Over the last six months, Freshpet’s shares have sunk to $63.74, producing a disappointing 6.1% loss - a stark contrast to the S&P 500’s 13.3% gain. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Freshpet, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free for active Edge members.

Why Is Freshpet Not Exciting?

Even with the cheaper entry price, we're swiping left on Freshpet for now. Here are three reasons there are better opportunities than FRPT and a stock we'd rather own.

1. Fewer Distribution Channels Limit its Ceiling

With $1.08 billion in revenue over the past 12 months, Freshpet is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

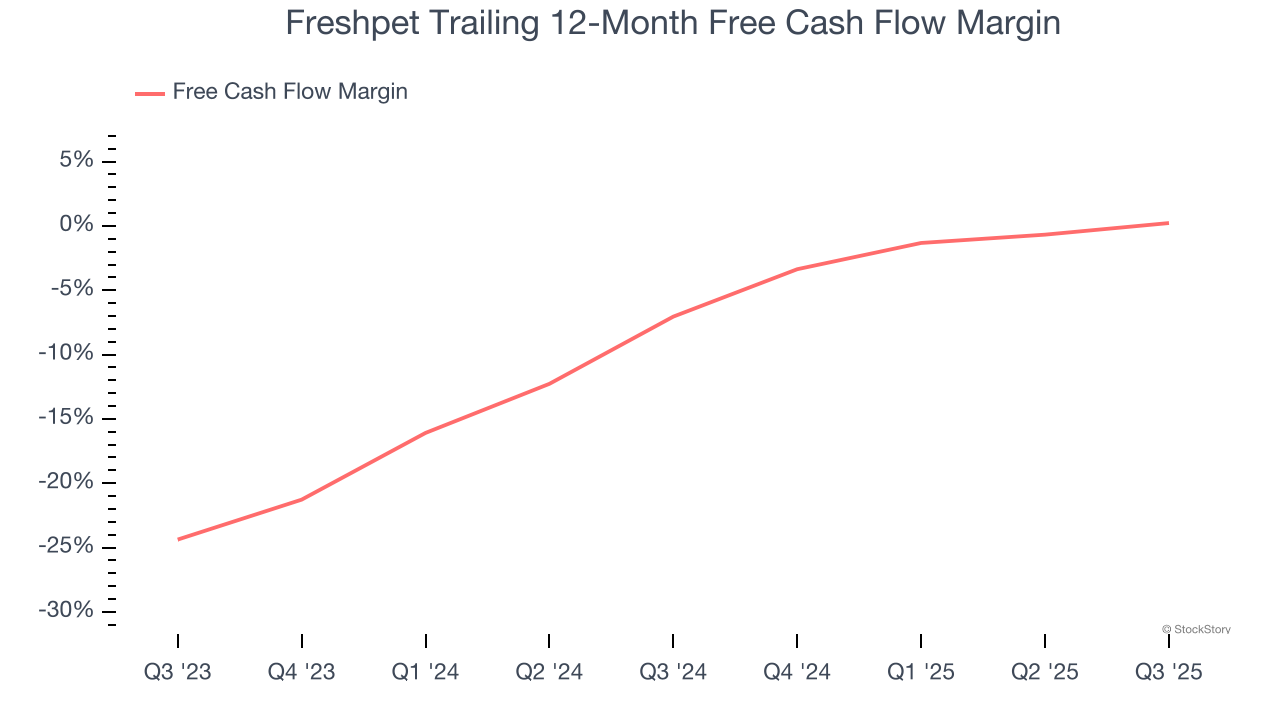

2. Cash Burn Ignites Concerns

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

While Freshpet posted positive free cash flow this quarter, the broader story hasn’t been so clean. Freshpet’s demanding reinvestments have consumed many resources over the last two years, contributing to an average free cash flow margin of negative 3.1%. This means it lit $3.14 of cash on fire for every $100 in revenue.

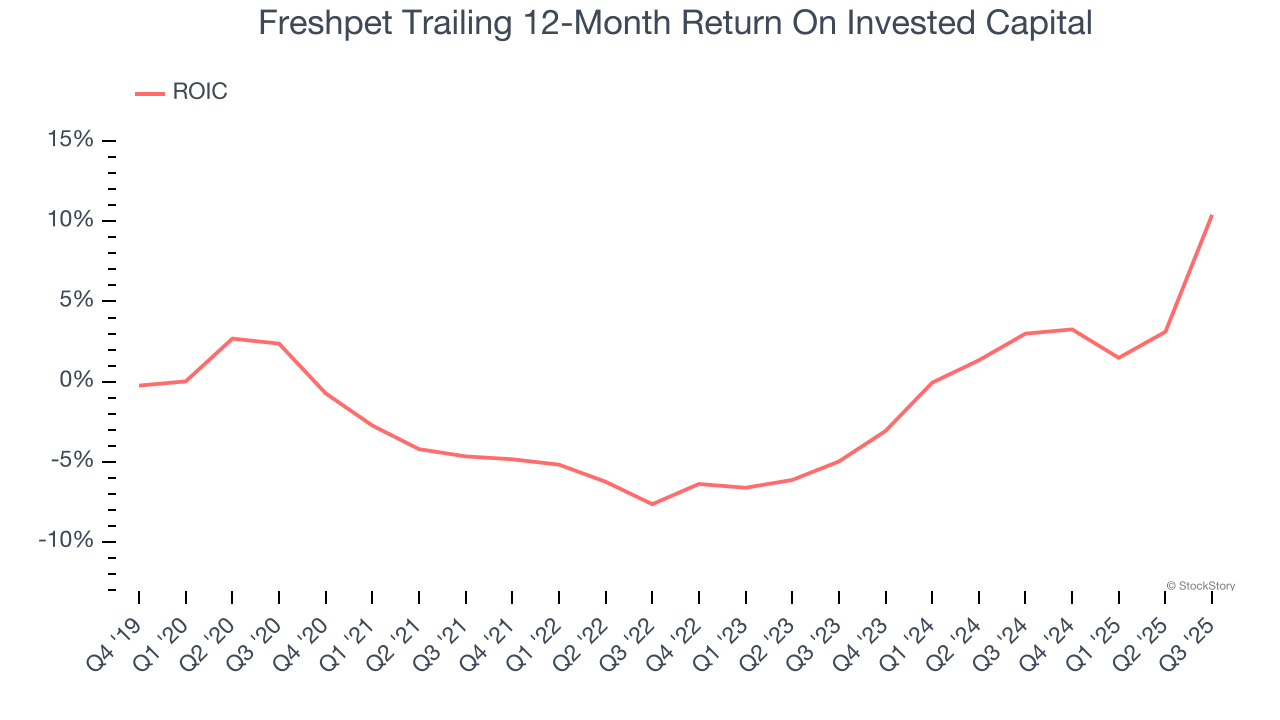

3. Previous Growth Initiatives Haven’t Paid Off Yet

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Freshpet’s five-year average ROIC was negative 0.8%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer staples sector.

Final Judgment

Freshpet’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 44.4× forward P/E (or $63.74 per share). This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

Stocks We Would Buy Instead of Freshpet

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.