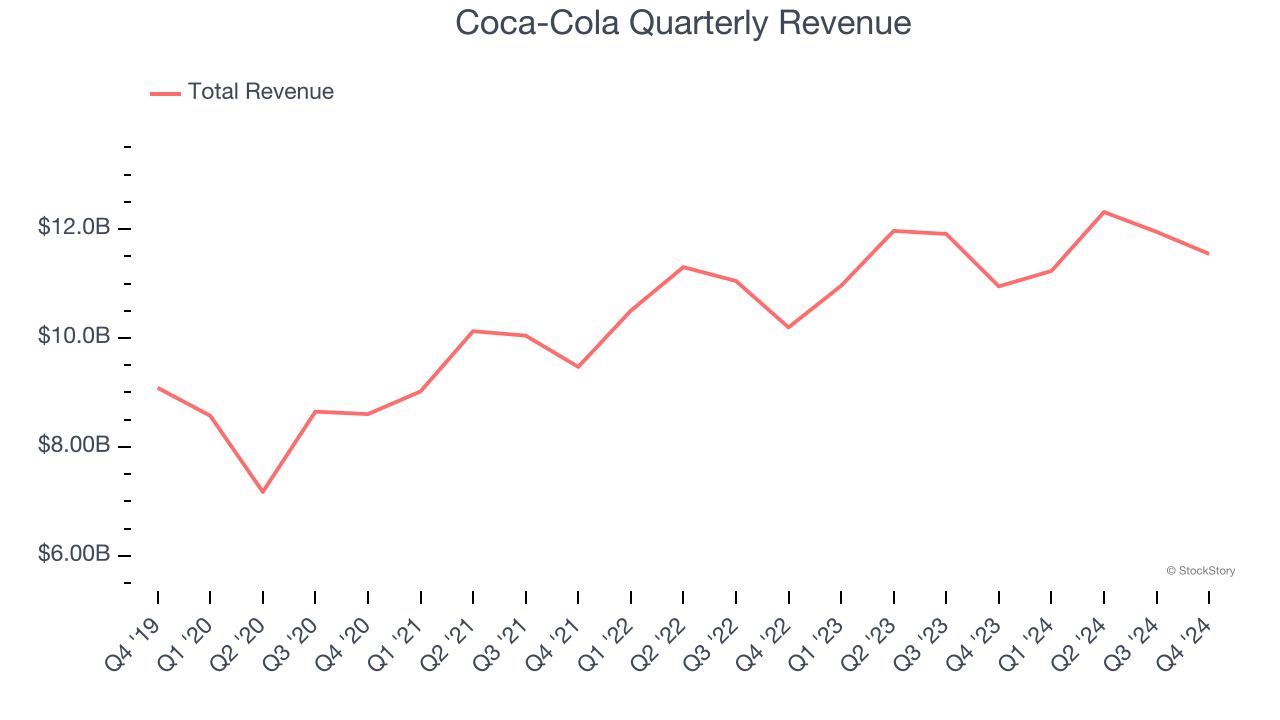

Beverage company Coca-Cola (NYSE: KO) reported Q4 CY2024 results beating Wall Street’s revenue expectations, with sales up 5.4% year on year to $11.54 billion. Its non-GAAP profit of $0.55 per share was 6.4% above analysts’ consensus estimates.

Is now the time to buy Coca-Cola? Find out by accessing our full research report, it’s free.

Coca-Cola (KO) Q4 CY2024 Highlights:

- Revenue: $11.54 billion vs analyst estimates of $10.71 billion (5.4% year-on-year growth, 7.8% beat)

- Adjusted EPS: $0.55 vs analyst estimates of $0.52 (6.4% beat)

- Adjusted EBITDA: $3.27 billion vs analyst estimates of $2.93 billion (28.3% margin, 11.7% beat)

- Operating Margin: 23.5%, up from 20.8% in the same quarter last year

- Free Cash Flow Margin: 27.3%, up from 16.6% in the same quarter last year

- Organic Revenue rose 14% year on year (12% in the same quarter last year)

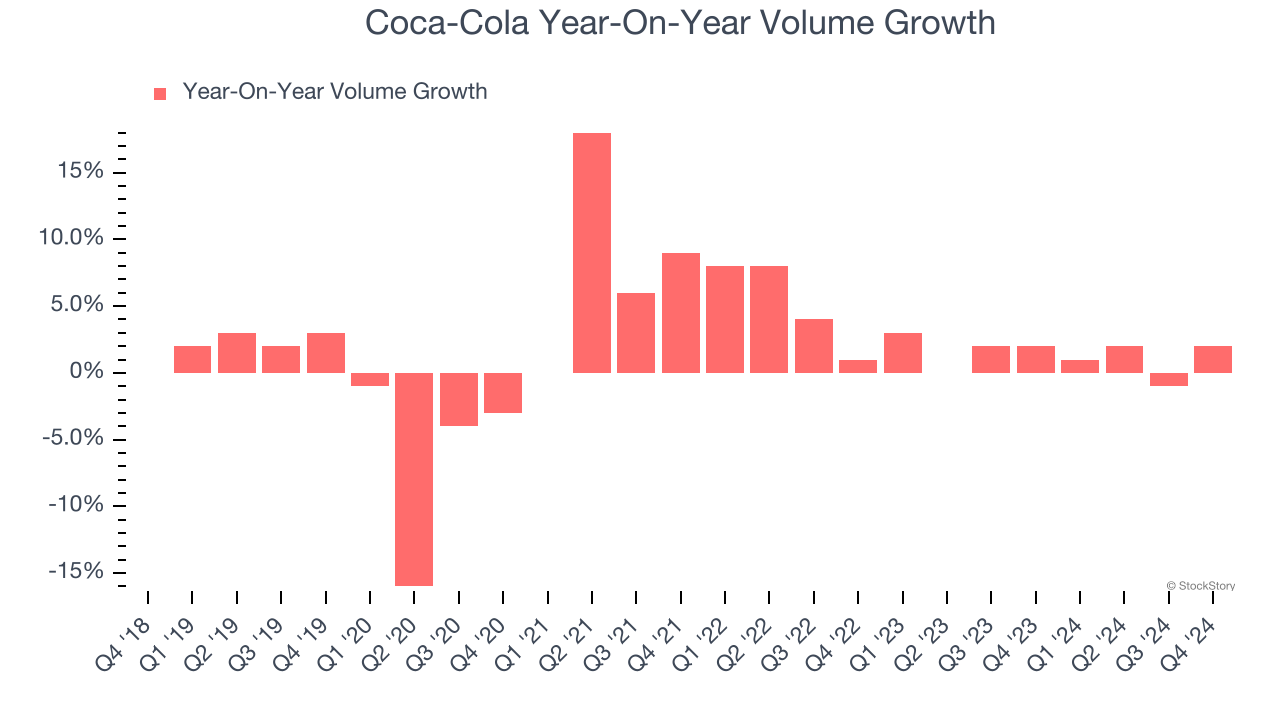

- Sales Volumes rose 2% year on year, in line with the same quarter last year

- Market Capitalization: $278.1 billion

Company Overview

A pioneer and behemoth in carbonated soft drinks, Coca-Cola (NYSE: KO) is a storied beverage company best known for its flagship soda.

Beverages, Alcohol, and Tobacco

These companies' performance is influenced by brand strength, marketing strategies, and shifts in consumer preferences. Changing consumption patterns are particularly relevant and can be seen in the rise of cannabis, craft beer, and vaping or the steady decline of soda and cigarettes. Companies that spend on innovation to meet consumers where they are with regards to trends can reap huge demand benefits while those who ignore trends can see stagnant volumes. Finally, with the advent of the social media, the cost of starting a brand from scratch is much lower, meaning that new entrants can chip away at the market shares of established players.

Sales Growth

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $47.04 billion in revenue over the past 12 months, Coca-Cola is one of the most widely recognized consumer staples companies. Its influence over consumers gives it negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don’t have). However, its scale is a double-edged sword because it's harder to find incremental growth when your existing brands have penetrated most of the market. To accelerate sales, Coca-Cola must lean into newer products.

As you can see below, Coca-Cola grew its sales at a mediocre 6.8% compounded annual growth rate over the last three years, but to its credit, consumers bought more of its products.

This quarter, Coca-Cola reported year-on-year revenue growth of 5.4%, and its $11.54 billion of revenue exceeded Wall Street’s estimates by 7.8%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and implies its products will see some demand headwinds.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

To analyze whether Coca-Cola generated its growth from changes in price or volume, we can compare its volume growth to its organic revenue growth, which excludes non-fundamental impacts on company financials like mergers and currency fluctuations.

Over the last two years, Coca-Cola’s average quarterly volume growth was a healthy 1.4%. Even with this good performance, we can see that most of the company’s gains have come from price increases by looking at its 11.9% average organic revenue growth. The ability to sell more products while raising prices indicates that Coca-Cola enjoys some degree of inelastic demand.

In Coca-Cola’s Q4 2024, sales volumes jumped 2% year on year. This result was an acceleration from its historical levels, certainly a positive signal.

Key Takeaways from Coca-Cola’s Q4 Results

We were impressed by how significantly Coca-Cola blew past analysts’ EBITDA and EPS expectations this quarter. We were also excited its organic revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good quarter with some key areas of upside. The stock traded up 3.3% to $66.69 immediately after reporting.

Coca-Cola put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.