Boutique fitness studio franchisor Xponential Fitness (NYSE: XPOF) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, but sales were flat year on year at $82.96 million. On the other hand, the company’s full-year revenue guidance of $265 million at the midpoint came in 12.5% below analysts’ estimates. Its non-GAAP loss of $0.91 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Xponential Fitness? Find out by accessing our full research report, it’s free.

Xponential Fitness (XPOF) Q4 CY2025 Highlights:

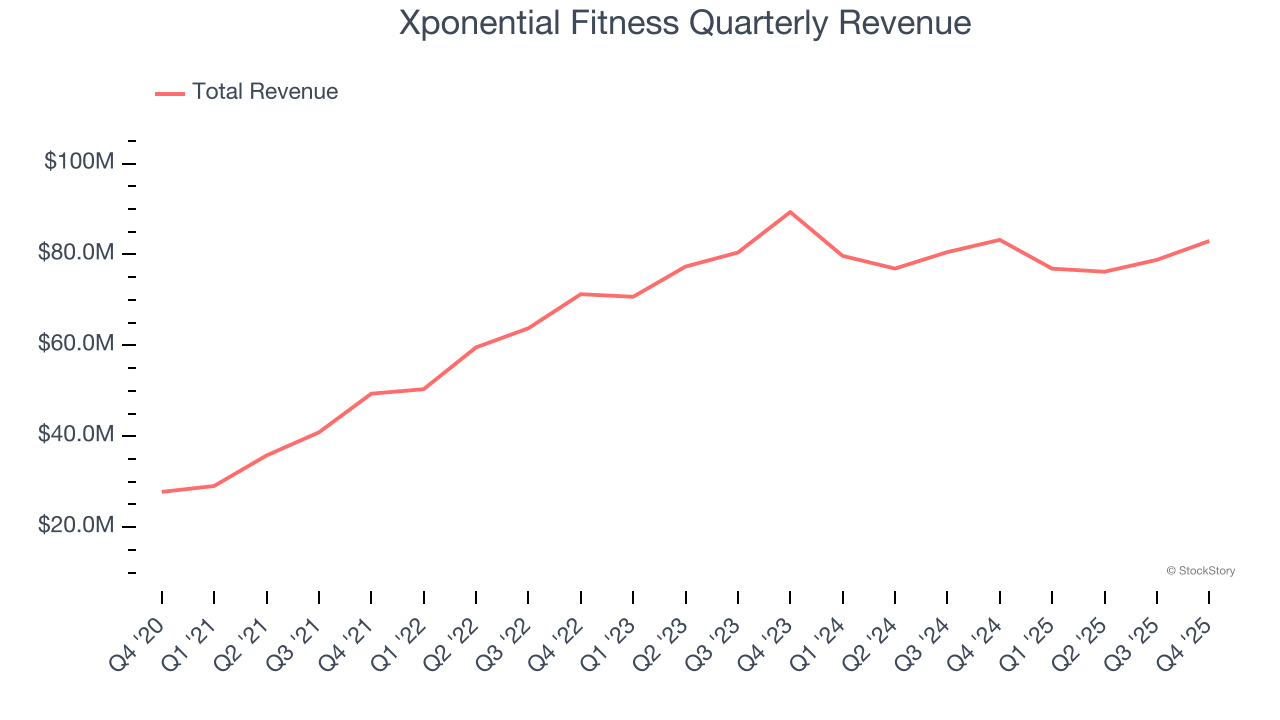

- Revenue: $82.96 million vs analyst estimates of $73.85 million (flat year on year, 12.3% beat)

- Adjusted EPS: -$0.91 vs analyst estimates of -$0.03 (significant miss)

- Adjusted EBITDA: $22.87 million vs analyst estimates of $19.18 million (27.6% margin, 19.2% beat)

- EBITDA guidance for the upcoming financial year 2026 is $105 million at the midpoint, below analyst estimates of $119.5 million

- Operating Margin: -9.9%, up from -62.4% in the same quarter last year

- Free Cash Flow Margin: 12.3%, up from 1.1% in the same quarter last year

- Market Capitalization: $289.4 million

“The fourth quarter capped a year of progress as we refined the strategic priorities that will drive Xponential’s long term growth,” said Mike Nuzzo, CEO of Xponential Fitness, Inc.

Company Overview

Owner of CycleBar, Rumble, and Club Pilates, Xponential Fitness (NYSE: XPOF) is a boutique fitness brand offering diverse and specialized exercise experiences.

Revenue Growth

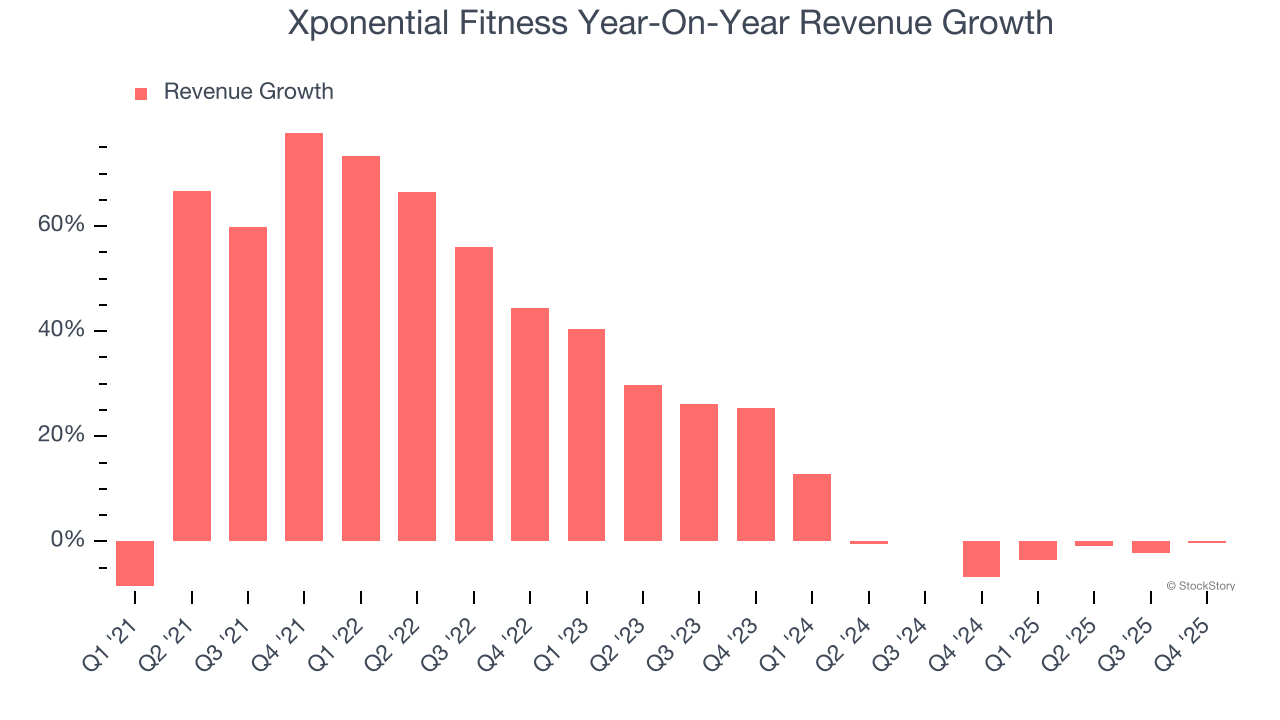

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Xponential Fitness grew its sales at a 24.2% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Xponential Fitness’s recent performance shows its demand has slowed as its revenue was flat over the last two years. Note that COVID hurt Xponential Fitness’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

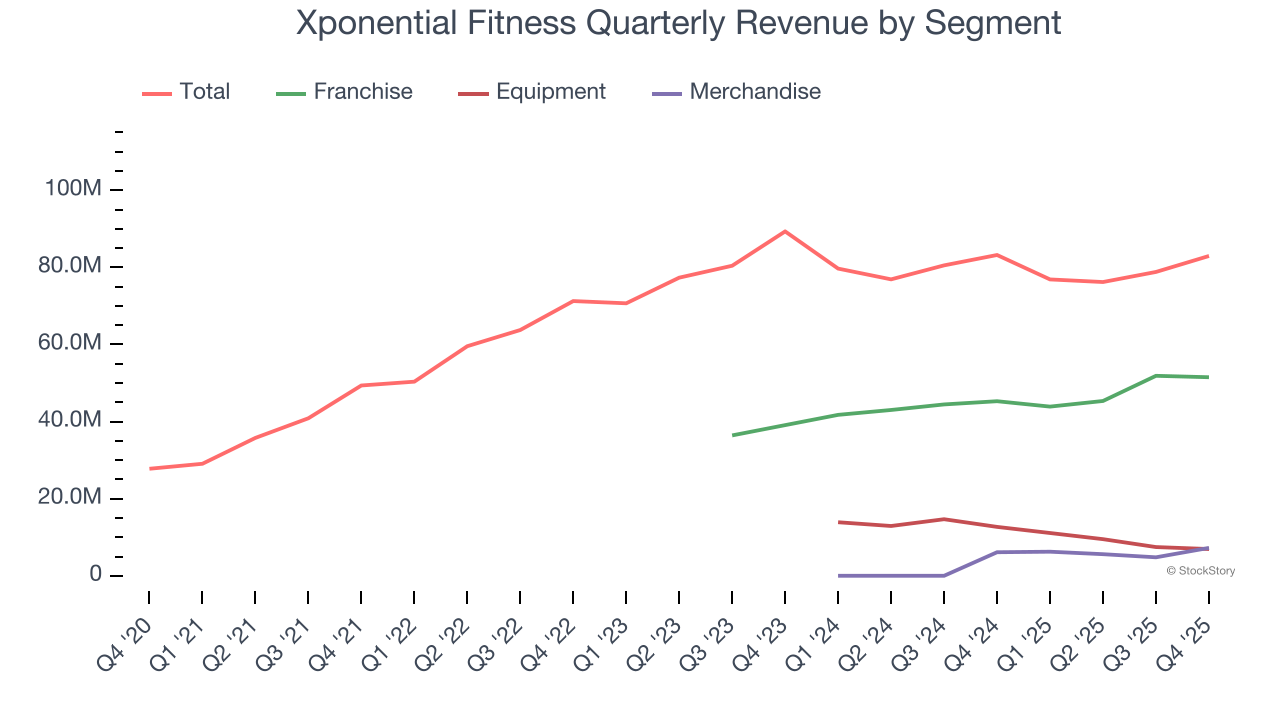

We can dig further into the company’s revenue dynamics by analyzing its three most important segments: Franchise, Equipment, and Merchandise, which are 62.1%, 8.4%, and 8.7% of revenue. Over the last two years, Xponential Fitness’s Franchise (royalty fees) and Merchandise (apparel sold to franchisees) revenues averaged year-on-year growth of 13.1% and 61,281%. On the other hand, its Equipment revenue (workout equipment sold to franchisees) averaged 35.2% declines.

This quarter, Xponential Fitness’s $82.96 million of revenue was flat year on year but beat Wall Street’s estimates by 12.3%.

Looking ahead, sell-side analysts expect revenue to decline by 4.3% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will face some demand challenges.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

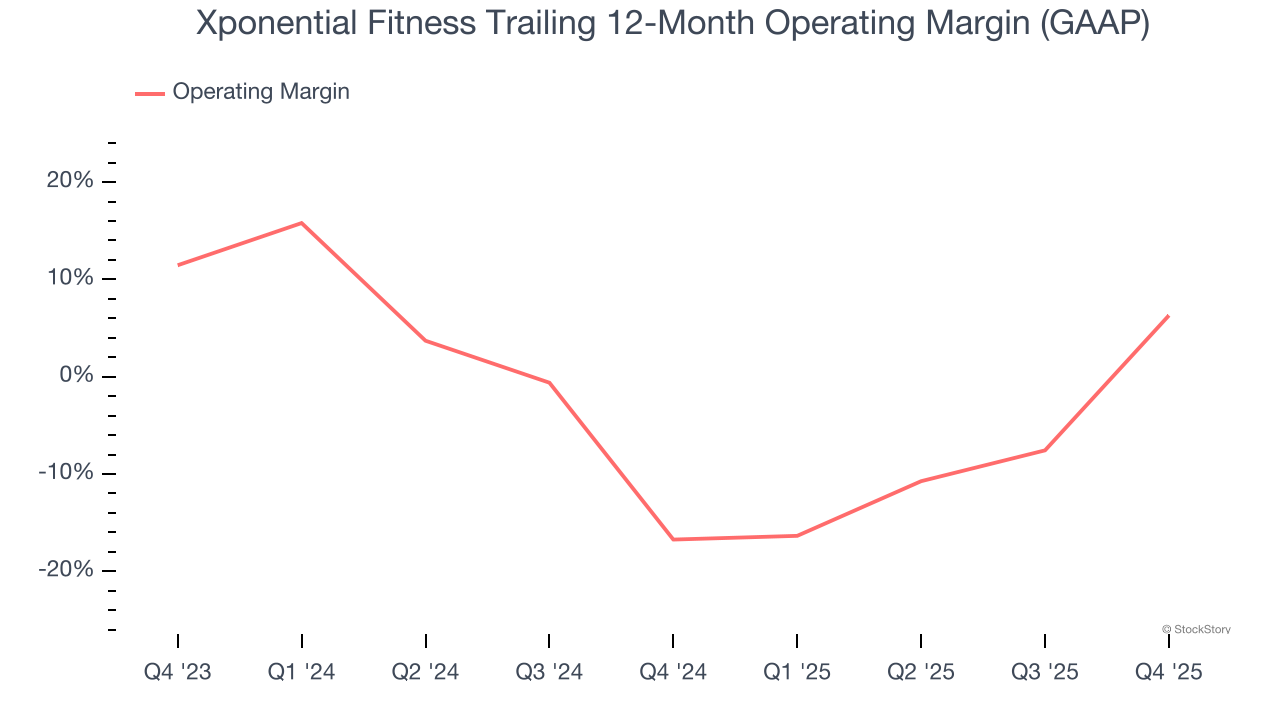

Xponential Fitness’s operating margin has risen over the last 12 months, but it still averaged negative 5.3% over the last two years. This is due to its large expense base and inefficient cost structure.

In Q4, Xponential Fitness generated a negative 9.9% operating margin. The company's consistent lack of profits raise a flag.

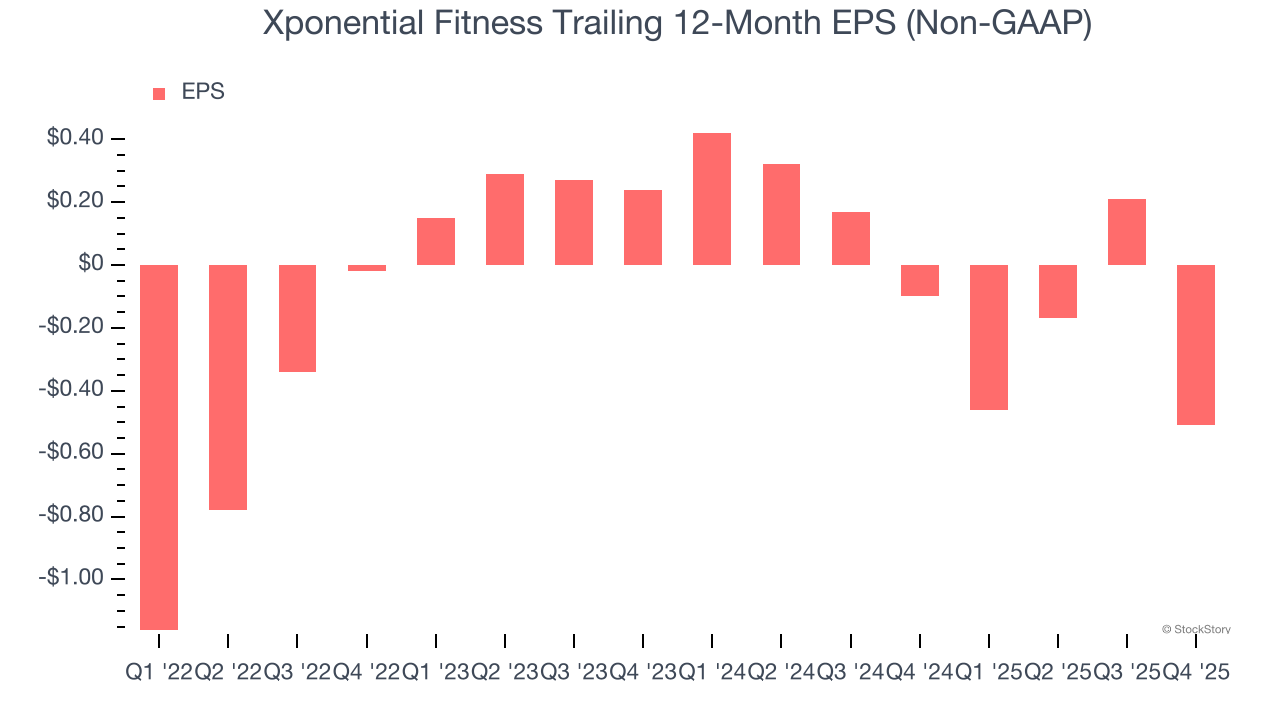

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Xponential Fitness’s full-year earnings are still negative, it reduced its losses and improved its EPS by 24.8% annually over the last four years. The next few quarters will be critical for assessing its long-term profitability.

In Q4, Xponential Fitness reported adjusted EPS of negative $0.91, down from negative $0.19 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Xponential Fitness’s full-year EPS of negative $0.51 will flip to positive $0.96.

Key Takeaways from Xponential Fitness’s Q4 Results

We were impressed by how significantly Xponential Fitness blew past analysts’ revenue expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 10.3% to $7.23 immediately after reporting.

Xponential Fitness’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).