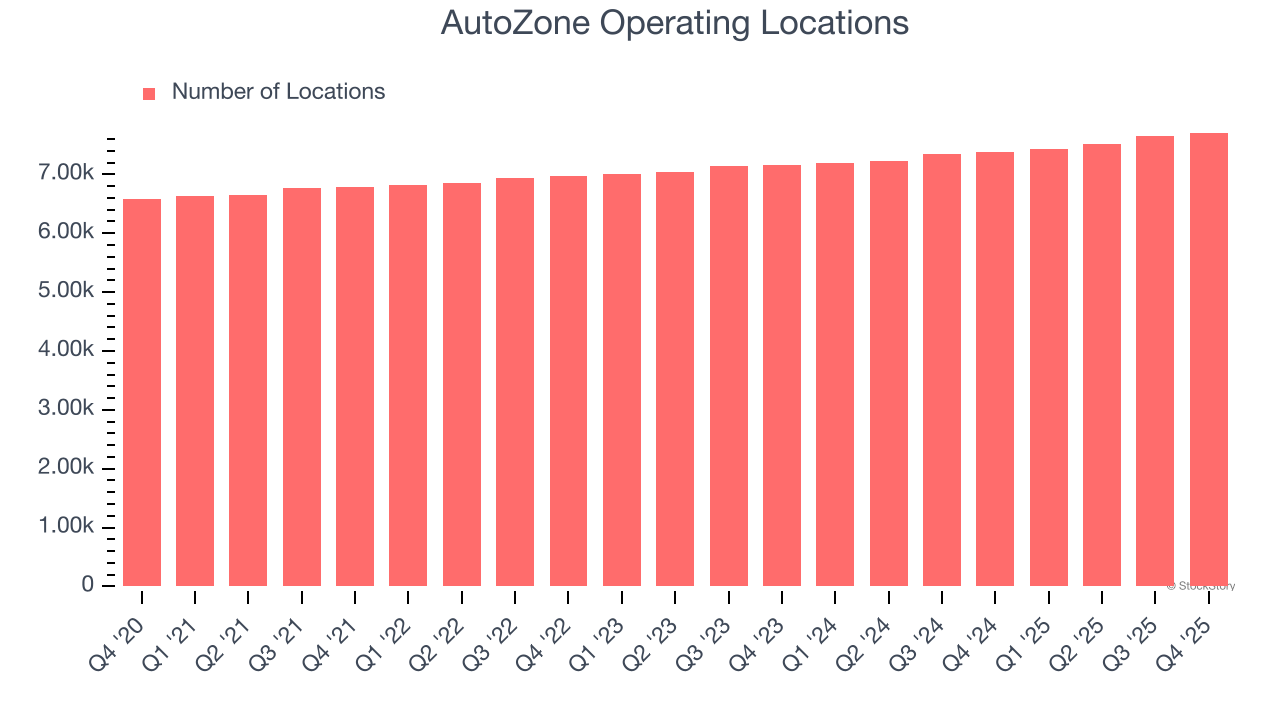

1. New Stores Popping Up Gradually, Supports Growth

A retailer’s store count often determines how much revenue it can generate.

AutoZone sported 7,710 locations in the latest quarter. Over the last two years, it has opened new stores quickly, averaging 3.4% annual growth. This was faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

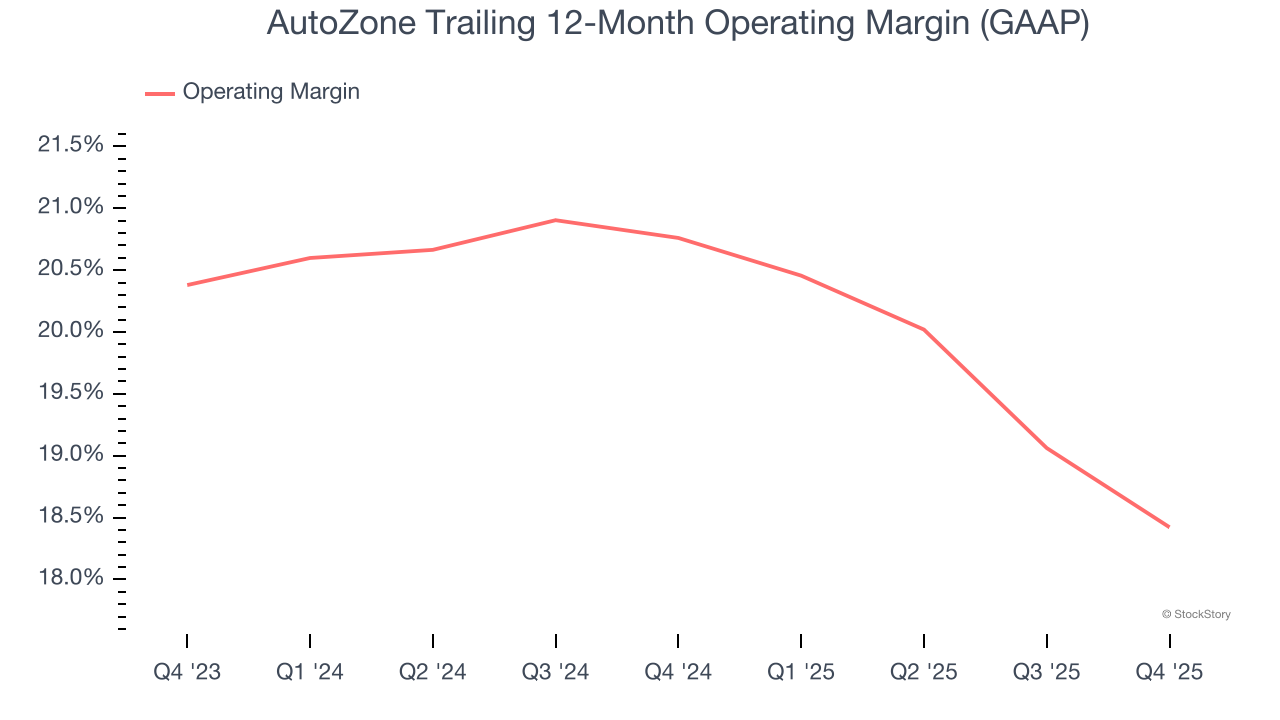

2. Operating Margin Reveals a Well-Run Organization

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

AutoZone has been a well-oiled machine over the last two years. It demonstrated elite profitability for a consumer retail business, boasting an average operating margin of 19.6%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

3. Stellar ROIC Showcases Lucrative Growth Opportunities

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

AutoZone’s five-year average ROIC was 40.4%, placing it among the best consumer retail companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

Final Judgment

These are just a few reasons AutoZone is a rock-solid business worth owning. After the recent drawdown, the stock trades at 22.6× forward P/E (or $3,470 per share). Is now a good time to initiate a position? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than AutoZone

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.