The past six months have been a windfall for Kulicke and Soffa’s shareholders. The company’s stock price has jumped 89.4%, hitting $70.86 per share. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Kulicke and Soffa, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Kulicke and Soffa Will Underperform?

We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are three reasons we avoid KLIC and a stock we'd rather own.

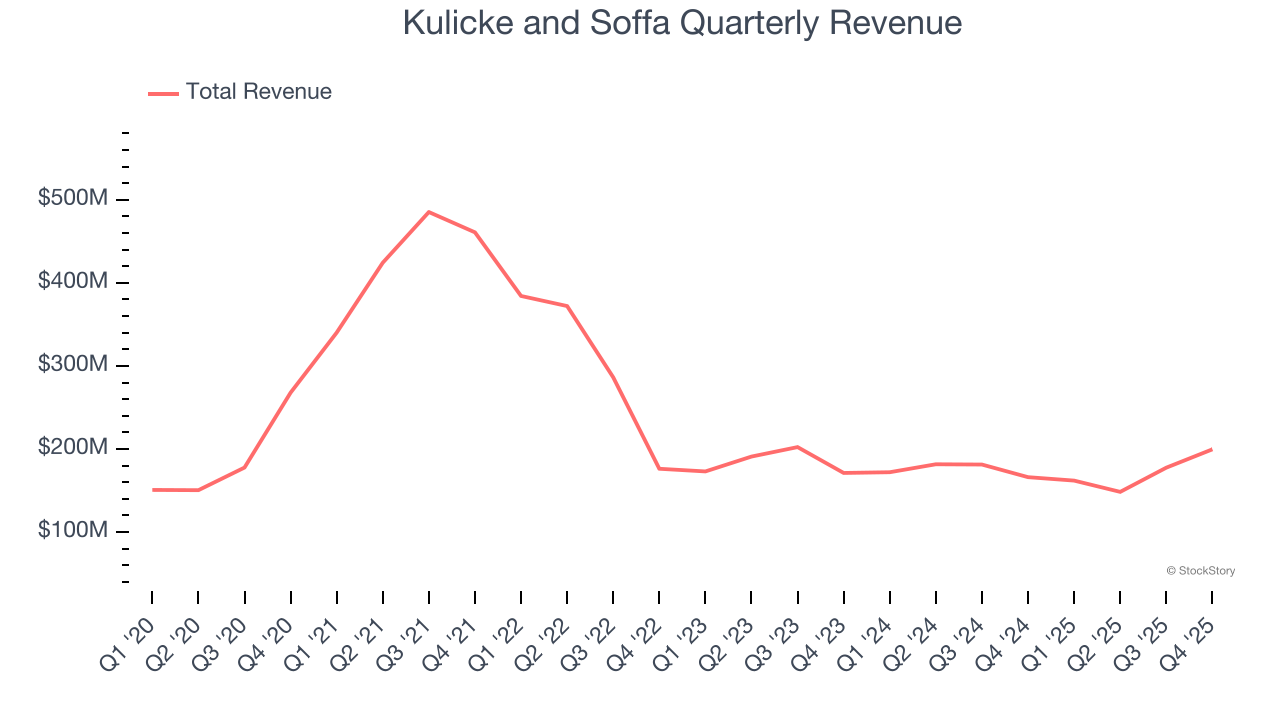

1. Revenue Spiraling Downwards

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Kulicke and Soffa’s demand was weak and its revenue declined by 1.6% per year. This wasn’t a great result and is a sign of poor business quality. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

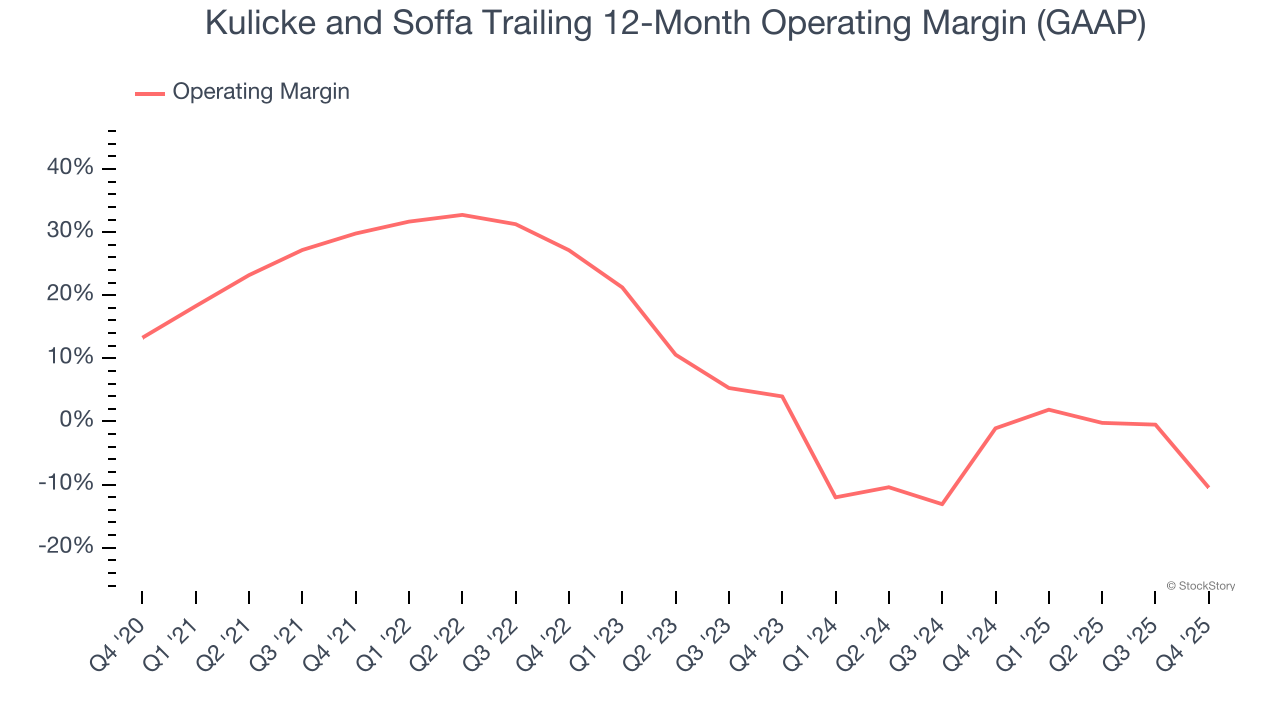

2. Shrinking Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Looking at the trend in its profitability, Kulicke and Soffa’s operating margin decreased by 40.3 percentage points over the last five years. Kulicke and Soffa’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its operating margin for the trailing 12 months was negative 10.5%.

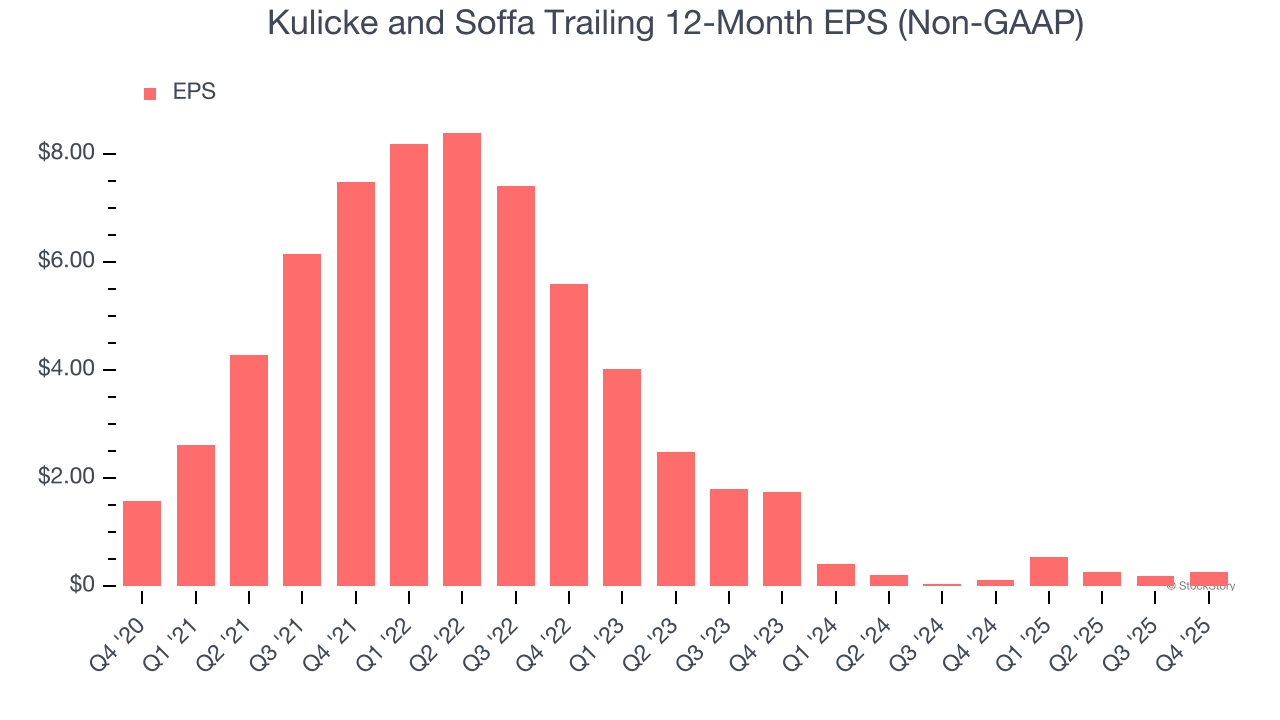

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Kulicke and Soffa, its EPS declined by 29.8% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Final Judgment

Kulicke and Soffa doesn’t pass our quality test. After the recent surge, the stock trades at 23.7× forward P/E (or $70.86 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think other companies feature superior fundamentals at the moment. We’d suggest looking at the most dominant software business in the world.

Stocks We Like More Than Kulicke and Soffa

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.