The chemicals sector has been under pressure lately. Global demand is weak, and feedstock and energy costs remain high, squeezing margins for petrochemical makers. Amid this pressure, LyondellBasell (LYB), a heavyweight in chemicals, just announced a surprise dividend cut. The board declared a quarterly payout of $0.69, down from $1.37 in Q4 2025, about a 50% reduction. That move reflects one of the longest downturns in the industry.

For income investors, halving the payout is jarring. Let's dig into what led to this change and why it may be more prudent than it appears at first glance.

About LyondellBasell Stock

LyondellBasell is a top global chemical and plastics producer. By revenue, it is one of the world’s largest polymer makers, focusing on polyethylene, polypropylene, and refining. It is unique in having an integrated model from refining oil to making polyolefins, plus advanced materials and catalysts. With over 25 plants worldwide, its scale and technology leadership (especially in polyolefins) set it apart.

LYB has quietly advanced some strategic plans. It’s on track to sell four European units by Q2 2026 to simplify its portfolio and raise cash. Work on its MoReTec-1 plastic-to-fuel recycling plant in Germany is also proceeding, with a 2027 startup targeted. These moves, alongside continued workforce cuts of 7% in 2025, reinforce that management is retrenching to the core business and shoring up finances. LyondellBasell has stayed mostly quiet on big acquisitions or new ventures lately; instead, the focus is on cost savings and maintaining its investment-grade balance sheet.

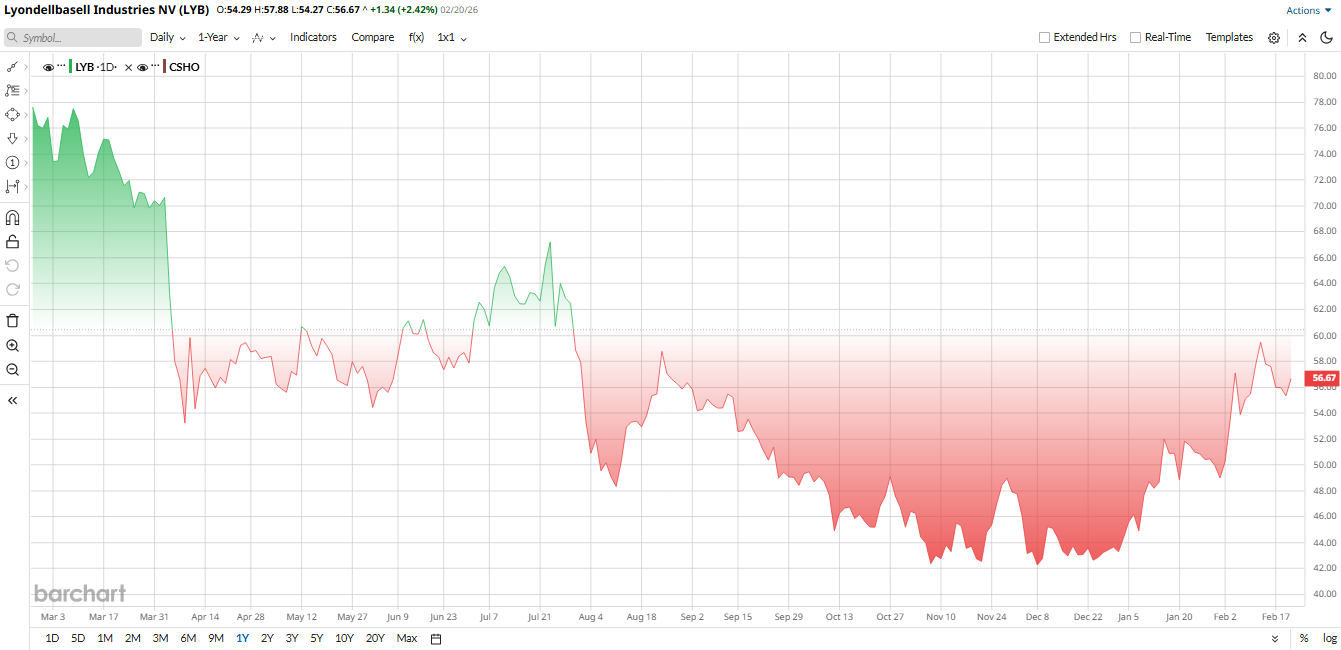

LYB’s share price took a beating in 2025. Over the 12 months, the stock fell sharply by roughly 27% as chemical margins crumbled. Furthermore, the slide accelerated on disappointing earnings and industry oversupply. However, more recently, the stock has rebounded strongly. As of late February 2026, LYB was up about 30% year-to-date (YTD). That rally reflected cost-cutting news and hopes that the trough was near. Still, LYB is off its highs; most of 2025 was weak as markets stayed sluggish.

LYB presents an attractive valuation scenario. Its EV/Sales is 0.8, significantly lower than the sector median of 2.1. Additionally, the dividend yield stands at a remarkable 9.46%, far surpassing the sector's yield of 1.6%, suggesting good income potential. Overall, LYB looks cheap to fair on some metrics, and it has an investment-grade balance sheet, which suggests the stock isn’t grossly overvalued.

Dividend Cut News

On Feb. 20, LYB’s board slashed the quarterly dividend to $0.69 per share. That’s about a 50% cut; the previous dividend was $1.37. Management framed the move as a “recalibration” needed in a prolonged industry trough. CEO Peter Vanacker noted that despite the downcycle, LB still returned $2 billion in cash to shareholders in 2025 but expects markets to remain challenged. By cutting the payout, LYB preserves cash to bolster its balance sheet and invest in cost-saving initiatives. It insisted this step is temporary: the company remains “committed to our target of returning 70% of free cash flow to shareholders through the cycle.”

In practical terms, the move frees up roughly $1.4 per share per year in cash from the lost dividend, which can fund operations or debt reduction instead. For income investors, it’s unwelcome news that the yield falls dramatically, but for longer-term holders, it signals prudence. But importantly, LYB says this won’t preclude future dividends once conditions improve.

LYB Earnings Miss Q4 Earnings Expectations

LYB reported disappointing Q4 2025 earnings released Jan 30, 2026, that align with the dividend decision. Sales were $7.091 billion, down 9% from $7.808 billion in Q4 2024. This actually came in slightly above consensus at around $6.9 billion, but the decline mainly reflects lower product prices and volumes in a weak market. Operationally, EBITDA was just $417 million, trimmed by seasonality and high feedstock costs.

The EPS story was even harsher. LYB swung to an adjusted loss of $0.26 per share in Q4, versus analyst expectations of a small profit. In fact, this was a reversal from last year’s $0.75 profit in Q4 2024. Management blamed typical year-end headwinds and higher raw material costs. Chief Financial Officer Agustin Izquierdo highlighted that cost cuts and working capital savings helped soften the year. The company freed up over $1 billion of working capital in Q4, ending 2025 with $3.4 billion of cash and about $8.1 billion total liquidity. In fact, LYB achieved $2.3 billion of operating cash flow for 2025, meeting its cash-improvement plan ahead of schedule. It even raised its target: LYB now plans to generate an extra $500 million of free cash in 2026, for a cumulative $1.3 billion of savings through next year.

Looking ahead, guidance was cautious. No specific revenue or profit forecasts were given, but the company expects continued volatility in feedstock and energy costs. Management said it will align operating rates to market demand in early 2026, with a modest restart of polymer capacity as inventories tighten. They projected 2026 capital spending at around $1.2 billion, with $400 million for growth projects, $800 million for sustaining, and a much lower effective tax rate of 10%.

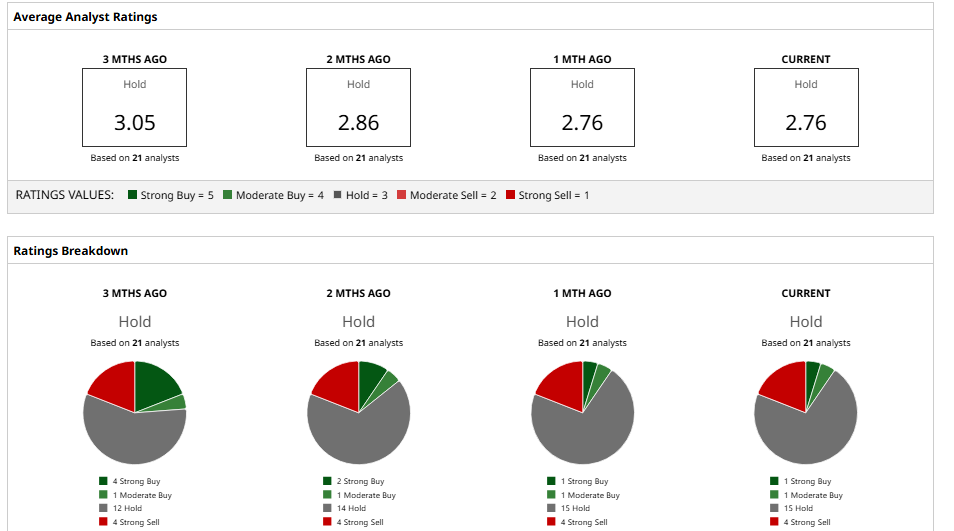

What Analysts Are Saying About LYB Stock

Wall Street is generally mixed on LYB stock's prospects. Recently, Goldman Sachs reiterated its “Sell” rating with a $51 price target, citing uncertainty around the dividend policy. GS noted investors may be skeptical of the timing of the cut and warned the dividend sustainability remains in question.

By contrast, Mizuho recently raised its target to $53, arguing that LB’s Q4 revenue beat and strong cost cuts could cushion the downturn. KeyBanc kept its Sector Weight "Hold" stance, pointing out ongoing weakness in olefins/polyolefins and high MTBE costs, though it did note the hefty dividend yield, now 11%, as an unusually high return for shareholders.

In general, analysts have a consensus “Hold” rating with a mean price target of $50.47, which suggests modest downside from current levels. However, analysts agree that 2025 was a trough; many have modestly raised 2026 earnings forecasts now that costs are being clipped.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- This Blue-Chip Stock Just Slashed Its Dividend by 50%. Should You Run Away Now?

- Claude Just Dealt Another Blow to IBM Stock. Will It Be Fatal, or Should You Buy the Dip?

- 3% Yield and 93% Upside: This Dividend Stock Could Offer a Lifetime of Income

- As Walmart Raises Its Dividend 5%, Should You Buy WMT Stock?