Nvidia (NVDA) delivered an exceptionally strong fourth quarter, beating expectations on both revenue and profit. Top-line growth accelerated from prior quarters, and earnings surged as demand for its artificial intelligence (AI) chips continued to expand across multiple markets.

Nvidia’s revenue growth is being driven primarily by its data center segment. Demand remains robust across a broad customer base that includes hyperscalers, major cloud service providers, AI model developers, large enterprises, and even national governments building sovereign AI infrastructure.

A key catalyst has been Nvidia’s next-generation Blackwell architecture, which is witnessing strong adoption. Further, management guided for continued sequential revenue growth throughout calendar 2026. That outlook signals that demand isn’t slowing. Importantly, AI infrastructure investment from large cloud providers and hyperscalers, which together account for over half of its data center revenue, has increased materially, indicating strong growth ahead.

Nvidia’s stronger-than-expected Q4 performance against elevated expectations, diversified demand, increasing AI infrastructure spending, and upbeat forward guidance strengthens its investment case and indicates further upside in the stock.

Nvidia to Gain from Solid Demand Momentum

Nvidia is set to deliver solid growth ahead and offers strong visibility into future revenue, driven largely by continued demand for AI infrastructure. In the fourth quarter, Nvidia generated $68 billion in total revenue, a 73% increase from the same period last year. Growth also accelerated from the prior quarter, with the company adding $11 billion in incremental data center revenue sequentially.

The data center segment remains the core engine. Fourth-quarter data center revenue reached $62 billion, up 75% year-over-year (YoY) and 22% sequentially. Demand has been especially strong for Nvidia’s Blackwell architecture and the newer Blackwell Ultra systems, which are designed for large-scale AI training and inference workloads. As more companies deploy AI models into real-world applications, the need for inference computing power is rising alongside traditional training demand.

The broader shift toward accelerated computing continues to support Nvidia’s outlook. Hyperscale cloud providers are embedding AI into existing services, and enterprises are deploying more advanced, multimodal AI systems. Applications such as agentic AI systems and physical AI used in robotics and automation are beginning to contribute meaningfully to revenue. These trends suggest that AI adoption will remain strong, supporting Nvidia’s investment case.

Nvidia expects revenue to continue rising quarter after quarter throughout calendar 2026, surpassing the projections tied to the $500 billion Blackwell and Rubin revenue opportunity it outlined last year. Importantly, the company has secured supply commitments and inventory to support demand that already extends into calendar year 2027, which provides visibility into future growth.

Another emerging growth driver is sovereign AI. Governments around the world are investing in domestic AI infrastructure to support national competitiveness and data sovereignty. In fiscal 2026, Nvidia’s sovereign AI-related revenue more than tripled YoY to exceed $30 billion. As more countries allocate capital to AI infrastructure, this segment could become an increasingly significant contributor.

For the first quarter, Nvidia expects revenue of approximately $78 billion, up 77% YoY, with data center sales again accounting for the majority of the growth. Further, analysts project Nvidia to report earnings of $1.55 per share in Q1, up 101.3% YoY.

Rising demand, the rapid expansion of AI applications across industries, and long-term supply agreements together create a strong foundation for Nvidia’s continued growth in the coming quarters. These factors will likely provide meaningful support to its share price.

How High NVDA Stock Could Go?

Nvidia has climbed more than 41% over the past year, reflecting strong investor confidence in its growth trajectory. Despite that run-up, the stock’s valuation remains relatively attractive. NVDA stock is trading at a forward price-to-earnings ratio of 27.2, which appears reasonable given analysts’ expectation that earnings per share will grow by 59.5% in fiscal 2027.

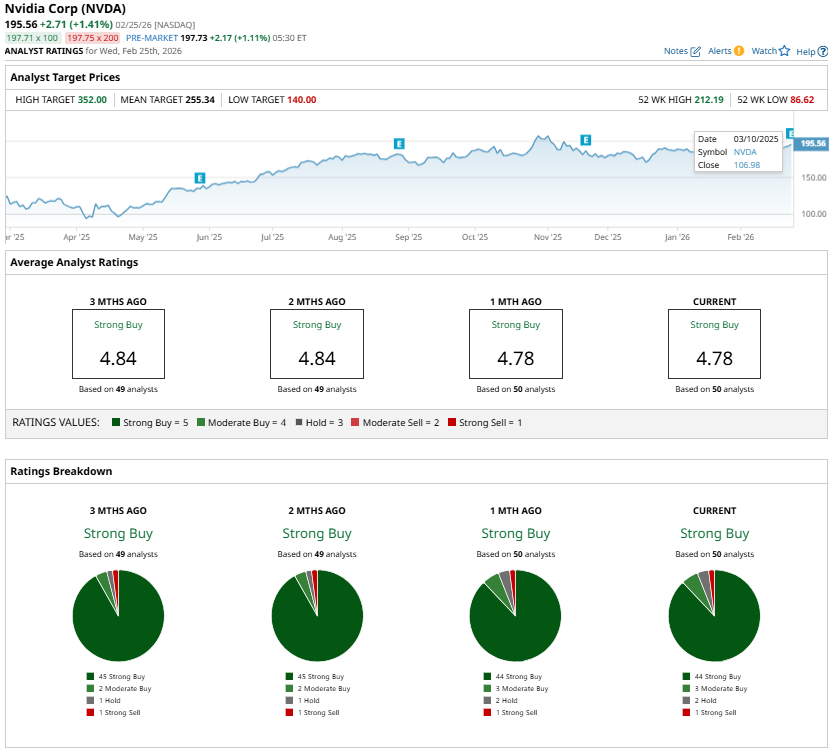

Wall Street’s average price target for NVDA stock stands at $255.34. Compared with its closing price of $195.56 on Feb. 25, this implies roughly 31% potential upside over the next 12 months. Analysts overall continue to rate the stock a “Strong Buy.”

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart