When one hears that some of the leading lights of the investing world — like Warren Buffett, Ray Dalio, and Ken Griffin — have sold off shares of a company, it certainly leaves an impact. That's the case even if it's Apple (AAPL). Based on recent filings, Buffett's Berkshire Hathaway (BRK.A), Dalio's Bridgewater Associates, and Griffin's Citadel Advisor recently reduced their stakes in the consumer tech giant by 4.3%, 16%, and 6%, now holding 227 million shares, 289,000 shares, and 31.7 million shares, respectively.

However, while these legendary investors may have lessened their stakes, some of Wall Street's leading institutions have actually added Apple shares as well. The world's largest asset manager, BlackRock (BLK), purchased 8.3 million shares, bringing its AAPL stake to more than 1.15 billion shares. Likewise, investment banking majors Morgan Stanley (MS) and Goldman Sachs (GS) now hold more than 230 million shares and 99 million shares of AAPL stock after recent purchases.

Now the question is: How do these moves affect Apple as a potential investment? While these high-profile sales and purchases make for good headlines, investors still need consider how AAPL stock stacks up as an investment for the long term. Let's take a closer look.

A Fortress Balance Sheet with Solid Numbers

Apple's ubiquity in the consumer tech landscape, despite its premium pricing, has led to the company sporting 10-year compound annual growth rates (CAGRs) of 5.9% and 12.4% for revenue and earnings, respectively. That's a testament to both Apple's brand power and the quality of its products and services.

Notably, the company's earnings have exceeded Wall Street expectations consistently. Moreover, revenue of $143.8 billion in the most recent quarter was not only higher by 16% year-over-year (YOY) but also handily surpassed the consensus estimate. This was fueled by staggering demand for the iPhone 17 lineup, which propelled iPhone net sales to $85.3 billion, up 23% YOY. Apple's high-margin services segment also saw net sales of $30 billion in the first quarter of 2026, up from $26.3 billion in the year-ago period.

Gross margins expanded to 48.2% as well, signifying strong pricing power. Meanwhile, EPS increased by 18% YOY to $2.84, while also coming in higher than Street forecasts for $2.65 per share. Apple also repurchased shares worth $25.2 billion in the quarter, which further aided EPS growth.

Cash flow from operating activities for the quarter came in at $53.9 billion, up a whopping 80% from the prior year. The company exited the quarter with a cash balance of $45.3 billion, much ahead of its short-term debt levels of $13.8 billion.

Valuation-wise, AAPL stock trades at heightened levels, but it is not out of whack. Apple's forward price-to-earnings (P/E), price-to-sales (P/S), and price-to-cash flow (P/CF) ratios of 31.6 times, 9.3 times, and 31.7 times, respectively, are all above the sector medians. However, compared to its five-year average, the stock is trading at a reasonable premium for a tech giant such as Apple, especially considering that the powerful iPhone segment is again firing on all cylinders and seeing increasing traction in fast-growing markets like India.

Overall, with a market capitalization of $3.9 trillion, AAPL stock is up just 1% on a year-to-date (YTD) basis.

Apple of the Eye

Things are gradually turning around for Apple. After a strong Q1 2026 courtesy of growth acceleration with solid iPhone sales, Apple's guidance looks robust, highlighted by higher R&D spending and increased AI efforts.

Notably, Apple has transitioned from a defensive to an offensive posture regarding AI, primarily through its Apple Intelligence suite. According to the Q1 2026 earnings call, CEO Tim Cook noted that the majority of users on enabled devices are now actively leveraging these features, which have expanded to 15 languages.

Strategically, Apple is prioritizing “personal” intelligence — on-device processing that ensures privacy, a key differentiator from cloud-centric competitors. This is powered by the A18 Pro and the newly unveiled M5 chip. The M5, built on an advanced 3-nanometer (nm) node, introduces a rearchitected GPU with dedicated Neural Accelerators, delivering a significant compute increase for AI tasks over the M4. Users are finding utility in integrated "Writing Tools," "Clean Up" in Photos, and the deeper integration of LLMs for "World Knowledge" queries. By embedding these models directly, Apple has effectively turned AI into a feature of the ecosystem rather than a standalone product, driving a massive "upgrade cycle" as older hardware cannot support these high-memory on-device requirements.

For its growth plans in terms of geography, Apple is doubling down on India, which is now the world’s second-largest smartphone market. Apple plans to open several more retail stores there throughout 2026.

On the other hand, while the iPhone 17 series drove record quarterly revenue, the focus is shifting to the iPhone 18, which is expected in late 2026. To maintain the current momentum, Apple is reportedly moving toward 2nm silicon (the A20 chip), which promises the most significant efficiency gain in years. However, supply chain constraints in advanced node production remain a variable. To diversify beyond the iPhone, Apple is aggressively growing its iPad and Wearables divisions. Furthermore, the company is quietly seeding new categories, with research and development shifting toward AI-enabled wearables — such as smart glasses and AirPods with "Visual Intelligence" cameras — to eventually supplement the iPhone as the primary interface for "ambient" computing.

However, challenges remain, with the industry seeing a sharp rise in memory component pricing. While Apple’s scale gives it better procurement leverage than peers, the increased Bill of Materials (BoM) cost is a headwind for fiscal 2026, which may limit the company's ability to maintain its aggressive earnings growth if production costs spike. Tariff issues and antitrust suits also remain irritants.

What Do Analysts Think About AAPL Stock?

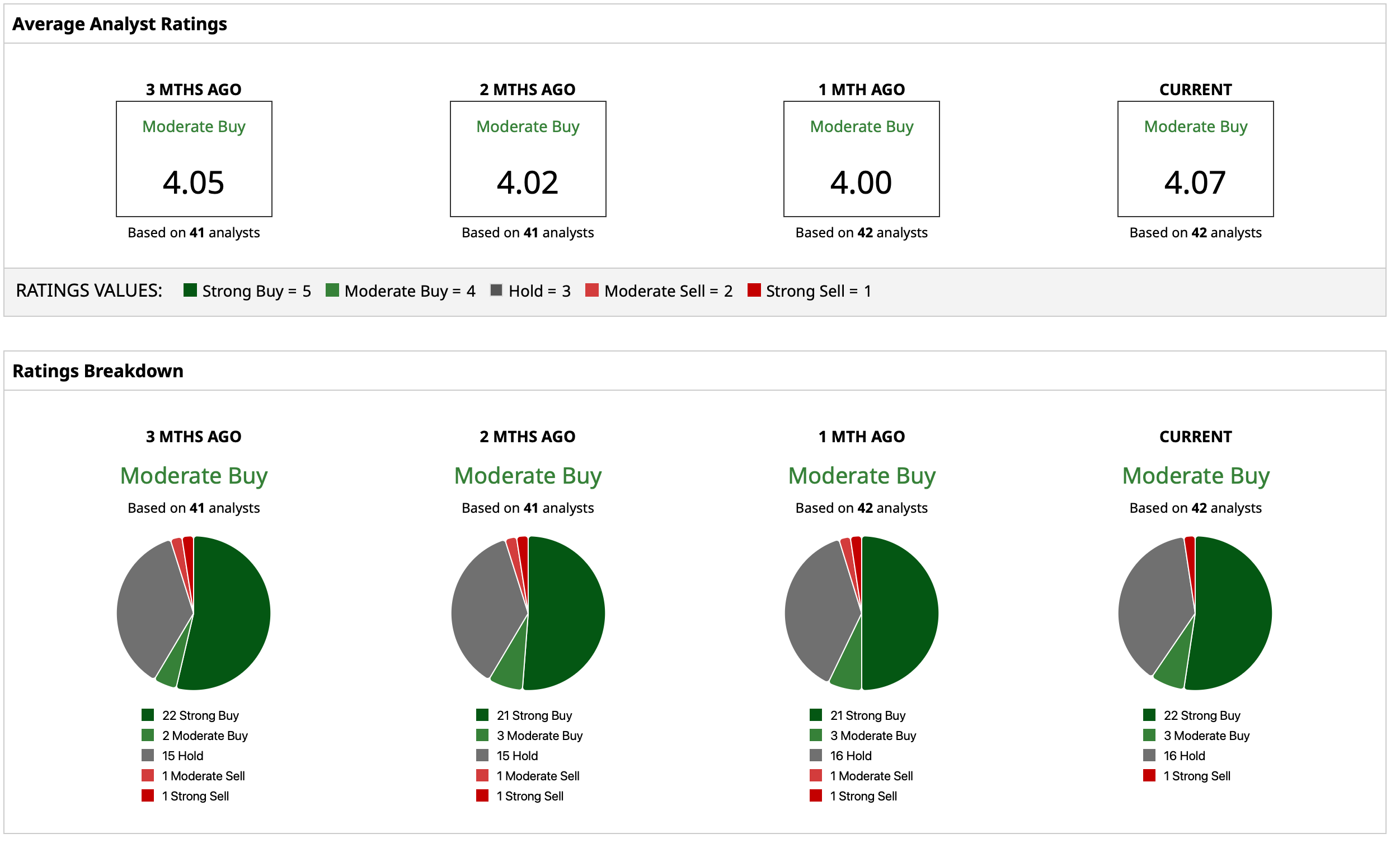

Analysts deem AAPL stock to be a consensus “Moderate Buy,” with the mean target price of $293.48 pointing to potential upside of about 7% from current levels. Out of 42 analysts covering the stock, 22 have a “Strong Buy” rating, three have a “Moderate Buy” rating, 16 have a “Hold” rating, and one has a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Cava Stock Jumps Into Overbought Territory. Is It Too Late to Buy CAVA Now?

- Axon Stock Is Challenging Its 50-Day Moving Average. Should You Buy AXON on the Post-Earnings Rally?

- Ken Griffin, Ray Dalio, and Warren Buffett All Sold More Apple Stock. Should You?

- As Circle Stock Breaks Through Key Resistance Levels, Should You Chase the CRCL Rally?