E-commerce software platform Shopify (NYSE: SHOP) announced better-than-expected revenue in Q4 CY2024, with sales up 31.2% year on year to $2.81 billion. The company expects next quarter’s revenue to be around $2.33 billion, close to analysts’ estimates. Its GAAP profit of $0.99 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Shopify? Find out by accessing our full research report, it’s free.

Shopify (SHOP) Q4 CY2024 Highlights:

- Revenue: $2.81 billion vs analyst estimates of $2.73 billion (31.2% year-on-year growth, 3% beat)

- EPS (GAAP): $0.99 vs analyst estimates of $0.33 (significant beat due to certain items below operating profit)

- Adjusted EBITDA: $582 million vs analyst estimates of $566.5 million (20.7% margin, 2.7% beat)

- Revenue Guidance for Q1 CY2025 is $2.33 billion at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: 16.5%, up from 13.5% in the same quarter last year

- Free Cash Flow Margin: 21.7%, up from 19.5% in the previous quarter

- Market Capitalization: $154.9 billion

Company Overview

Originally created as an internal tool for a snowboarding company, Shopify (NYSE: SHOP) provides a software platform for building and operating e-commerce businesses.

E-commerce Software

While e-commerce has been around for over two decades and enjoyed meaningful growth, its overall penetration of retail still remains low. Only around $1 in every $5 spent on retail purchases comes from digital orders, leaving over 80% of the retail market still ripe for online disruption. It is these large swathes of the retail where e-commerce has not yet taken hold that drives the demand for various e-commerce software solutions.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Shopify grew its sales at a solid 24.4% compounded annual growth rate. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, Shopify reported wonderful year-on-year revenue growth of 31.2%, and its $2.81 billion of revenue exceeded Wall Street’s estimates by 3%. Company management is currently guiding for a 25% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 22.2% over the next 12 months, a slight deceleration versus the last three years. Still, this projection is admirable and implies the market is factoring in success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

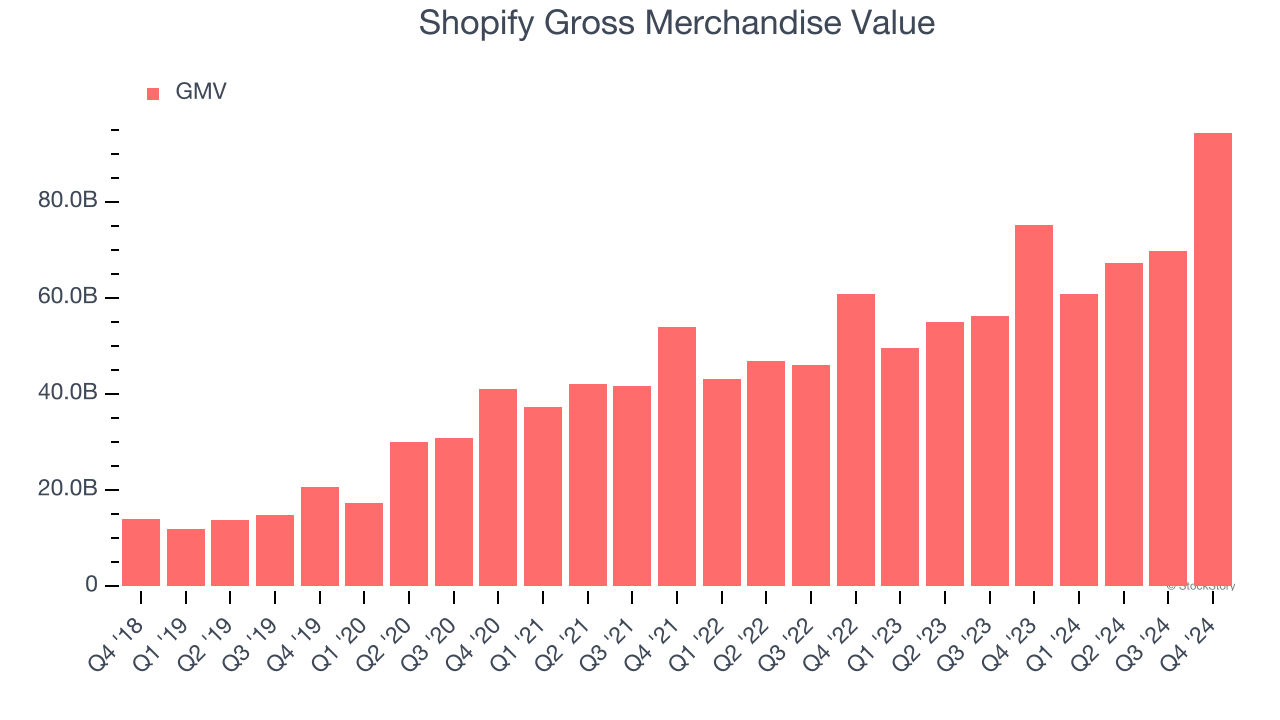

Gross Merchandise Value

GMV, or gross merchandise value, is the total value of goods and services sold on Shopify’s platform. This is the number from which the company will ultimately collect fees (usually called a take rate), and the higher it is, the higher the switching costs, enabling Shopify to monetize in additional ways (like subscription revenue for more services).

Shopify’s GMV punched in at $94.46 billion in Q4, and over the last four quarters, its growth was impressive as it averaged 23.7% year-on-year increases. This alternate topline metric grew slower than total sales, meaning its revenue from adjacent products such as merchant loans and AI-driven inventory management software outpaced its transaction fees. This signals the company is locking its customers further into its platform and mining them for profits.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Shopify is extremely efficient at acquiring new customers, and its CAC payback period checked in at 6.6 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Shopify more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

Key Takeaways from Shopify’s Q4 Results

It was encouraging to see Shopify beat analysts’ gross merchandise volume expectations this quarter, leading to better revenue and profits. On the other hand, revenue guidance for next quarter was just in line, and this has shown to not be enough for fast-growing, premium-valuation SaaS companies. Shares traded down 9.5% to $108.50 immediately following the results.

Should you buy the stock or not? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.