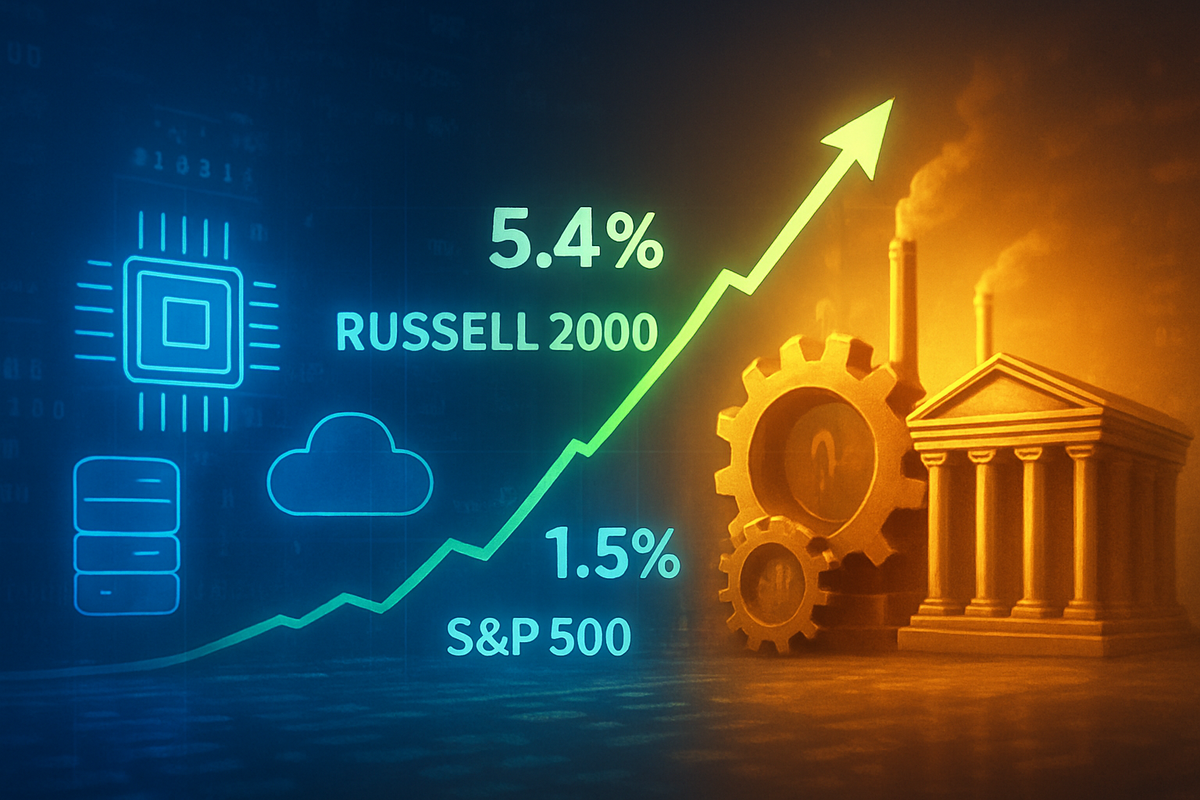

The financial markets have reached a historic fever pitch in early 2026, marking what analysts are now calling the "Great Rotation." After years of dominance by a handful of silicon giants, the tide has officially turned. As of February 24, 2026, the Russell 2000 Index, the benchmark for small-cap American companies, has surged a staggering 5.4% since the start of the year. In stark contrast, the S&P 500 (NYSEARCA:SPY)—long the darling of the bull market—has managed a meager 1.5% gain, weighed down by cooling sentiment in the mega-cap technology sector.

This decoupling represents more than just a brief rally; it is a fundamental reordering of the American investment landscape. For the first time in over half a decade, the "median stock" is outperforming the index heavyweights. Institutional capital is flowing out of overextended AI plays and into domestic cyclicals, regional banks, and industrial manufacturers. This shift signals a market that is finally looking past the speculative promise of artificial intelligence and toward the tangible growth of the broader U.S. economy.

A Springboard of Value: The Timeline of the Turnaround

The roots of this rotation can be traced back to the closing months of 2025. As the Federal Reserve successfully navigated the "soft landing," lowering the Federal Funds Rate to its current range of 3.50%–3.75%, the cost of capital for smaller firms began to plummet. Throughout late 2025, while the "Magnificent Seven" saw their valuations stretch to historic extremes, the Russell 2000 remained a "coiled spring," trading at a forward price-to-earnings multiple of just 18x compared to the S&P 500's 22x+.

The breaking point arrived in January 2026, during the fourth-quarter earnings season. While tech behemoths like NVIDIA (NASDAQ: NVDA) and Microsoft (NASDAQ: MSFT) posted solid results, their guidance failed to satisfy a market that had priced in perfection. Simultaneously, small-cap companies showed surprising resilience, with nearly 65% of the index components beating earnings expectations. This "earnings handoff" convinced skeptical fund managers that the profit growth narrative had finally broadened beyond the software and semiconductor sectors, sparking the 5.4% surge we see today in the iShares Russell 2000 ETF (NYSEARCA:IWM).

Winners and Losers: The New Market Hierarchy

The primary beneficiaries of this rotation are the companies tied to the domestic economy. Regional banks, which were battered during the volatility of 2023 and 2024, are seeing a renaissance as the yield curve stabilizes. Five Star Bancorp (NASDAQ: FSBC) and Northeast Bank (NASDAQ: NBN) have emerged as top performers, benefiting from a pickup in commercial lending and improved net interest margins. These firms are thriving as the "neutral" interest rate environment allows for more predictable lending cycles, a far cry from the "higher for longer" era that pressured their balance sheets.

On the industrial front, the "One Big Beautiful Bill Act" of 2025 has provided a massive tailwind. Small and mid-cap manufacturers like Gorman-Rupp (NYSE: GRC) and Donaldson Company (NYSE: DCI) are seeing record order backlogs as domestic infrastructure projects and reshoring initiatives move into high gear. Conversely, the "losers" in this environment are the high-growth, high-valuation tech firms that lack the domestic insulation of the Russell 2000. Companies heavily reliant on global supply chains or Chinese consumer demand are finding themselves out of favor as investors prioritize the safety of the U.S. consumer and domestic industrial productivity. Even aerospace suppliers like Hexcel (NYSE: HXL) are finding new life as the aviation sector’s recovery finally trickles down to specialized material providers.

The Macro Engine: Analyzing the Significance

This event signifies a departure from the "era of concentration" that defined the early 2020s. Historically, such rotations occur when the market enters a period of synchronized global growth or when a dominant sector reaches a valuation ceiling. The current shift reflects both. The AI infrastructure buildout, which fueled the S&P 500 for years, has moved into its "implementation phase," where the winners are no longer just the chipmakers, but the companies using the technology to drive efficiency in the real world—most of which reside in the small and mid-cap space.

Furthermore, the policy implications are significant. The 2025 legislative focus on 100% bonus depreciation and immediate R&D expensing has effectively acted as a stimulus package for the Russell 2000. This fiscal support, combined with a Federal Reserve that is no longer in "inflation-fighting" mode but rather "growth-sustaining" mode, creates a Goldilocks environment for domestic cyclicals. We are seeing a rare alignment where monetary and fiscal policy are both tilting the scales in favor of Main Street over Silicon Valley, a dynamic not seen with this intensity since the mid-2000s.

The Road Ahead: Short-Term Gains or Long-Term Trend?

Looking forward, the critical question is whether this 5.4% surge is a temporary "mean reversion" or the start of a multi-year bull market for small-caps. In the short term, the market is pricing in at least two more rate cuts in 2026, which would likely push the Russell 2000 toward the 20% gain mark projected by some analysts. However, the path is not without risks. Any resurgence in inflation or a sudden spike in energy costs could disproportionately hurt smaller companies that have less pricing power than their mega-cap counterparts.

Strategic pivots will be required for institutional investors who have spent years "overweighting" tech. We expect to see a continued rebalancing of portfolios through the end of the second quarter, as managers chase the momentum of the Russell 2000. For the companies themselves, the challenge will be managing the rapid influx of capital. Small-cap firms that have lived in a "survival mode" for years must now pivot to "growth mode," scaling operations to meet the demands of a resurgent domestic economy.

A New Market Regime: Final Thoughts

The "Great Rotation" of 2026 marks the end of an era. The dominance of a few tech giants has given way to a healthier, broader market where thousands of companies—not just seven—are driving the American economy forward. The 5.4% surge in the Russell 2000 versus the 1.5% in the S&P 500 is the clearest signal yet that the market’s center of gravity has shifted.

As we move deeper into 2026, investors should keep a close watch on regional banking health and manufacturing PMI data. If these domestic engines continue to fire, the Russell 2000’s outperformance may not just be a highlight of the first quarter, but the story of the decade. The message from the market is clear: the most exciting opportunities are no longer found in the cloud, but on the factory floors and in the local banks of Middle America.

This content is intended for informational purposes only and is not financial advice.