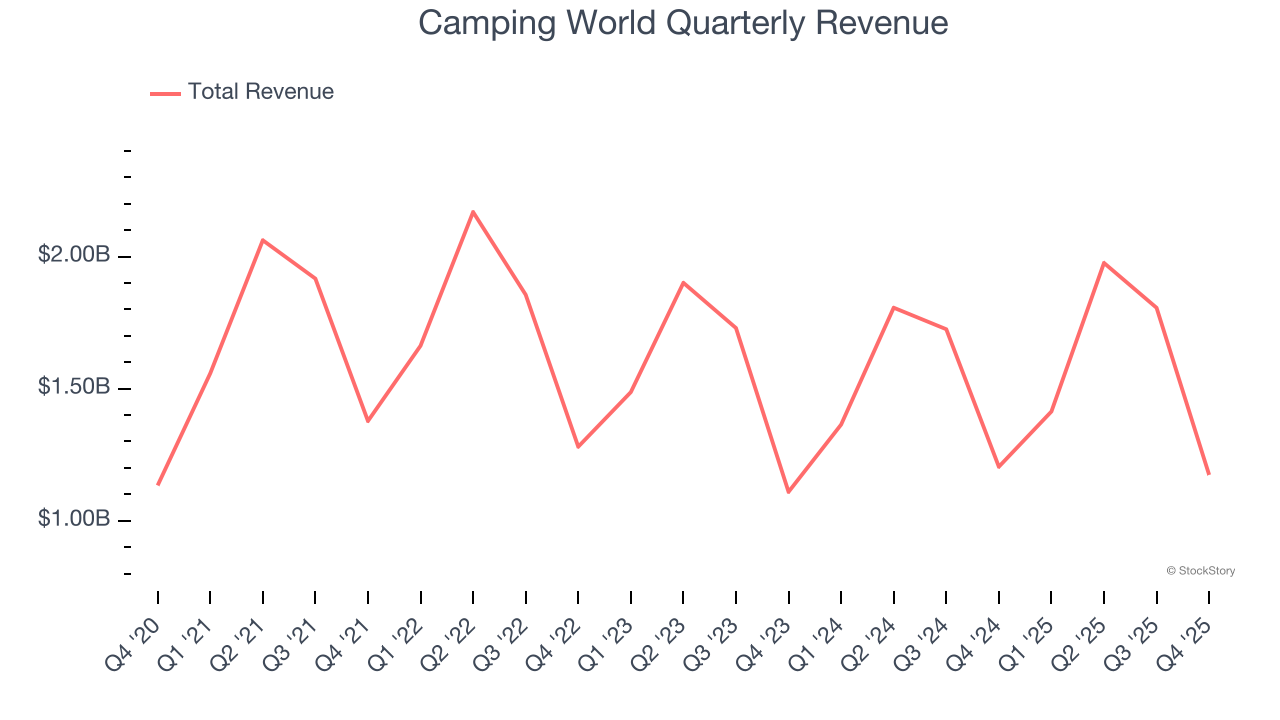

Recreational vehicle (RV) and boat retailer Camping World (NYSE: CWH) reported Q4 CY2025 results exceeding the market’s revenue expectations, but sales fell by 2.6% year on year to $1.17 billion. Its non-GAAP loss of $0.73 per share was 53.9% below analysts’ consensus estimates.

Is now the time to buy Camping World? Find out by accessing our full research report, it’s free.

Camping World (CWH) Q4 CY2025 Highlights:

- Revenue: $1.17 billion vs analyst estimates of $1.16 billion (2.6% year-on-year decline, 1.2% beat)

- Adjusted EPS: -$0.73 vs analyst expectations of -$0.47 (53.9% miss)

- Operating Margin: -4.3%, down from -1.3% in the same quarter last year

- Free Cash Flow was -$272.5 million compared to -$186 million in the same quarter last year

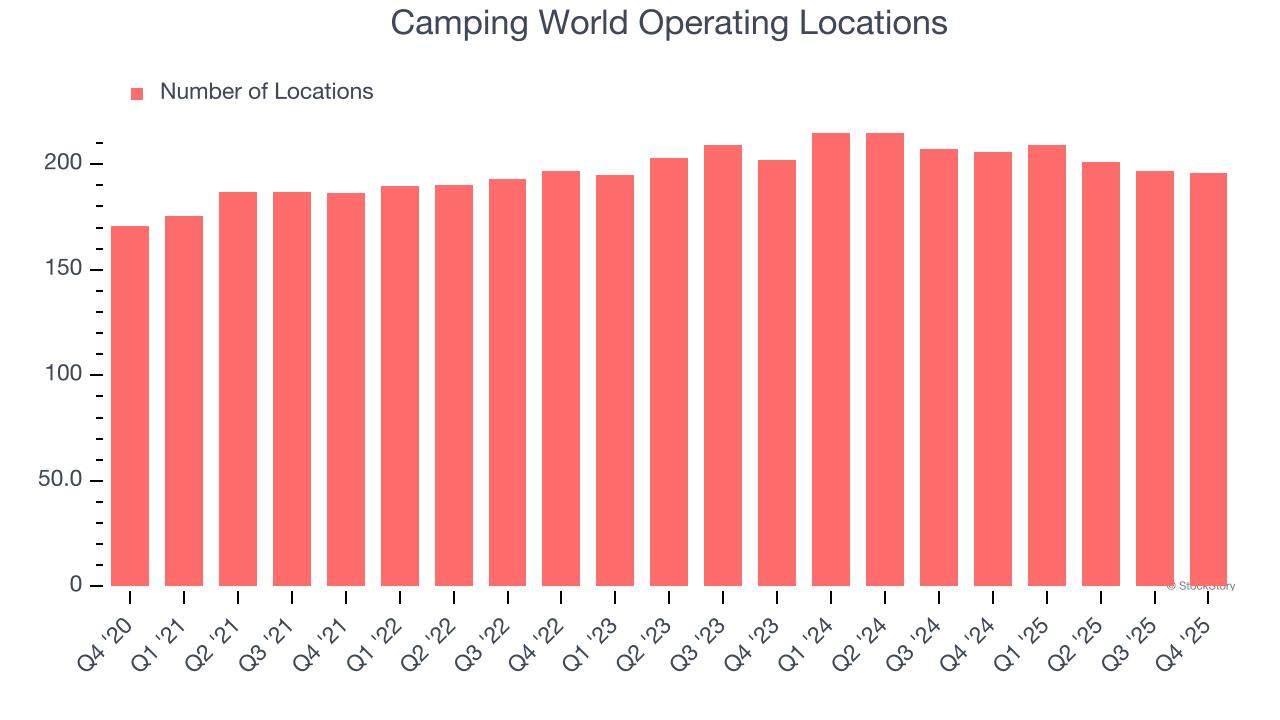

- Locations: 196 at quarter end, down from 206 in the same quarter last year

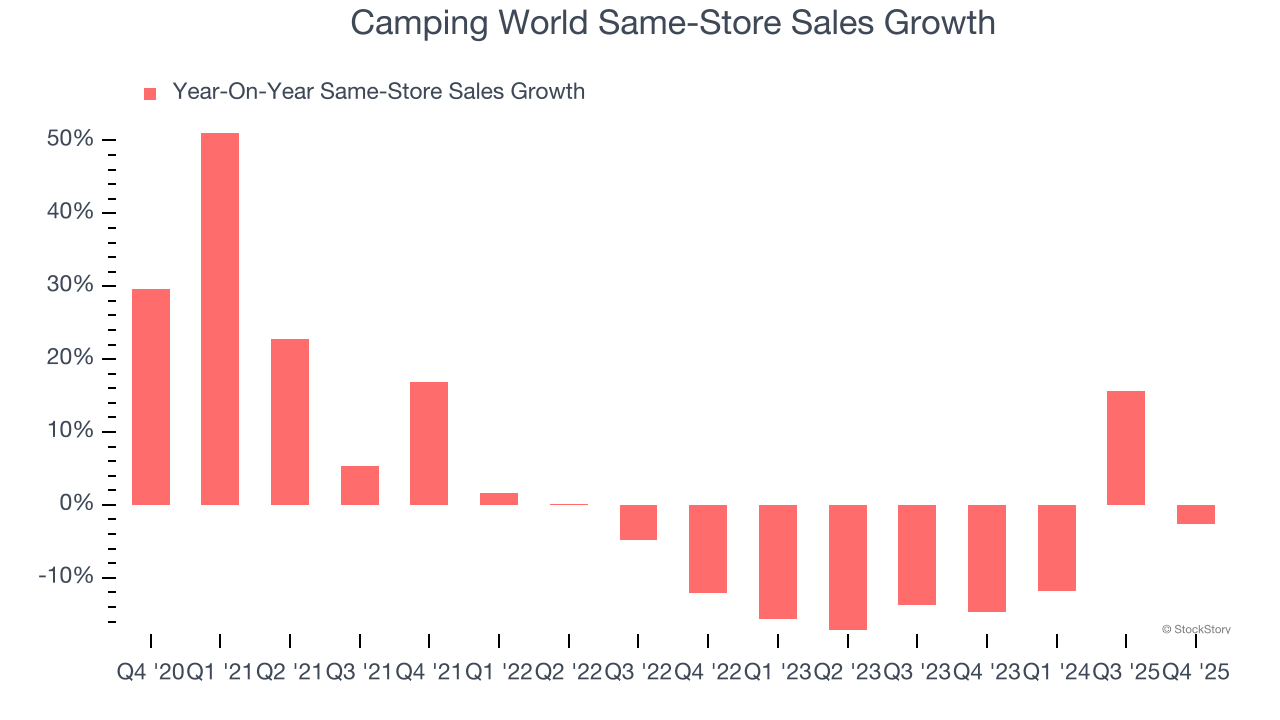

- Same-Store Sales were down 2.6% year on year

- Market Capitalization: $708.6 million

Company Overview

Founded in 1966 as a single recreational vehicle (RV) dealership, Camping World (NYSE: CWH) still sells RVs along with boats and general merchandise for outdoor activities.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $6.37 billion in revenue over the past 12 months, Camping World is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Camping World struggled to generate demand over the last three years. Its sales dropped by 2.9% annually as it didn’t open many new stores.

This quarter, Camping World’s revenue fell by 2.6% year on year to $1.17 billion but beat Wall Street’s estimates by 1.2%.

Looking ahead, sell-side analysts expect revenue to grow 3.6% over the next 12 months, an acceleration versus the last three years. This projection is above average for the sector and suggests its newer products will spur better top-line performance.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Store Performance

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Camping World operated 196 locations in the latest quarter, and over the last two years, has kept its store count flat while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Camping World’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and we’d be skeptical if Camping World starts opening new stores to artificially boost revenue growth.

In the latest quarter, Camping World’s same-store sales fell by 2.6% year on year. This decline was a reversal from its historical levels.

Key Takeaways from Camping World’s Q4 Results

It was good to see Camping World narrowly top analysts’ revenue expectations this quarter. On the other hand, its EBITDA missed and its gross margin fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 4.9% to $10.28 immediately following the results.

Camping World may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).