The TJX Companies, Inc. (TJX) is the world’s largest off-price apparel and home fashions retailer, operating a global network of value-oriented chains including T.J. Maxx, Marshalls, HomeGoods, Homesense, and international banners such as TK Maxx and Winners. Headquartered in Framingham, Massachusetts, TJX purchases branded and designer merchandise opportunistically from manufacturers and department stores, then sells it at significant discounts to full-price retail through a high-turnover, treasure-hunt shopping model.

Companies valued over $10 billion are generally described as “large-cap” stocks, and TJX, with a market capitalization of $173 billion, fits right into that category. The company is positioned as a defensive, cash-generative retail leader with durable traffic, strong vendor relationships, and consistent same-store sales execution. It competes on price, assortment freshness, and brand discovery rather than private-label dominance or e-commerce scale. Its off-price model tends to outperform in uncertain economic environments, as consumers trade down while brands seek efficient channels to clear excess inventory.

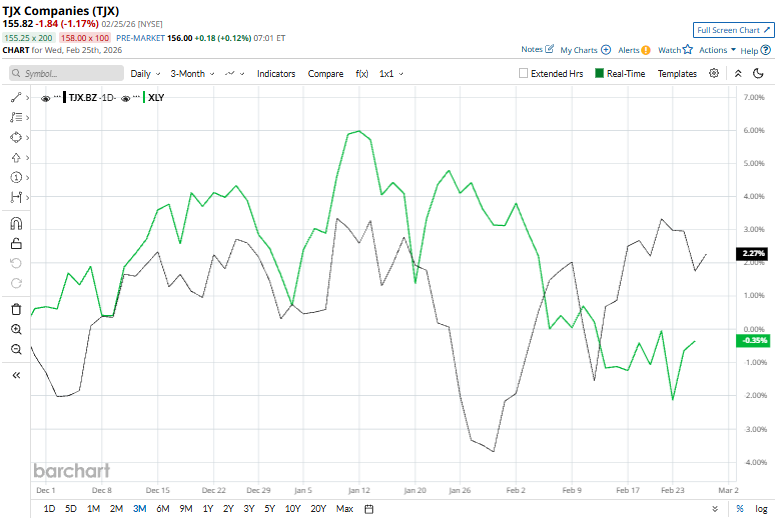

TJX shares climbed to a fresh 52-week high of $162.68 in the last trading session. It has surged 2.3% over the past three months, outpacing the State Street Consumer Discretionary Select Sector SPDR Fund’s (XLY) marginal uptick.

Over the past year, the off-price retail leader has delivered a 27% gain and is up 1.4% in 2026, comfortably outperforming the ETF’s 8.2% 12-month return and 1.9% year-to-date decline.

Technically, the stock has spent most of the past year trading above its 200-day moving average and has moved past its 50-day moving average early this month, signaling persistent upward bias and underlying trend strength.

On Feb. 25, TJX posted its fiscal 2026 Q4 results, and its shares dipped 1.2%. Its revenue rose 8.5% year over year to about $17.7 billion, and adjusted EPS of $1.43, both ahead of Wall Street expectations. Comparable sales grew 5%, exceeding forecasts, with gains across all divisions as the off-price model continued to attract value-focused shoppers and drive market-share gains. Its profit also improved meaningfully, reflecting solid merchandise margins and expense discipline. Despite the upbeat quarter, management issued conservative FY2027 guidance, tempering near-term expectations even as the company maintained strong underlying momentum.

Top rival, Ross Stores, Inc. (ROST) has climbed 47.7% over the past 52 weeks and gained 11.9% in 2026, far exceeding TJX’s return over the same time frames.

Nevertheless, Wall Street analysts are strongly bullish on TJX’s stock. The stock has a consensus rating of “Strong Buy” from the 20 analysts covering it. The mean price target of $170.20 implies a 9.2% upside from current levels. Moreover, the Street-high price target of $193 indicates an 23.9% upside.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart