HCA Healthcare has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 25.2% to $419.60 per share while the index has gained 25.5%.

Is now a good time to buy HCA? Find out in our full research report, it’s free for active Edge members.

Why Are We Positive On HCA?

With roots dating back to 1968 and a network spanning 20 states, HCA Healthcare (NYSE: HCA) operates a network of 190 hospitals and 150+ outpatient facilities providing a full range of medical services across the US and England.

1. Economies of Scale Give It Negotiating Leverage with Suppliers

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $72.7 billion in revenue over the past 12 months, HCA Healthcare is one of the most scaled enterprises in healthcare. This is particularly important because hospital chains companies are volume-driven businesses due to their low margins.

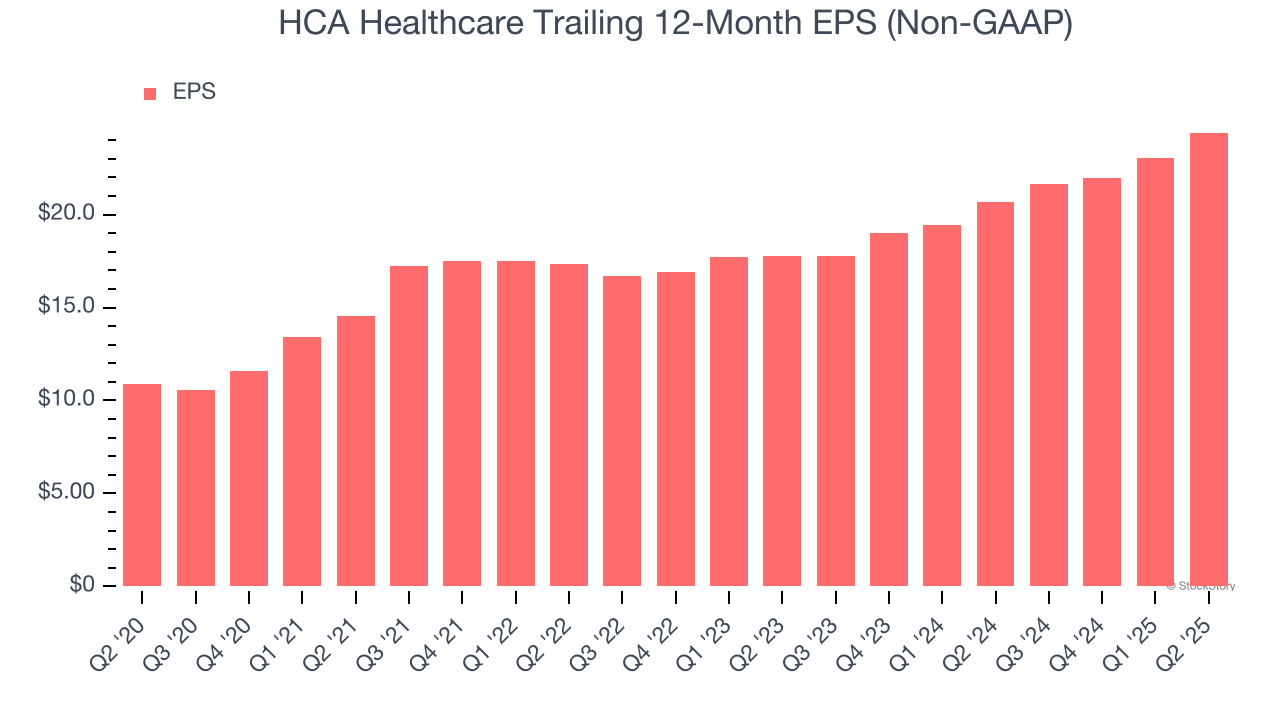

2. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

HCA Healthcare’s EPS grew at an astounding 17.5% compounded annual growth rate over the last five years, higher than its 7.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

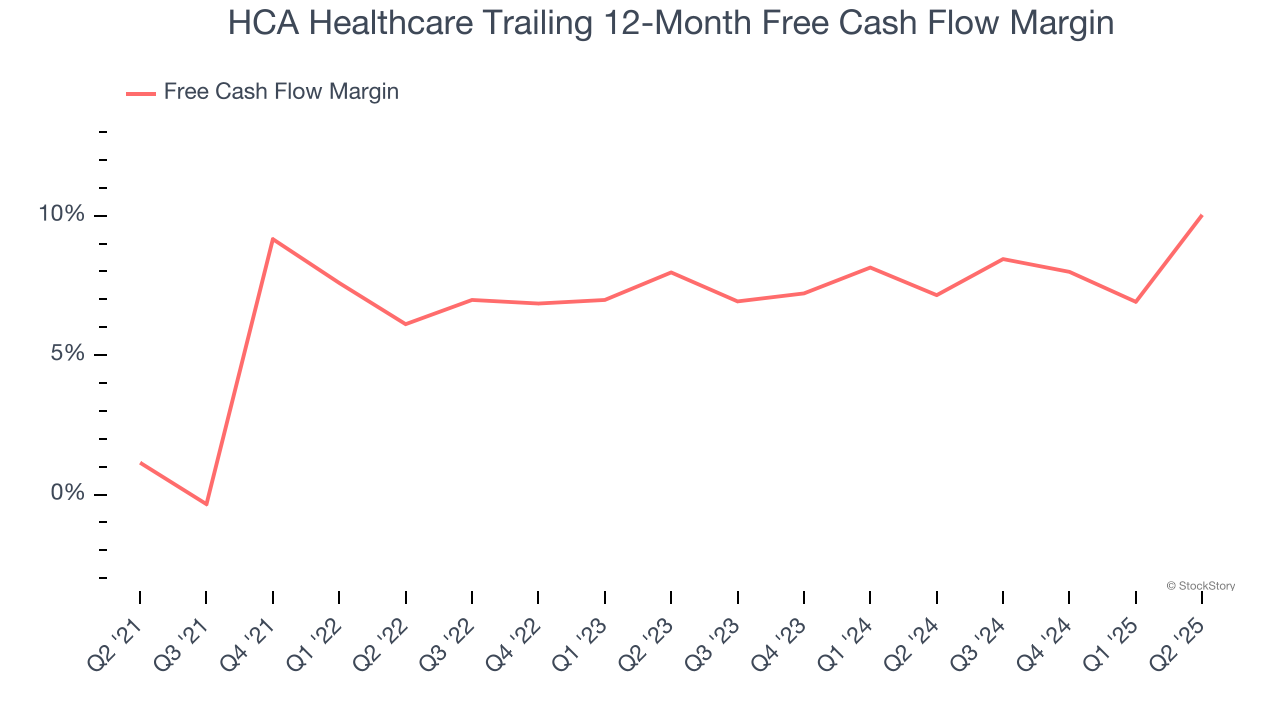

3. Increasing Free Cash Flow Margin Juices Financials

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, HCA Healthcare’s margin expanded by 8.9 percentage points over the last five years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell. HCA Healthcare’s free cash flow margin for the trailing 12 months was 10%.

Final Judgment

These are just a few reasons why HCA Healthcare ranks highly on our list, but at $419.60 per share (or 15.3× forward P/E), is now the right time to buy the stock? See for yourself in our comprehensive research report, it’s free for active Edge members .

Stocks We Like Even More Than HCA Healthcare

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.