Uranium is back in the spotlight once again. The world is leaning harder on nuclear power to support clean energy goals, grid stability, and rising electricity demand from artificial intelligence (AI)-driven data centers. But just as nuclear momentum builds, the fuel behind it is facing pressure.

A looming supply crunch in enriched uranium, tighter Western supply chains, and restrictions on Russian imports are creating a structural imbalance, as per Centrus Energy (LEU) CEO Amir Vexler. Consequently, spot uranium prices have jumped sharply in 2026, crossing $100 per pound and signaling renewed strength in the commodity cycle.

Demand is expanding beyond existing reactors. New large-scale plants and small modular reactors are in development, adding longer-term strain to an already tight enrichment market. Policy support is firm, capital is rotating upstream, and supply additions remain slow.

As per the CEO, meaningful relief in the enrichment market is unlikely before the next wave of large-scale capacity comes online, a process that could stretch well into the next decade, and until then, tight supply conditions may persist. Amid this constrained landscape, Centrus holds a strategic advantage as one of only two licensed U.S. enrichment providers. It is expanding capacity at its Ohio facility to support a multibillion-dollar order backlog.

With LEU stock trading significantly below its recent highs, investors may consider buying the stock as current levels could offer a compelling entry point into a supply-constrained uranium market.

About Centrus Energy Stock

Just like its ticker, Centrus Energy is all about LEU—low enriched uranium—the essential fuel that keeps nuclear reactors running. The Bethesda, Maryland-based company, with a market capitalization of roughly $4 billion, plays a critical role in the nuclear supply chain. It operates through two main segments—LEU, which provides fuel and enrichment services to utilities, and Technical Solutions, which delivers advanced engineering and manufacturing support to government and commercial customers.

Since 1998, Centrus has supplied more than 1,850 reactor years of fuel—equivalent to replacing over 7 billion tons of coal. At its core, the company enriches uranium hexafluoride gas to increase the concentration of uranium-235, the isotope needed for nuclear fuel pellets.

Its Oak Ridge, Tennessee, facility builds advanced centrifuge machines, which are deployed at its Piketon, Ohio, plant to produce both LEU and high-assay low-enriched uranium (HALEU)—a next-generation fuel designed for smaller, advanced reactors.

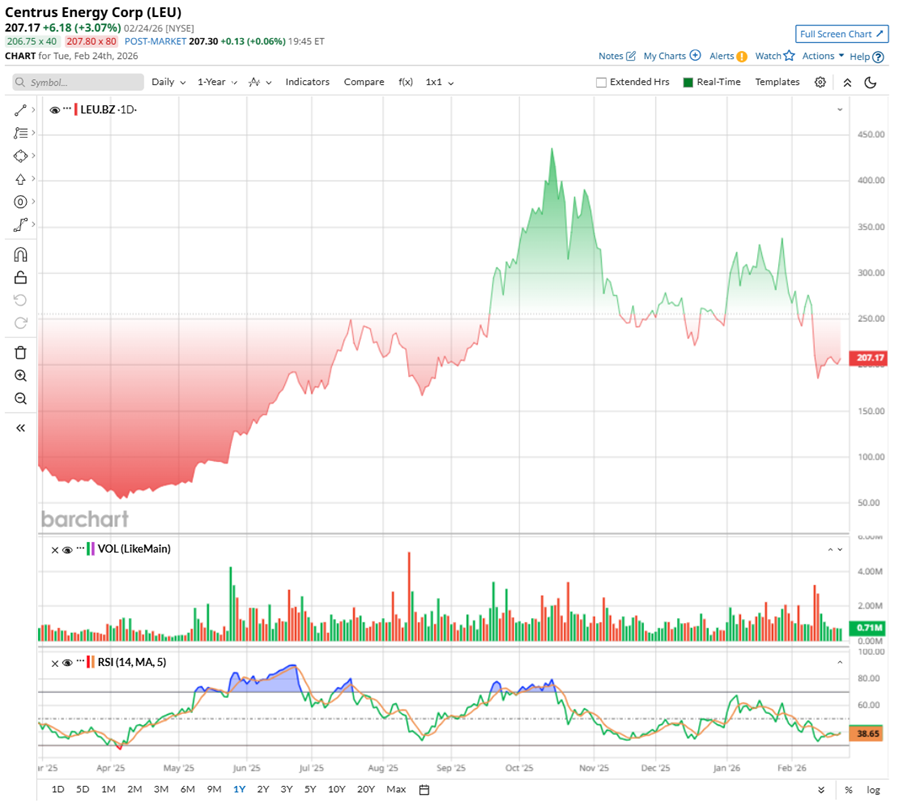

Centrus Energy’s shares have delivered a dramatic price journey over the past year—one marked by sharp rallies and equally sharp pullbacks. The stock soared to a record $464.25 in October, riding strong uranium sentiment and supply-driven enthusiasm. Since then, shares have retraced significantly, now trading more than 55.4% below that peak as momentum cooled and valuations reset.

Even with that correction, the broader performance remains striking. Over the past 52 weeks, LEU is still up 131.3%, outperforming much of the uranium space. For context, the Global X Uranium ETF (URA) has climbed 114% in the past year. Momentum improved late last year following its NYSE uplisting news, which helped steady the decline.

However, 2026 has opened on a softer note. The stock is down about 17% over the past three months and nearly 15% on a year-to-date (YTD) basis. It touched a low of $183.45 in mid-February. Technically, with the 14-day RSI hovering near 40, selling pressure appears to be easing, though confidence remains measured.

Even after the pullback, LEU is not exactly a bargain. Investors are still pricing in strong execution and future growth. The stock trades around 57x forward adjusted earnings and 8.5x forward sales, trading above sector averages and its own historical medians.

A Snapshot of Centrus’ Q4 Earnings Report

When Centrus Energy released its fourth-quarter and full-year 2025 results on Feb. 10, shares slid more than 20% the following trading session after both Q4 revenue and earnings fell short of Wall Street’s expectations. Quarterly revenue dipped 3.6% year-over-year (YoY) to $146.2 million, while EPS dropped sharply to $0.79 from $3.20 a year earlier—a reset that clearly unsettled investors.

Digging into the business lines, the story was more layered. Revenue from separative work units (SWU) in Q4 surged 127.9% YoY to $111 million, technical solutions revenue declined 26.6% to $21.8 million, and uranium sales fell steeply to $13.4 million, reflecting timing and contract dynamics rather than structural weakness.

For the full fiscal year, revenue inched up 1.5% annually to $448.7 million, while gross profit improved to $117.5 million. Net income reached $77.8 million, or $3.90 per share. LEU segment revenue came in at $346.2 million, slipping 1% from last year. Uranium sales declined, but higher volumes of SWU lifted its revenue, even though the average selling price dipped slightly.

Centrus closed the year on far stronger financial footing. Cash and cash equivalents rose sharply to $1.96 billion, compared with $671.4 million at the end of 2024. Its unrestricted cash position expanded to roughly $2 billion, underscoring improved liquidity and balance sheet flexibility. Meanwhile, operating cash flow gained momentum. Cash generated from operations climbed to $51 million, a clear sign of strengthening internal cash generation.

A key highlight for Centrus Energy is the depth and duration of its contracted visibility. Total backlog climbed to $3.8 billion through 2040, including $2.9 billion tied to the LEU segment, with $2.3 billion in contingent sales supporting potential expansion of production capacity at the Piketon, Ohio.

Strategically, 2025 marked an inflection point. Centrus advanced both its existing enrichment operations and its future growth platform, formally launching its centrifuge buildout in the fourth quarter. The company also secured a $900 million HALEU enrichment award from the U.S. government, strengthening its role in domestic fuel supply. With a growing LEU order book and targeted HALEU output of 12 metric tons, Centrus is positioning itself to address commercial reactor demand, national security requirements, and the emerging advanced reactor market.

Looking ahead, management is guiding for fiscal 2026 revenue in the range of $425 million to $475 million, with capital deployment projected between $350 million and $500 million. Much of this investment will fund its accelerating centrifuge manufacturing buildout. Operationally, management aims to finalize key industrial partnerships, hire at least 100 employees in Oak Ridge and 50 in Piketon, and advance toward releasing a Certified for Construction package—steady steps toward scaling domestic enrichment capacity.

Analysts tracking the company expect earnings to soften in the near term, with fiscal 2026 EPS projected to dip 27.2% annually to $3.27. However, profitability is forecast to stabilize thereafter, with fiscal 2027 EPS edging up 3.4% annually to $3.38.

What Do Analysts Expect for LEU Stock?

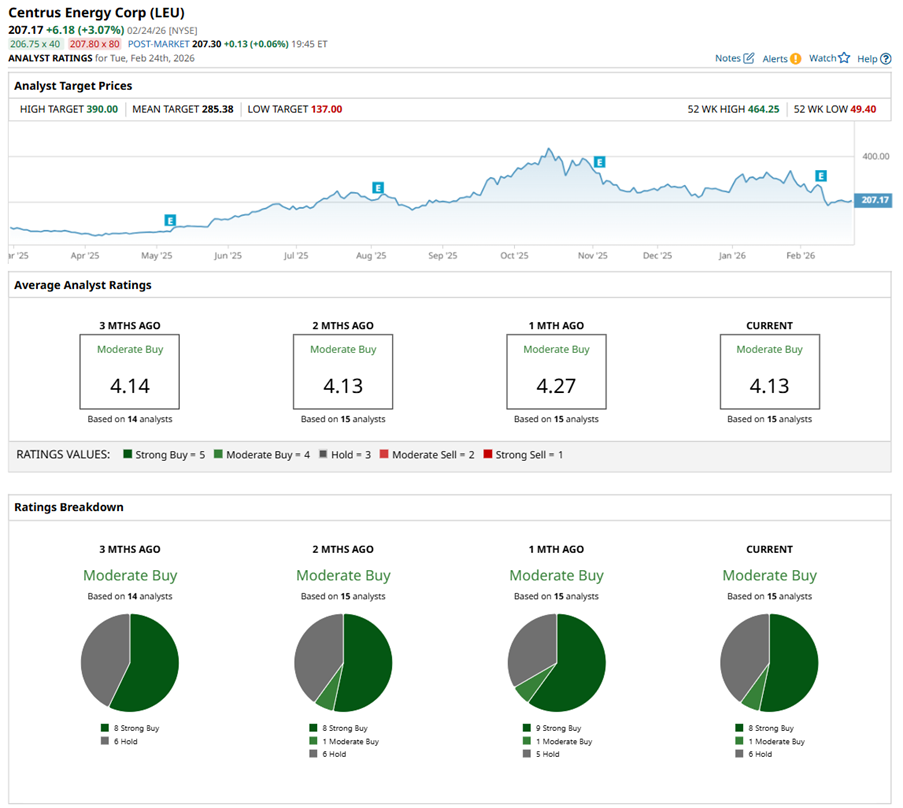

Sentiment around Centrus Energy stays positive, as analysts remain confident long-term while staying mindful of short-term swings. LEU stock has a “Moderate Buy” consensus rating overall. Of the 15 analysts tracking the stock, eight have a “Strong Buy,” one has a “Moderate Buy,” and the remaining six have a “Hold” rating.

While LEU has pulled back over the past months, Wall Street continues to model meaningful upside. The average price target of $285.38 implies roughly a 37.8% potential surge from current levels. On the more optimistic end, the Street-high target of $390 suggests the possibility of an 88% advance, should operational momentum and favorable uranium market dynamics persist.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- 1 Stock to Buy Now as Experts Warn of a Looming Uranium Supply Crunch

- As Oil Surges on Iran Tensions, Is It Better To Buy the Commodity or Energy Stocks?

- 2 Top Stocks That Analysts Love to Play the AI Data Center Boom

- Everything You Need to Know About Musk’s ‘Self-Growing’ Moon City as He Races to ‘Secure the Future of Civilization’