Over the last six months, Banner Bank’s shares have sunk to $60.43, producing a disappointing 9.9% loss - a stark contrast to the S&P 500’s 7.3% gain. This might have investors contemplating their next move.

Is there a buying opportunity in Banner Bank, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Banner Bank Will Underperform?

Despite the more favorable entry price, we're swiping left on Banner Bank for now. Here are three reasons why BANR doesn't excite us and a stock we'd rather own.

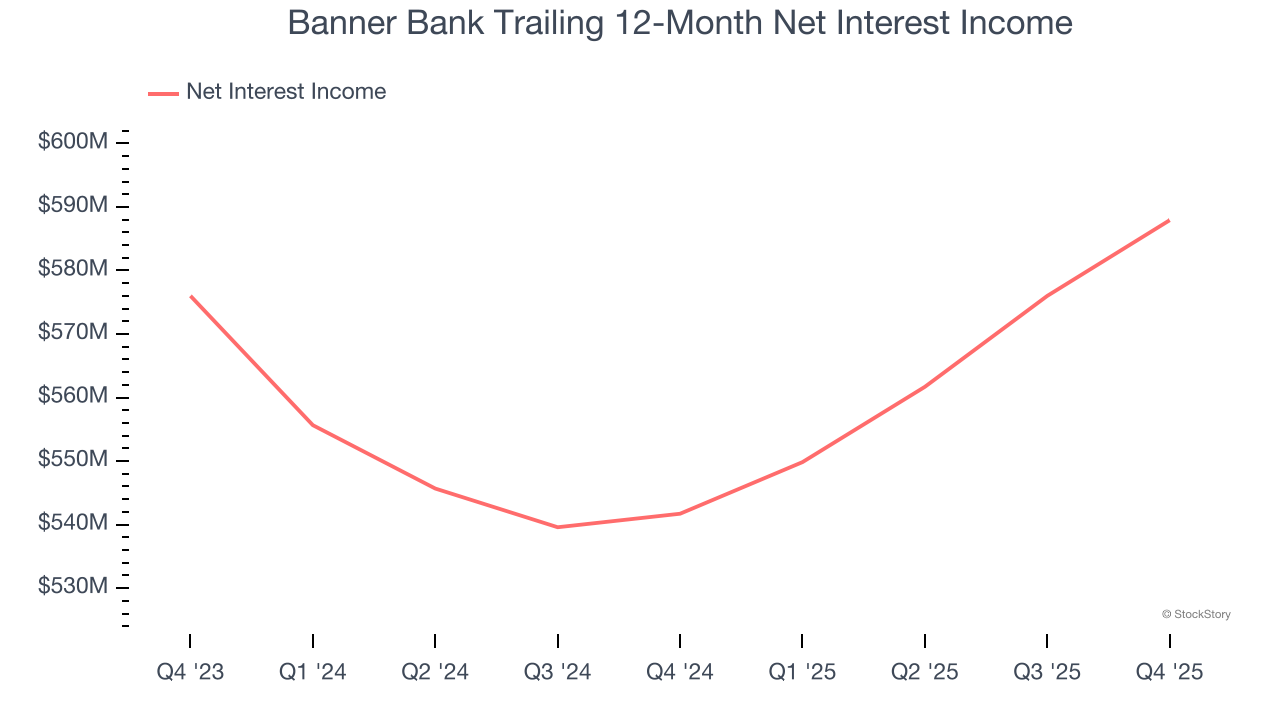

1. Net Interest Income Points to Soft Demand

Markets consistently prioritize net interest income over non-recurring fees, recognizing its superior quality compared to the more unpredictable revenue streams.

Banner Bank’s net interest income has grown at a 4.1% annualized rate over the last five years, much worse than the broader banking industry. Its growth was driven by an increase in its outstanding loans as its net interest margin, which represents how much a bank earns in relation to its outstanding loan book, was flat throughout that period.

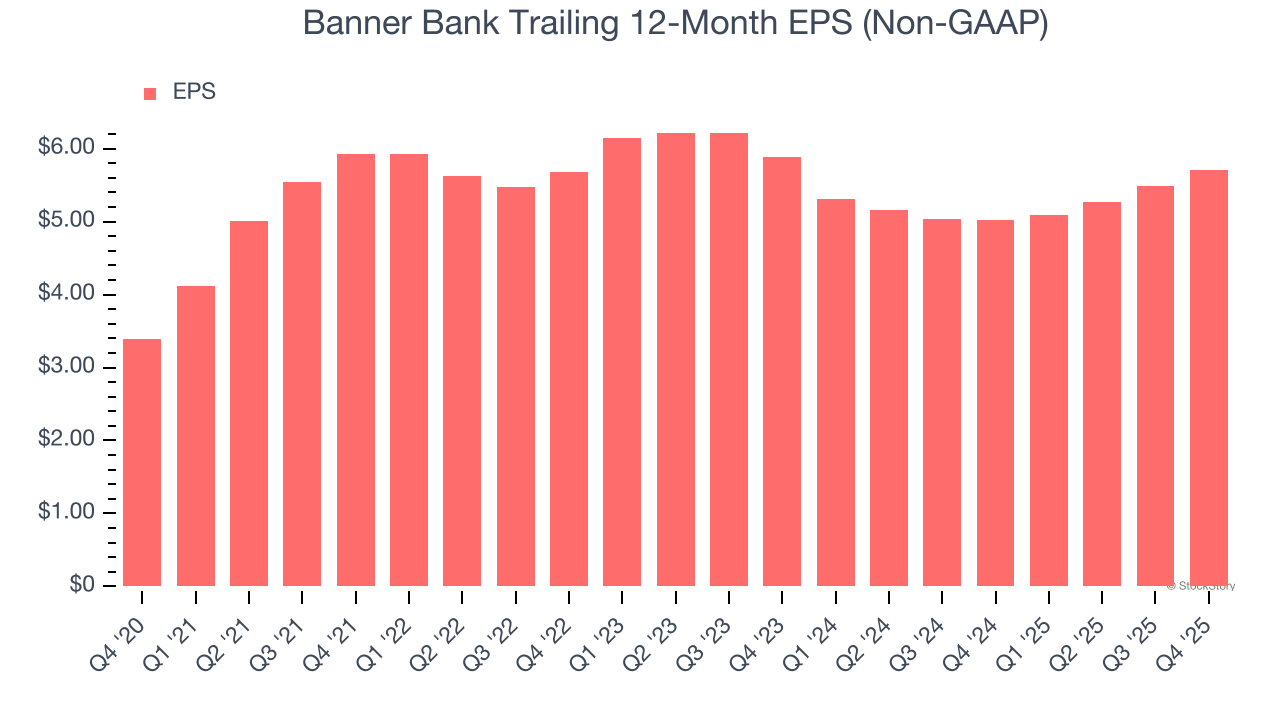

2. EPS Took a Dip Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Banner Bank, its EPS declined by 1.5% annually over the last two years while its revenue grew by 1.5%. This tells us the company became less profitable on a per-share basis as it expanded.

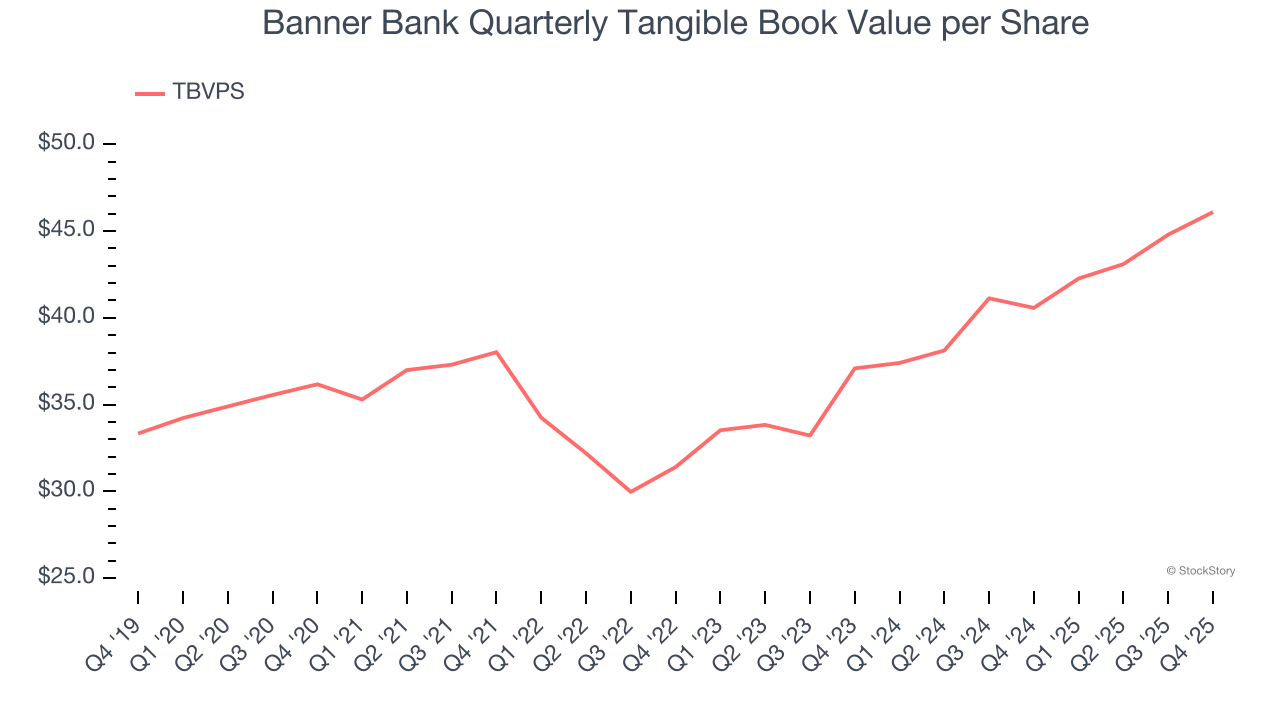

3. Projected TBVPS Growth Is Slim

The key to tangible book value per share (TBVPS) growth is a bank’s ability to earn consistent returns on its assets that exceed its funding costs and credit losses.

Over the next 12 months, Consensus estimates call for Banner Bank’s TBVPS to grow by 9.7% to $50.55, paltry growth rate.

Final Judgment

Banner Bank falls short of our quality standards. Following the recent decline, the stock trades at 1× forward P/B (or $60.43 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are better stocks to buy right now. We’d recommend looking at one of our all-time favorite software stocks.

Stocks We Like More Than Banner Bank

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.