As the craze of earnings season draws to a close, here’s a look back at some of the most exciting (and some less so) results from Q4. Today, we are looking at surgical equipment & consumables - diversified stocks, starting with Zimmer Biomet (NYSE: ZBH).

The surgical equipment and consumables industry provides tools, devices, and disposable products essential for surgeries and medical procedures. These companies therefore benefit from relatively consistent demand, driven by the ongoing need for medical interventions, recurring revenue from consumables, and long-term contracts with hospitals and healthcare providers. However, the high costs of R&D and regulatory compliance, coupled with intense competition and pricing pressures from cost-conscious customers, can constrain profitability. Over the next few years, tailwinds include aging populations, which tend to need surgical interventions at higher rates. The increasing integration of AI and robotics into surgical procedures could also create opportunities for differentiation and innovation. However, the industry faces headwinds including potential supply chain vulnerabilities, evolving regulatory requirements, and more widespread efforts to make healthcare less costly.

The 5 surgical equipment & consumables - diversified stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 1.5%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 11.7% since the latest earnings results.

Zimmer Biomet (NYSE: ZBH)

With a history dating back to 1927 and a presence in over 100 countries worldwide, Zimmer Biomet (NYSE: ZBH) designs and manufactures orthopedic products including knee and hip replacements, surgical tools, and robotic technologies for joint reconstruction and spine surgeries.

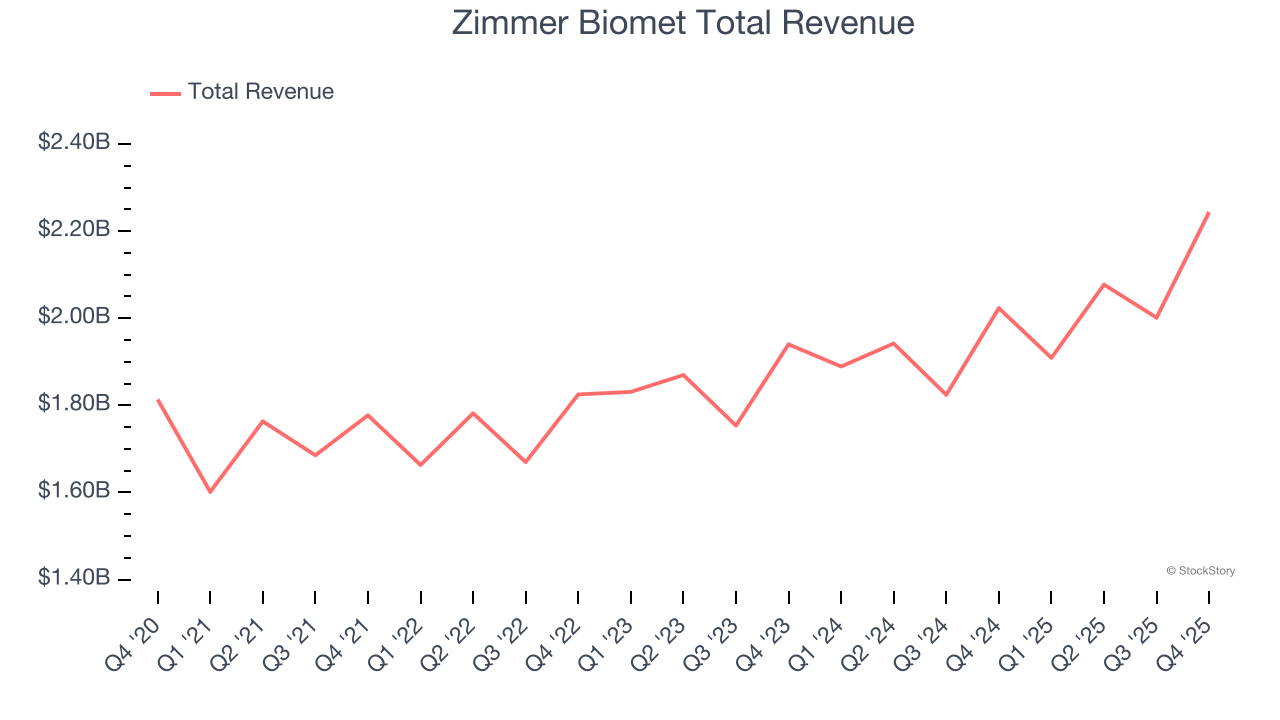

Zimmer Biomet reported revenues of $2.24 billion, up 10.9% year on year. This print exceeded analysts’ expectations by 0.9%. Despite the top-line beat, it was still a mixed quarter for the company with a narrow beat of analysts’ revenue estimates but a slight miss of analysts’ full-year EPS guidance estimates.

"We made significant strategic and financial progress in 2025, delivering on our initial revenue growth, EPS and free cash flow commitments and integrating three acquisitions, all while navigating tariff headwinds," said Ivan Tornos, Chairman, President and CEO of Zimmer Biomet.

Zimmer Biomet scored the fastest revenue growth but had the weakest performance against analyst estimates of the whole group. The results were likely priced in, however, and the stock is flat since reporting. It currently trades at $89.99.

Read our full report on Zimmer Biomet here, it’s free.

Best Q4: STERIS (NYSE: STE)

With a mission critical role in preventing healthcare-associated infections, STERIS (NYSE: STE) provides infection prevention products, sterilization services, and medical equipment that help healthcare facilities and life science companies maintain sterile environments.

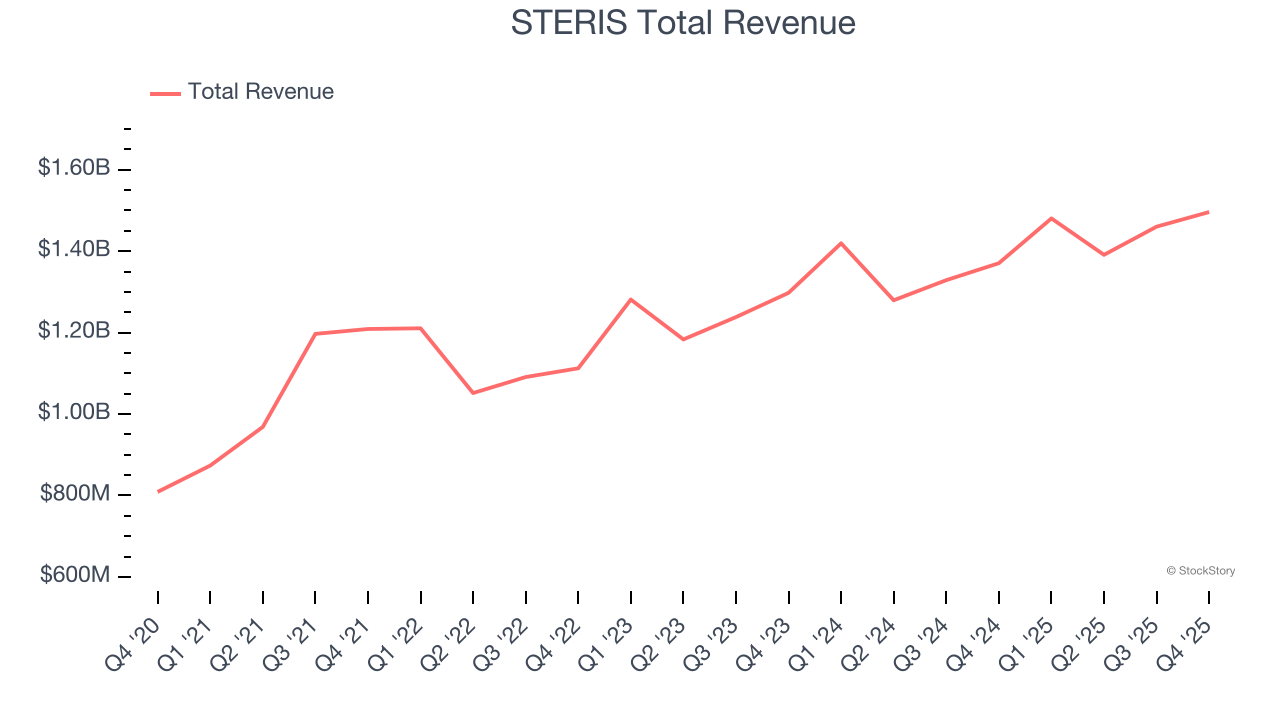

STERIS reported revenues of $1.50 billion, up 9.2% year on year, outperforming analysts’ expectations by 1.1%. The business performed better than its peers, but it was unfortunately a mixed quarter with a narrow beat of analysts’ revenue estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 18.2% since reporting. It currently trades at $216.24.

Is now the time to buy STERIS? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: CONMED (NYSE: CNMD)

With over five decades of experience in surgical innovation since its founding in 1970, CONMED (NYSE: CNMD) develops and manufactures medical devices and equipment for surgical procedures, specializing in orthopedic and general surgery products.

CONMED reported revenues of $373.2 million, up 7.9% year on year, exceeding analysts’ expectations by 1.7%. Still, it was a slower quarter as it posted a significant miss of analysts’ full-year EPS guidance estimates and full-year revenue guidance missing analysts’ expectations.

As expected, the stock is down 5.1% since the results and currently trades at $36.72.

Read our full analysis of CONMED’s results here.

Solventum (NYSE: SOLV)

Founded in 1985, Solventum (NYSE: SOLV) develops, manufactures, and commercializes a portfolio of healthcare products and services addressing critical customer and therapeutic patient needs.

Solventum reported revenues of $2.00 billion, down 3.7% year on year. This result surpassed analysts’ expectations by 1.9%. Zooming out, it was a mixed quarter as it also produced an impressive beat of analysts’ organic revenue estimates but a significant miss of analysts’ EPS estimates.

Solventum had the slowest revenue growth among its peers. The stock is down 10.6% since reporting and currently trades at $68.78.

Read our full, actionable report on Solventum here, it’s free.

BD (NYSE: BDX)

With a history dating back to 1897 and a presence in virtually every hospital around the globe, Becton Dickinson (NYSE: BDX) develops and manufactures medical supplies, devices, laboratory equipment and diagnostic products used by healthcare institutions and professionals worldwide.

BD reported revenues of $5.25 billion, up 1.6% year on year. This number topped analysts’ expectations by 2.1%. More broadly, it was a slower quarter as it recorded a significant miss of analysts’ full-year EPS guidance estimates.

BD delivered the biggest analyst estimates beat among its peers. The stock is down 25.1% since reporting and currently trades at $157.27.

Read our full, actionable report on BD here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.