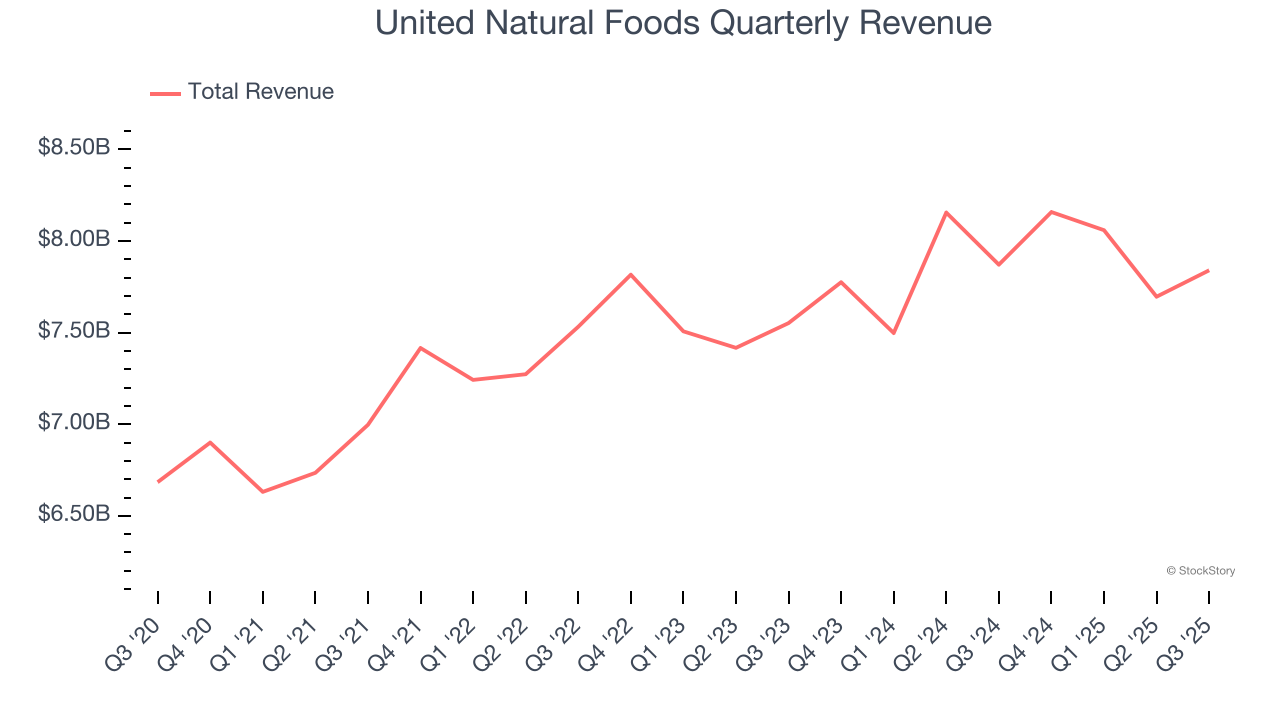

Food distribution company United Natural Foods (NYSE: UNFI) fell short of the markets revenue expectations in Q3 CY2025, with sales flat year on year at $7.84 billion. The company’s full-year revenue guidance of $31.8 billion at the midpoint came in 0.7% below analysts’ estimates. Its non-GAAP profit of $0.56 per share was 40.3% above analysts’ consensus estimates.

Is now the time to buy United Natural Foods? Find out by accessing our full research report, it’s free for active Edge members.

United Natural Foods (UNFI) Q3 CY2025 Highlights:

- Revenue: $7.84 billion vs analyst estimates of $7.91 billion (flat year on year, 0.9% miss)

- Adjusted EPS: $0.56 vs analyst estimates of $0.40 (40.3% beat)

- Adjusted EBITDA: $167 million vs analyst estimates of $156.2 million (2.1% margin, 6.9% beat)

- EBITDA guidance for the full year is $665 million at the midpoint, in line with analyst expectations

- Operating Margin: 0.2%, in line with the same quarter last year

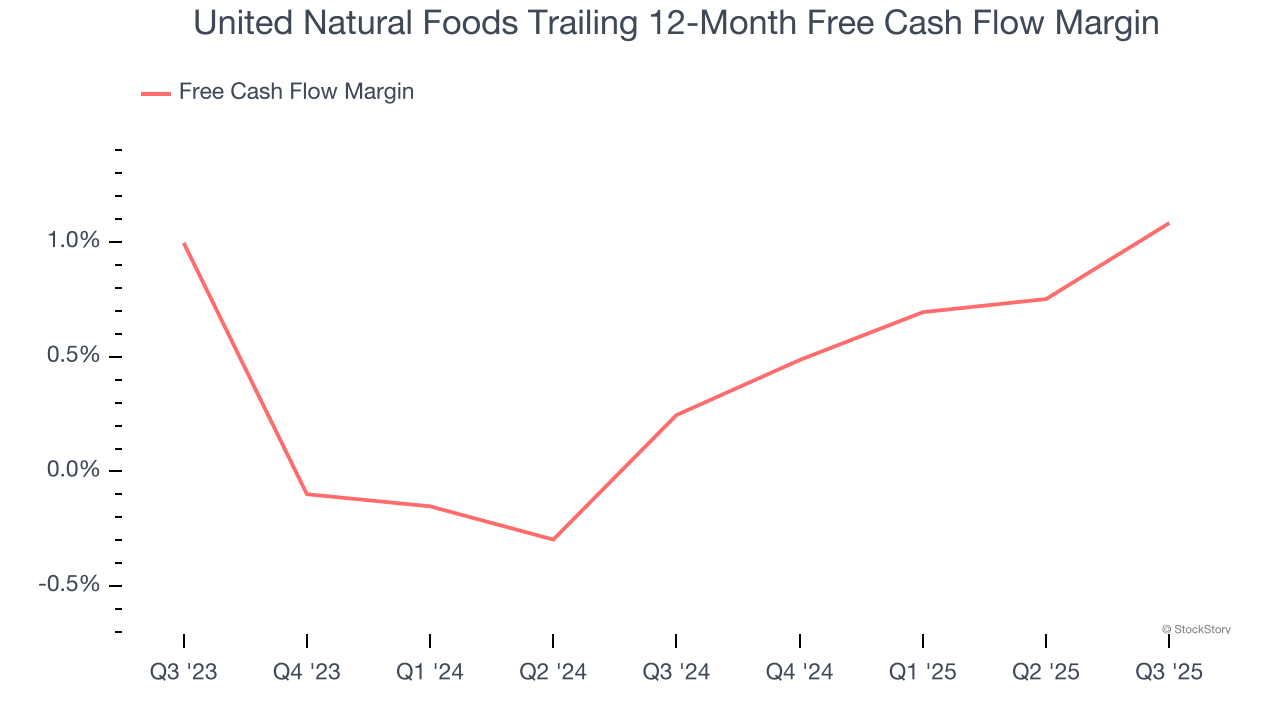

- Free Cash Flow was -$54 million compared to -$159 million in the same quarter last year

- Market Capitalization: $2.04 billion

Company Overview

With a vast network of 55 distribution centers spanning approximately 30 million square feet of warehouse space, United Natural Foods (NYSE: UNFI) is North America's premier grocery wholesaler distributing natural, organic, and conventional products to over 30,000 retail locations across the US and Canada.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $31.75 billion in revenue over the past 12 months, United Natural Foods is one of the most widely recognized consumer staples companies. Its influence over consumers gives it negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don’t have). However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing brands have penetrated most of the market. To accelerate sales, United Natural Foods likely needs to optimize its pricing or lean into new products and international expansion.

As you can see below, United Natural Foods grew its sales at a sluggish 2.5% compounded annual growth rate over the last three years. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

This quarter, United Natural Foods missed Wall Street’s estimates and reported a rather uninspiring 0.4% year-on-year revenue decline, generating $7.84 billion of revenue.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a slight deceleration versus the last three years. This projection doesn't excite us and implies its products will see some demand headwinds.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

United Natural Foods broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

United Natural Foods broke even from a free cash flow perspective in Q3. This result was good as its margin was 1.3 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends carry greater meaning.

Key Takeaways from United Natural Foods’s Q3 Results

It was good to see United Natural Foods beat analysts’ EPS expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance slightly missed and its revenue fell slightly short of Wall Street’s estimates. Overall, we think this was still a decent quarter with some key metrics above expectations. The stock remained flat at $33.42 immediately after reporting.

Big picture, is United Natural Foods a buy here and now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.