What a brutal six months it’s been for Chegg. The stock has dropped 52.8% and now trades at $0.65, rattling many shareholders. This may have investors wondering how to approach the situation.

Is now the time to buy Chegg, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Chegg Will Underperform?

Even with the cheaper entry price, we're swiping left on Chegg for now. Here are three reasons why CHGG doesn't excite us and a stock we'd rather own.

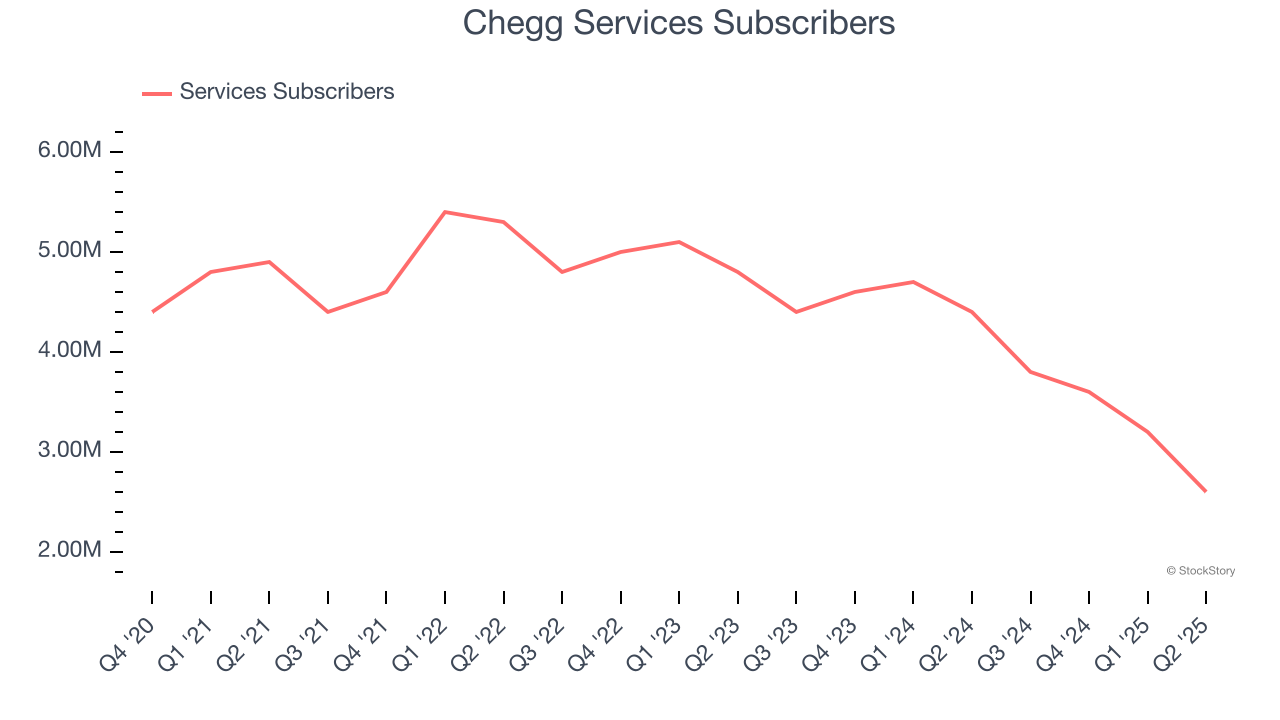

1. Declining Services Subscribers Reflect Product Weakness

As a subscription-based app, Chegg generates revenue growth by expanding both its subscriber base and the amount each subscriber spends over time.

Chegg struggled with new customer acquisition over the last two years as its services subscribers have declined by 20.7% annually. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Chegg wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

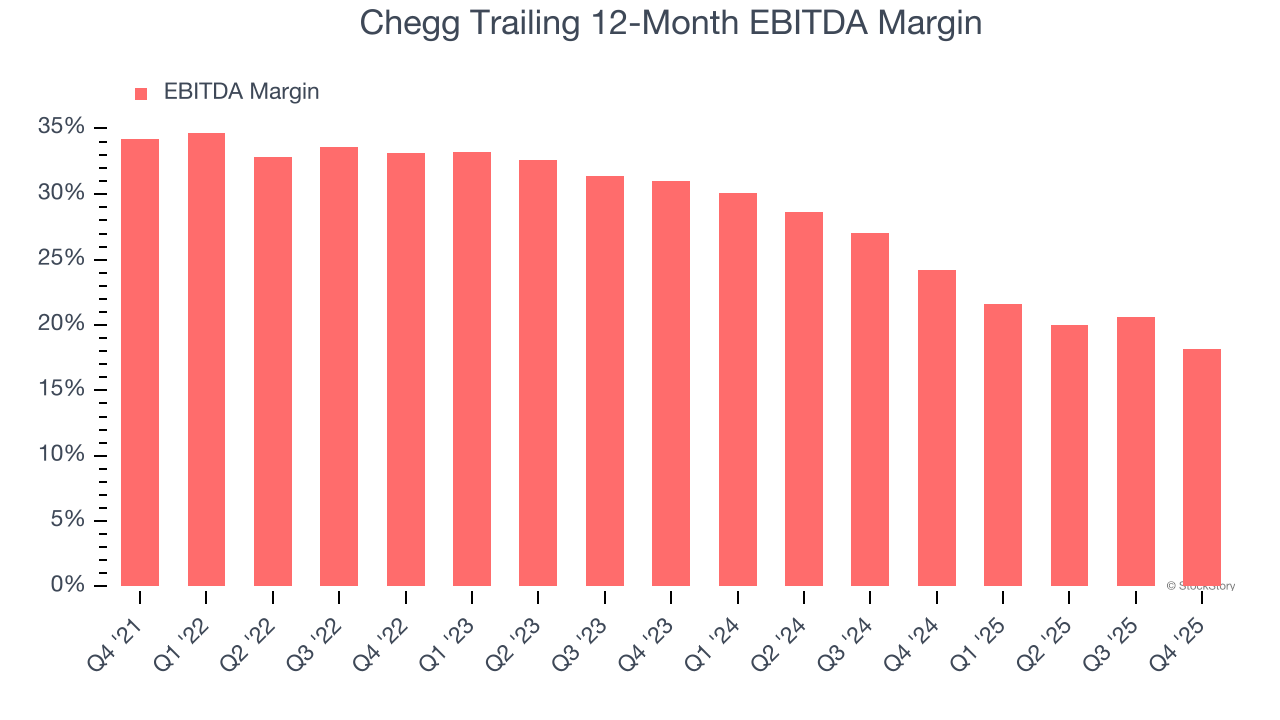

2. Shrinking EBITDA Margin

Operating income is often evaluated to assess a company’s underlying profitability. In a similar vein, EBITDA is used to analyze consumer internet companies because it excludes various one-time or non-cash expenses (depreciation), providing a clearer view of the business’s profit potential.

Analyzing the trend in its profitability, Chegg’s EBITDA margin decreased by 15 percentage points over the last few years. Even though its historical margin was healthy, shareholders will want to see Chegg become more profitable in the future. Its EBITDA margin for the trailing 12 months was 18.2%.

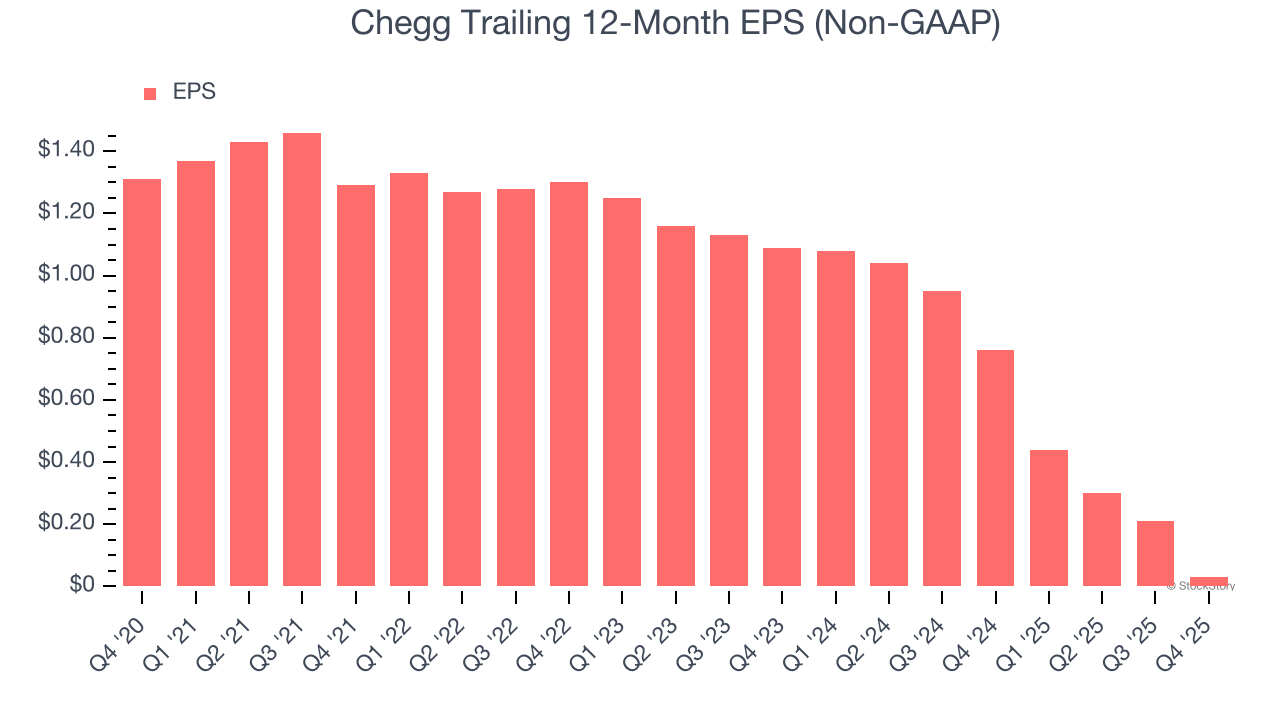

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Chegg, its EPS declined by 71.5% annually over the last three years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of Chegg, we’ll be cheering from the sidelines. After the recent drawdown, the stock trades at 2.2× forward EV/EBITDA (or $0.65 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are more exciting stocks to buy at the moment. We’d recommend looking at one of Charlie Munger’s all-time favorite businesses.

High-Quality Stocks for All Market Conditions

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.