The pressure will be on when Apple reports its latest quarterly results after the bell on May 4th. Better-than-expected earnings at fellow trillion-dollar market club members Alphabet and Microsoft have led equities back to their 2023 peak — and set the stage for Apple to send the market to new heights.

Investors’ obsession with these three companies is for good reason. Together they account for more than $7 trillion of stock market value and 17% of the widely followed S&P 500. Their collective performances have a tremendous impact on benchmarks, exchange traded funds (ETFs) and personal portfolio values.

Just because they carry the most clout in the global equity market, however, doesn’t mean they have the most upside.

There are approximately 50 mega-cap companies that aren’t named Apple, Microsoft or Alphabet. The vast majority don’t reside in the technology sector. From e-commerce leaders to drug manufacturers, the fundamentals of many of these companies are on par if not better than the so-called ‘MAMAA’ stocks (which adds Amazon and Meta Platforms to the trillion-dollar trio).

According to Wall Street research groups, it is these three mega caps that will have the biggest gains over the next 12 months.

Which Mega Cap Stock Has the Most Upside?

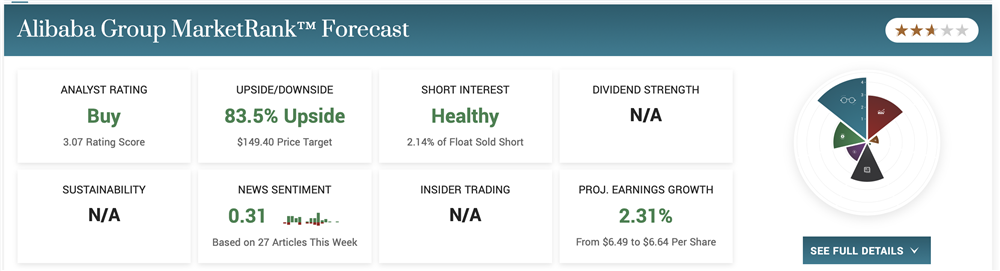

Alibaba Group Holding Limited (NYSE: BABA) has by far the most upside of any of the mega caps in the opinion of sell-side analysts. China’s e-commerce giant boasts 78% return potential over the next year based on more than a dozen firms that closely follow the stock. The Street is unanimously bullish on Alibaba, which is something Apple and Microsoft can’t claim (but Alphabet can).

Why are analysts so excited about Alibaba? For one, the Chinese economy appears to be well on its way to recovery. First quarter gross domestic product (GDP) growth was a better-than-expected 4.5% led by a strong rebound in consumer spending.

Second, Alibaba’s plan to split into six separate business units has the potential to unlock value. Cloud and other segments outside of the core commerce business should have greater autonomy and flexibility to pursue growth initiatives. While the plan is to keep everything under one roof for now, management has suggested that split-off IPOs may be in the future.

Make no mistake, though, it is Alibaba’s massive retail footprint that is leading the charge. Domestic and international commerce combined made up 76% of company sales last year. Alibaba’s dominance at home and steps to derive growth from the U.S. and other international markets is the main reason analysts are expecting strong financial results.

What Could Drive Gains in Taiwan Semiconductor Shares?

Taiwan Semiconductor Manufacturing Company Limited (NYSE: TSM) is recovering nicely from its November 2022 low, but analysts think there’s more room to run. The chipmaker has a consensus price target of around $119, which implies more than 40% upside. Like Alibaba, all firms that cover Taiwan Semiconductor currently have buy ratings.

Last month, the company beat the Street’s earnings forecast, demonstrating resilience in a tough macro environment. Although inventory pileups and soft-end market demand drove a 5% revenue decline, Taiwan Semi continued to see strong interest in its new 5 nanometer chips for smartphones and other electronic devices. Legacy product sales also held up well, thanks to improving demand from automotive and industrial customers.

Customer inventory adjustments are expected to wind down in the coming months, which could lead to easier year-over-year comparisons and a return to top-line growth in the back half of 2023. Beyond that, Taiwan Semi is expected to benefit from global digitization trends that will make digital technologies a bigger part of our everyday lives — and entail a growing need for the company's semiconductor products.

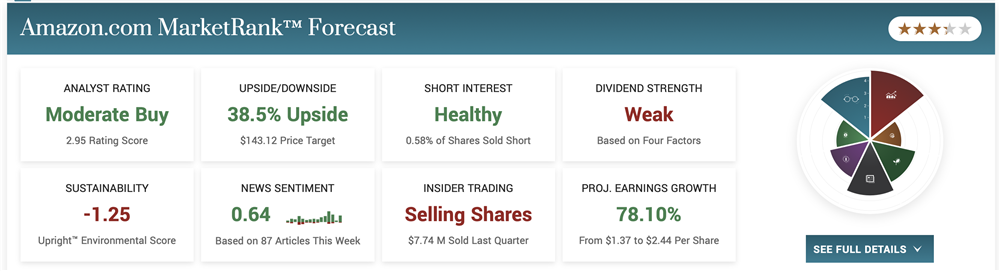

Is Amazon’s Stock Weakness an Opportunity?

Amazon.com (NASDAQ: AMZN) has the third-best return potential, according to Wall Street. This is telling, considering the stock is already up about 25% from its recent low. The uptrend should persist, according to analysts who have been praising the company’s Q1 double beat and healthy Q2 guidance.

The market has disagreed since the Q1 release, however, focusing instead on slower growth in the AWS cloud business. Sales in the key profit center have come well off their torrid pandemic pace because of weaker economic conditions. But with the global cloud transformation only on pause, analysts believe Amazon’s share price weakness is an opportunity.

Like other mega-cap industry leaders, Amazon has been forced to eliminate jobs in its core online shopping business. This reflects management’s cautious view on consumer activity even as signs of improvement emerge. As with the AWS though, these challenges should be temporary and lend way to the bigger trend — the ongoing global shift from brick-and-mortar to e-commerce retail.