Small-cap stocks rarely receive the limelight they deserve. A handful of small-cap companies are quietly laying the groundwork for long-term success. They are expanding market share, improving profitability, and scaling their business models while most investors ignore them for the short-term volatility.

With a market cap of $2.07 billion, Alphatec Holdings (ATEC) is one such small-cap stock that investors may regret not buying 10 years from now.

Let’s find out why.

A Spine Company Built With Singular Focus

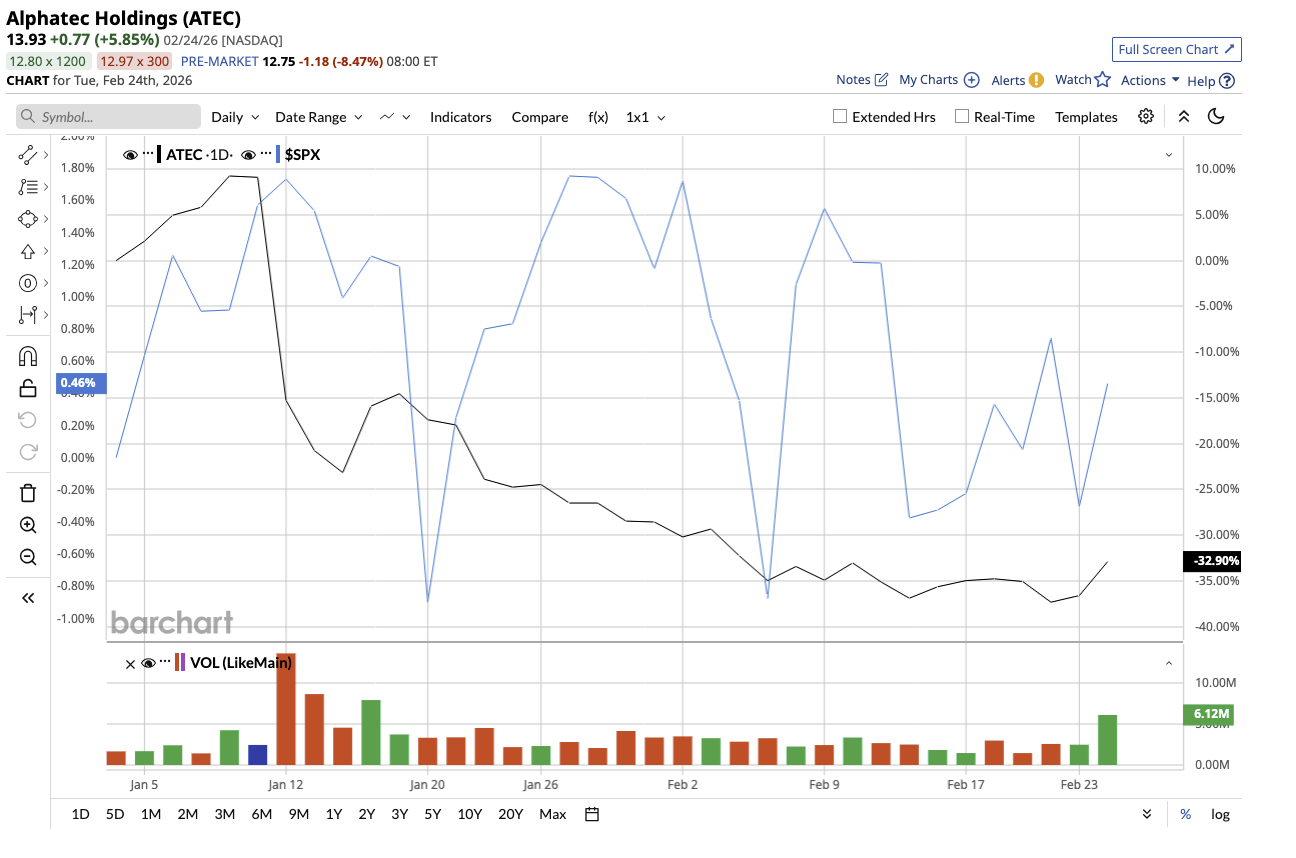

Alphatec is completely focused on spine surgery, a massive and still-evolving market. It has built an integrated ecosystem of implants, imaging, navigation, and data-driven surgical tools aimed at simplifying complex spinal procedures. ATEC stock has dipped 34% so far this year, compared to the S&P 500 Index’s ($SPX) modest gain of 0.5%.

While larger, established MedTech giants like Intuitive Surgical (ISRG), Medtronic (MDT), Stryker (SYK), and Johnson & Johnson (JNJ) offer a more varied portfolio of products, Alphatec has chosen to focus 100% on just one area—the spine. That strategy appears to be working. The company reported its fourth quarter and full year 2025 results on Tuesday. For Q4, Alphatec reported $213 million in revenue, up 20% year-over-year (YoY). Surgical revenue grew 21% in the quarter, supported by 21% procedural volume growth and a 23% increase in net new surgeon users.

For the full year, surgical revenue reached $687 million, up 26% from 2024, driven by 22% procedural volume growth and 3% growth in average revenue per procedure. EOS imaging revenue contributed an additional $77 million, growing 15% YoY. Total revenue for the year increased 25% YoY to $764 million, driven by surgeon adoption, rising utilization, and expanding procedural complexity.

Management stressed the company’s predictable adoption model, wherein new surgeons begin with lateral procedures and, over time, expand utilization across additional techniques. This reveals Alphatec has built a consistent, multi-year ramp pattern in surgeon usage, resulting in ongoing growth without relying only on new additions. What makes Alphatec a compelling buy now is that profitability is scaling along with revenue. The company reported its third profitable quarter with $9 million in adjusted net income. For the full year, the company reported adjusted net income of $8 million, compared to a loss in 2024. Gross margin held steady at roughly 70%. Importantly, while it continues investing heavily in instruments and inventory to support growth, it generated $3 million in free cash flow for the full year. Management expects at least $20 million in free cash flow in 2026 while maintaining aggressive growth investment. On the balance sheet, the company had $161 million in cash.

For an emerging medical device company, the shift from capital consumption to capital generation is a significant achievement. It highlights maturity in operations and confidence in the sustainability of demand.

Alphatec’s integrated ecosystem is its biggest factor contributing to the high growth. Notably, its EOS technology combines standing full-body weight-bearing imaging, automatic alignment measurements, and bone mineral density monitoring in a single platform. Furthermore, SafeOp neuromonitoring and the Valence navigation and robotics technology are intended to fit seamlessly into spinal procedural workflows. Management claims that, whereas most rivals focus primarily on implants, Alphatec proceduralizes the entire surgical process. These factors result in higher switching costs and stronger surgeon ties, which give Alphatec a competitive edge.

Looking ahead, Alphatec expects 2026 revenue of approximately $890 million, representing 17% growth. Surgical revenue is projected to be around $805 million, with EOS revenue potentially being roughly $85 million.

Why a Decade Matters

No doubt, like any growing company, Alphatec might have some hiccups in the short term, and the stock will likely be volatile. However, Alphatec is no longer a cash-burning early-stage healthcare company. It is a scaled business with improved profitability, increased cash generation, and a unique in-depth business model. With minimally invasive and robotic surgeries rising in demand, healthcare will look very different ten years from now.

The spinal implants and surgery devices market is estimated to generate revenue worth $16 billion by 2032. With an early-mover advantage and profound knowledge of spinal surgery solutions, Alphatec will have an upper hand. For those willing to think long-term and with a high-risk appetite, this may be the kind of stock you simply do not regret owning.

What Does Wall Street Say About ATEC Stock?

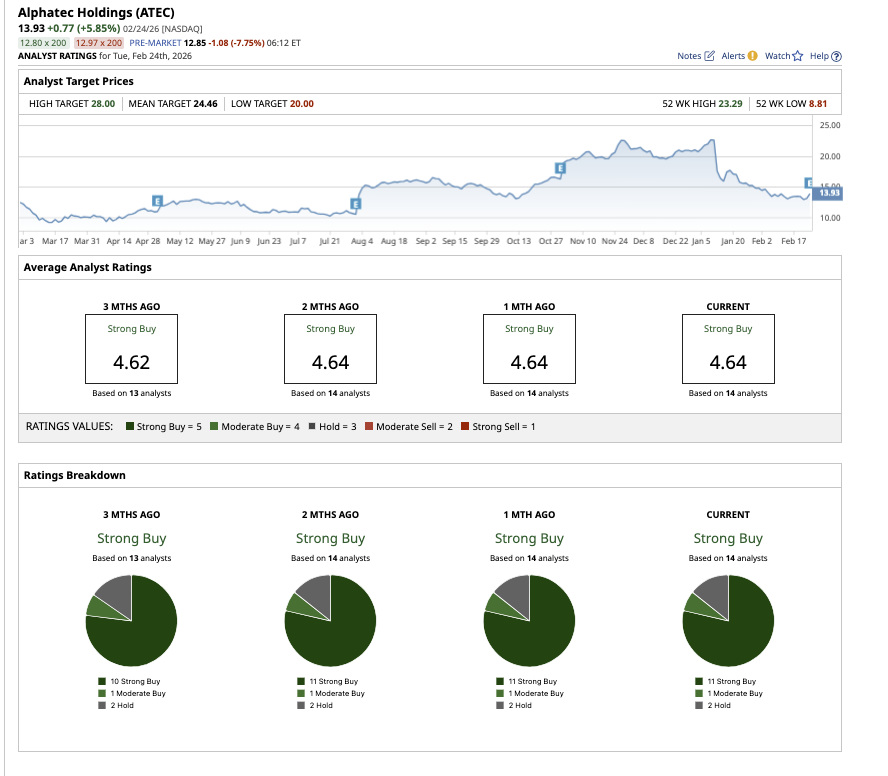

On Wall Street, ATEC stock has garnered an overall “Strong Buy” rating. Of the 14 analysts covering ATEC, 11 have rated it a “Strong Buy,” one recommends a “Moderate Buy,” and two say it is a “Hold.” Based on its mean price target of $24.46, Wall Street expects the stock to climb as high as 76% from current levels. Furthermore, its high target price of $28 implies a potential upside of nearly 101% in the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart