Nvidia (NVDA) delivered another set of record-breaking financial results, underscoring its commanding position in the artificial-intelligence infrastructure boom. The company posted robust revenue and earnings growth while issuing upbeat guidance that highlighted sustained demand for its cutting-edge GPUs and accelerated computing platforms.

Management emphasized expanding adoption across hyperscalers, enterprises, sovereign nations, and emerging agentic AI applications, painting a picture of durable fundamentals and long-term leadership in the AI ecosystem. Yet the market’s muted reaction—shares barely budged after hours and have dipped over 4% today—raises an important question: are investors beginning to price in perfection, or do deeper structural concerns lurk beneath the surface of these stellar numbers?

Nvidia Trounces Estimates

Nvidia’s fiscal fourth-quarter results, released after the market closed yesterday, once again shattered Wall Street expectations. Revenue reached $68.1 billion, topping consensus estimates of approximately $66.2 billion and surging 73% year-over-year (YoY) while rising 20% sequentially. Data Center revenue—the company’s core growth engine—hit a record $62.3 billion, up 75% from the prior year. Non-GAAP earnings per share came in at $1.62, comfortably ahead of the $1.53 forecast. For the full fiscal 2026 year, revenue totaled $215.9 billion, a 65% increase.

Looking ahead, management guided fiscal first-quarter 2027 revenue to $78 billion, plus or minus 2%, well above the Street’s $72.6 billion consensus. Gross margins are expected to remain strong at roughly 75% on a non-GAAP basis. The company also highlighted accelerating investments in next-generation platforms. Chief among them was the unveiling of the Vera Rubin architecture, featuring six new chips promising up to 10x lower inference token costs and 50x better performance for agentic AI workloads.

Additional launches included the BlueField-4 data processing unit, open models for AI weather forecasting and autonomous vehicles, and expanded partnerships with major cloud providers for Rubin deployment. Sovereign AI initiatives more than tripled to over $30 billion for the year, while enterprise demand for agentic systems was described as “skyrocketing.” The report contained no new major contract wins but reinforced broad-based momentum across customer segments, with no signs of demand softening despite earlier AI fatigue concerns.

Is This What Investors Are Worried About?

Beneath the impressive top-line growth lies a customer base that remains heavily concentrated among a handful of giants. During the earnings conference call, CFO Colette Kress noted that Nvidia’s top five customers—primarily cloud service providers and hyperscalers—account for over 50% of total revenue. One prominent analyst, Deepwater Asset Management’s Gene Munster, has estimated that the top eight customers represent as much as 80% of the company’s business. This level of reliance on a small group of buyers has long fueled skepticism, especially amid recurring criticisms of “circular financing,” where hyperscalers effectively fund one another’s AI buildouts through mutual purchases and infrastructure sharing.

Compounding these concentration risks is a broader sense of AI fatigue among some market participants. After years of explosive gains, many investors wonder whether the extraordinary results are now fully priced into Nvidia's $4.8 trillion market capitalization. With shares having delivered multibagger returns in recent years, expectations for further dramatic upside appear limited.

The market’s tepid response to the earnings beat suggests that even outsized beats and raised guidance are increasingly taken for granted. At current valuations, any hint of deceleration in hyperscaler spending, regulatory scrutiny, or macroeconomic slowdown could trigger meaningful volatility.

Critics also point to the potential for margin pressure as competition intensifies from custom silicon offerings by the very hyperscalers Nvidia serves. While management remains confident in its technology moat and the expanding total addressable market for accelerated computing, the combination of customer concentration, lofty expectations, and a maturing AI investment cycle has left the stock range-bound in recent months. Absent fresh catalysts or evidence of meaningful revenue diversification, NVDA may continue trading within a relatively narrow band until the next leg of AI infrastructure spending materializes or new growth avenues gain greater traction.

In short, the concerns are less about the current quarter’s performance and more about whether the exceptional performance can remain exceptional indefinitely at this scale.

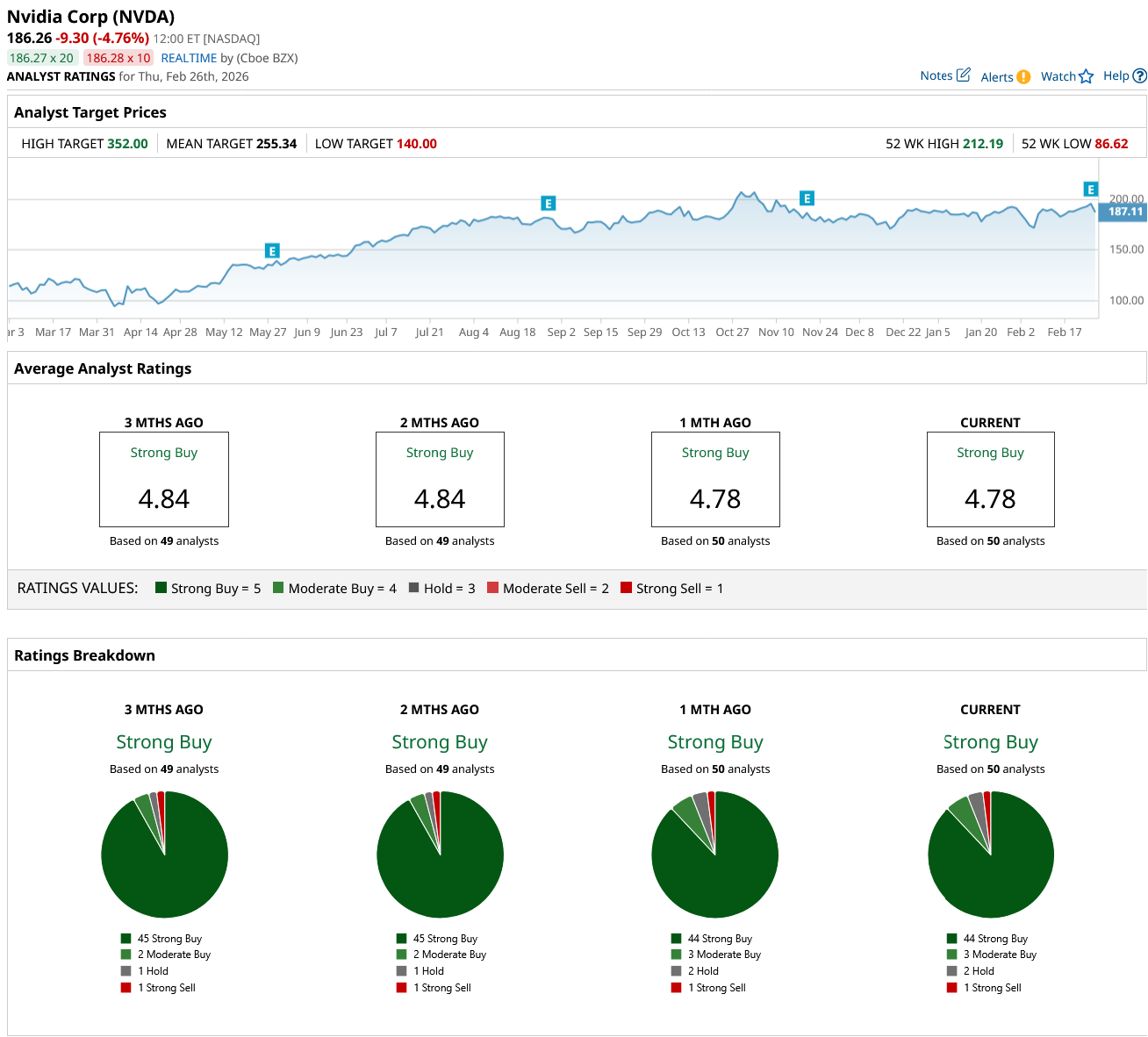

What Do Analysts Expect For NVDA Stock

Wall Street remains overwhelmingly bullish on Nvidia despite the recent valuation debate. According to Barchart’s internal analyst ratings page, the consensus stands at a "Strong Buy" 4.78 based on coverage from 50 analysts. The breakdown reflects broad optimism, with 44 "Strong Buy" ratings, three "Moderate Buy," two "Hold" and one "Strong Sell" rating. No major downgrades have occurred in recent months, but a handful of firms have tempered near-term enthusiasm while maintaining long-term buy ratings.

Barchart’s mean price target sits at $255.34, representing a potential upside of 30%. That figure incorporates Street-high targets approaching $352 and lows near $140, underscoring a wide dispersion of views but an overall constructive stance. Analysts continue to emphasize Nvidia’s secular tailwinds in AI, with many highlighting the Vera Rubin ramp and expanding software ecosystem as key upside drivers for fiscal 2027 and beyond. While the consensus has not shifted post-earnings dramatically, the slight softening in average rating from 4.84 to 4.78 out of 5 suggests growing awareness that sustained outperformance will require not just beats but accelerating growth narratives to justify the premium multiple.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- C3.ai Plummets 20% After Earnings. Should You Buy the Dip in AI Stock Now?

- Is Instacart Stock a Buy, Hold or Sell Now?

- Netflix’s Unusual Options Activity: Was It the Bullish Signal Investors Were Waiting For or a Dead Cat Bounce?

- This ETF Is Up 30% Since November. Is the Rally Over or Is There More Room To Run?