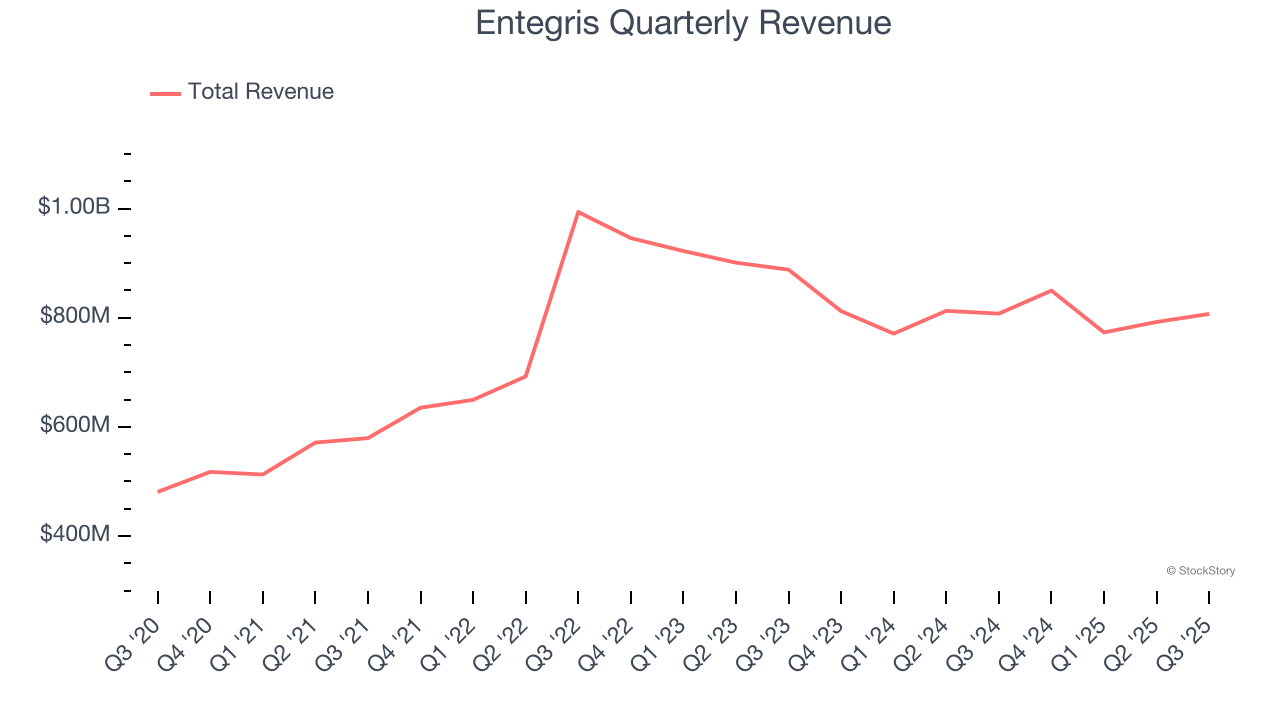

Semiconductor materials supplier Entegris (NASDAQ: ENTG) reported Q3 CY2025 results exceeding the market’s revenue expectations, but sales were flat year on year at $807.1 million. On the other hand, next quarter’s revenue guidance of $810 million was less impressive, coming in 2% below analysts’ estimates. Its non-GAAP profit of $0.72 per share was in line with analysts’ consensus estimates.

Is now the time to buy Entegris? Find out by accessing our full research report, it’s free for active Edge members.

Entegris (ENTG) Q3 CY2025 Highlights:

- Revenue: $807.1 million vs analyst estimates of $802 million (flat year on year, 0.6% beat)

- Adjusted EPS: $0.72 vs analyst estimates of $0.72 (in line)

- Adjusted EBITDA: $220.7 million vs analyst estimates of $223.1 million (27.3% margin, 1.1% miss)

- Revenue Guidance for Q4 CY2025 is $810 million at the midpoint, below analyst estimates of $826.9 million

- Adjusted EPS guidance for Q4 CY2025 is $0.66 at the midpoint, below analyst estimates of $0.76

- Operating Margin: 15.2%, down from 16.9% in the same quarter last year

- Free Cash Flow Margin: 22.6%, up from 14.2% in the same quarter last year

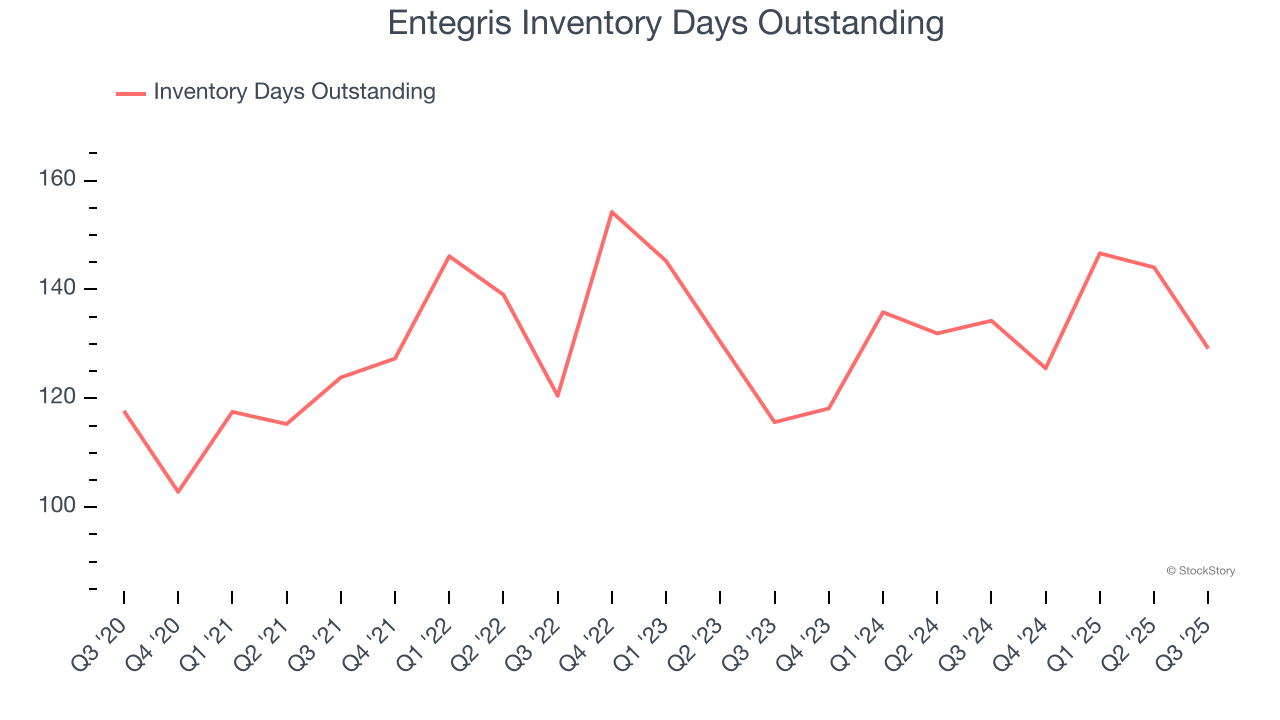

- Inventory Days Outstanding: 129, down from 144 in the previous quarter

- Market Capitalization: $14.33 billion

Dave Reeder, Entegris’ President and Chief Executive Officer, said: “As I begin my tenure as CEO of Entegris, I want to say how honored I am to lead this exceptional company through its next phase of growth and value creation. In the third quarter, revenue, EBITDA and non-GAAP EPS all met guidance; and we delivered record operating cash flow. We continue to see key wins and strong momentum in products critical to the most advanced nodes, including liquid filtration & purification, deposition materials and CMP consumables.”

Company Overview

With fabs representing the company’s largest customer type, Entegris (NASDAQ: ENTG) supplies products that purify, protect, and generally ensure the integrity of raw materials needed for advanced semiconductor manufacturing.

Revenue Growth

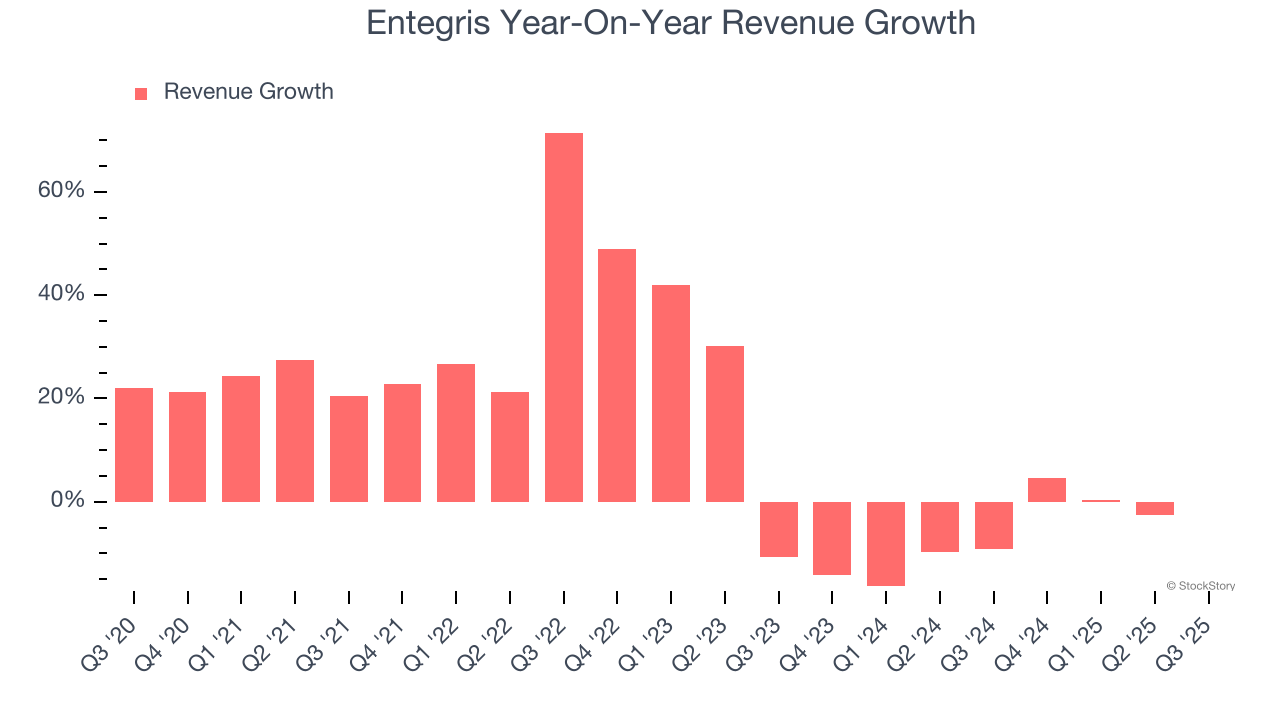

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Entegris’s sales grew at an impressive 12.7% compounded annual growth rate over the last five years. Its growth beat the average semiconductor company and shows its offerings resonate with customers. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. Entegris’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 6.1% over the last two years.

This quarter, Entegris’s $807.1 million of revenue was flat year on year but beat Wall Street’s estimates by 0.6%. Adding to the positive news, Entegris’s flat sales marked an inflection from its revenue decline last quarter, news that will likely give some shareholders hope. Company management is currently guiding for a 4.7% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.6% over the next 12 months. While this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Entegris’s DIO came in at 129, which is one day below its five-year average. At the moment, these numbers show no indication of an unusual inventory buildup.

Key Takeaways from Entegris’s Q3 Results

We were impressed by Entegris’s strong improvement in inventory levels. On the other hand, its revenue guidance for next quarter missed and its EPS was in line with Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 2.1% to $92.65 immediately after reporting.

Entegris may have had a tough quarter, but does that actually create an opportunity to invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.