Regional banking company Byline Bancorp (NYSE: BY) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 11.8% year on year to $117 million. Its non-GAAP profit of $0.76 per share was 6% above analysts’ consensus estimates.

Is now the time to buy Byline Bancorp? Find out by accessing our full research report, it’s free.

Byline Bancorp (BY) Q4 CY2025 Highlights:

- Net Interest Income: $101.3 million vs analyst estimates of $98.35 million (14.4% year-on-year growth, 3% beat)

- Net Interest Margin: 4.4% vs analyst estimates of 4.2% (18.7 basis point beat)

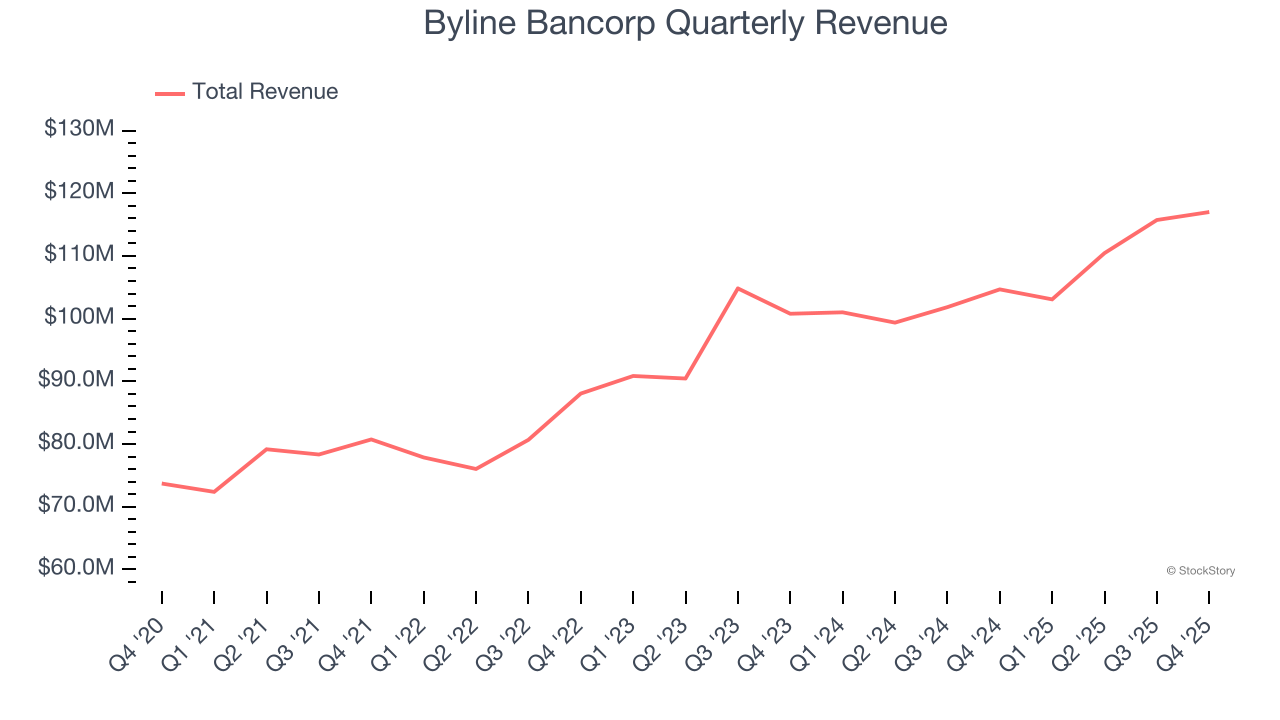

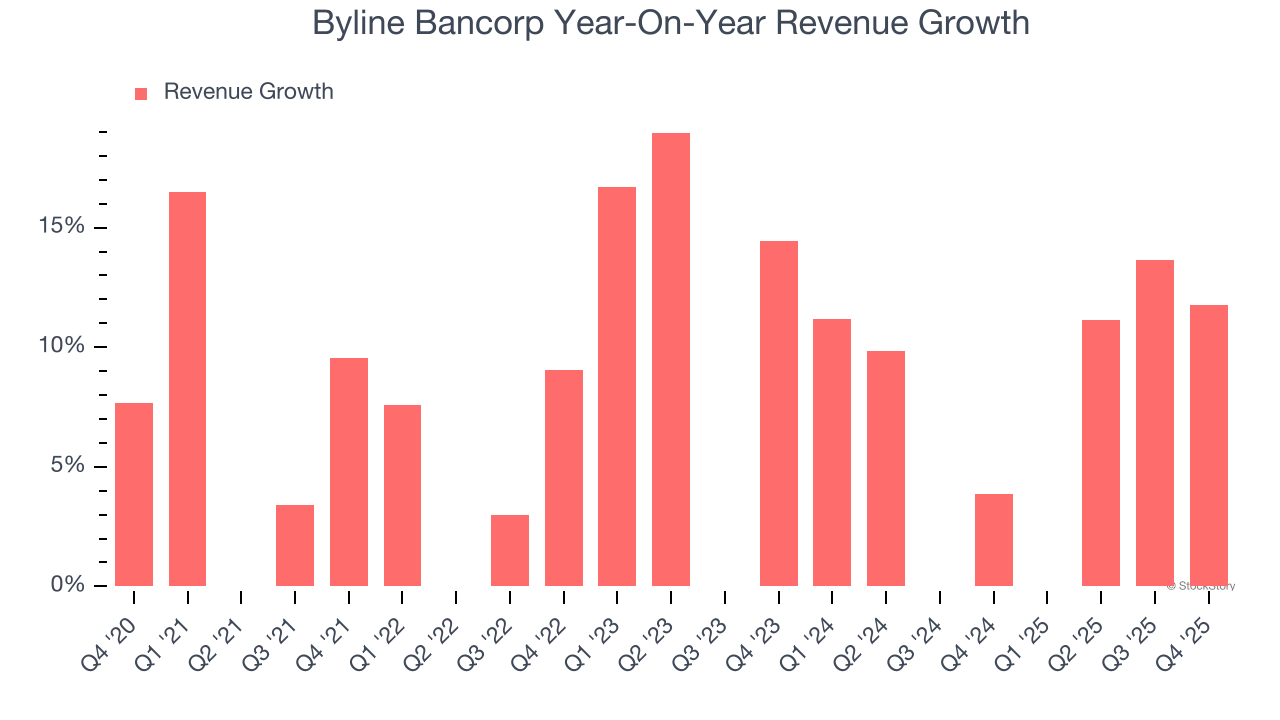

- Revenue: $117 million vs analyst estimates of $111.9 million (11.8% year-on-year growth, 4.6% beat)

- Efficiency Ratio: 50.3% vs analyst estimates of 52.9% (254.7 basis point beat)

- Adjusted EPS: $0.76 vs analyst estimates of $0.72 (6% beat)

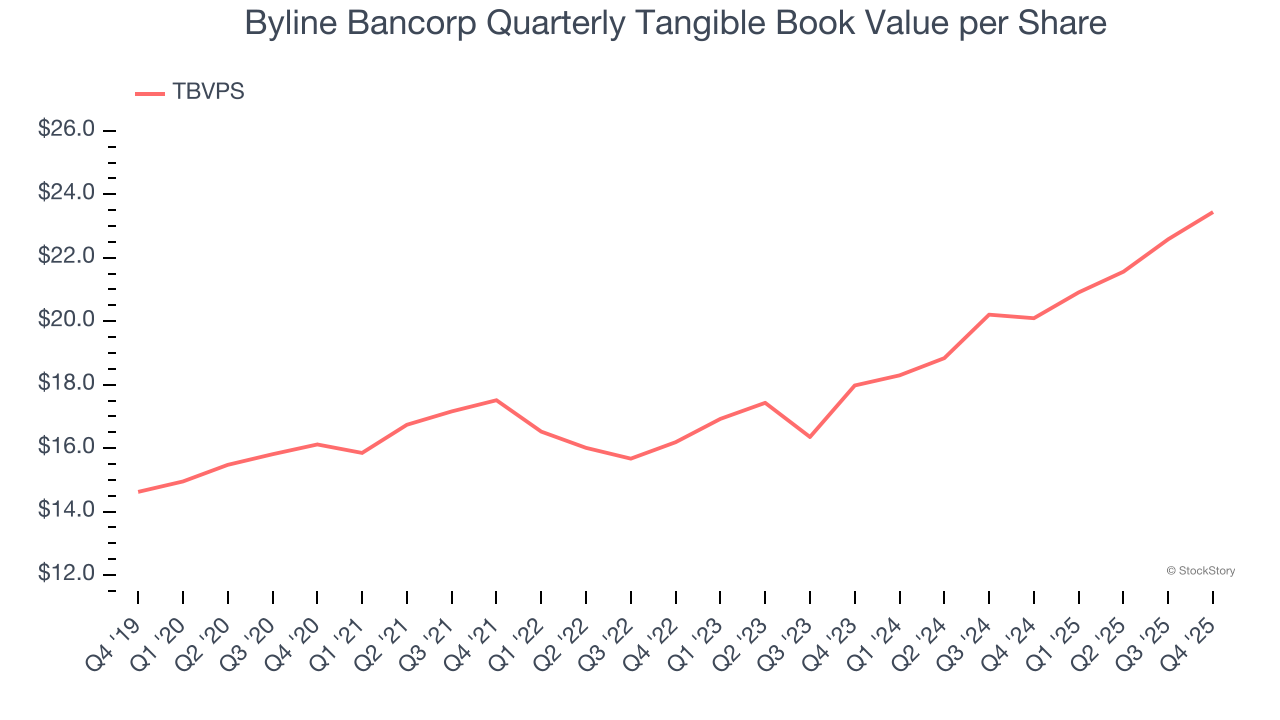

- Tangible Book Value per Share: $23.44 vs analyst estimates of $23.29 (16.6% year-on-year growth, 0.7% beat)

- Market Capitalization: $1.45 billion

Roberto R. Herencia, Executive Chairman and CEO of Byline Bancorp, commented, "Throughout 2025 we advanced our strategy of becoming the preeminent commercial bank in Chicago and delivering strong financial results. We made significant progress across our strategic priorities—deepening our commercial presence, growing customers, and executing initiatives that strengthened our franchise. As we enter 2026, we are operating from a position of strength, remain focused on consistent execution of our strategy, supporting our customers, and driving long‑term value for our stockholders. "

Company Overview

Ranking as the fifth most active Small Business Administration lender in the country, Byline Bancorp (NYSE: BY) is a Chicago-based bank that provides banking services to small and medium-sized businesses, commercial real estate developers, and consumers.

Sales Growth

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees. Over the last five years, Byline Bancorp grew its revenue at a decent 10% compounded annual growth rate. Its growth was slightly above the average banking company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Byline Bancorp’s recent performance shows its demand has slowed as its annualized revenue growth of 7.4% over the last two years was below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Byline Bancorp reported year-on-year revenue growth of 11.8%, and its $117 million of revenue exceeded Wall Street’s estimates by 4.6%.

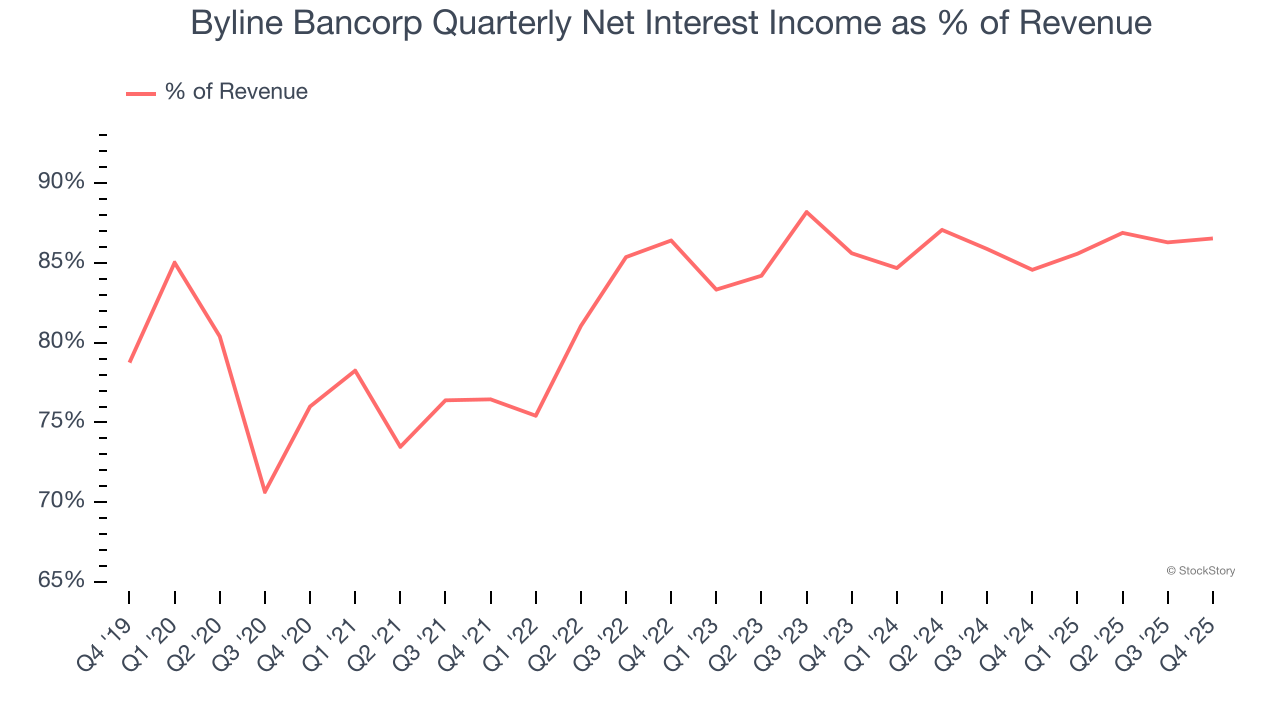

Net interest income made up 83.1% of the company’s total revenue during the last five years, meaning Byline Bancorp barely relies on non-interest income to drive its overall growth.

Net interest income commands greater market attention due to its reliability and consistency, whereas non-interest income is often seen as lower-quality revenue that lacks the same dependable characteristics.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Tangible Book Value Per Share (TBVPS)

Banks are balance sheet-driven businesses because they generate earnings primarily through borrowing and lending. They’re also valued based on their balance sheet strength and ability to compound book value (another name for shareholders’ equity) over time.

This is why we consider tangible book value per share (TBVPS) the most important metric to track for banks. TBVPS represents the real, liquid net worth per share of a bank, excluding intangible assets that have debatable value upon liquidation. On the other hand, EPS is often distorted by mergers and flexible loan loss accounting. TBVPS provides clearer performance insights.

Byline Bancorp’s TBVPS grew at an impressive 7.8% annual clip over the last five years. TBVPS growth has also accelerated recently, growing by 14.2% annually over the last two years from $17.98 to $23.44 per share.

Over the next 12 months, Consensus estimates call for Byline Bancorp’s TBVPS to grow by 10.6% to $25.92, mediocre growth rate.

Key Takeaways from Byline Bancorp’s Q4 Results

We enjoyed seeing Byline Bancorp beat analysts’ revenue expectations this quarter. We were also glad its net interest income outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flat at $31.70 immediately following the results.

Is Byline Bancorp an attractive investment opportunity at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).