Stamford, Connecticut-based Philip Morris International Inc. (PM) is a tobacco company with a market cap of $291.1 billion. It offers cigarettes and smoke-free products, including heat-not-burn, e-vapor, and oral nicotine products.

Companies valued at $200 billion or more are typically classified as “mega-cap stocks,” and PM fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the tobacco industry. The company is known for its strategic leadership in smoke-free products. Its key strengths include significant pricing power, robust cash flow generation, extensive global distribution, and deep regulatory expertise.

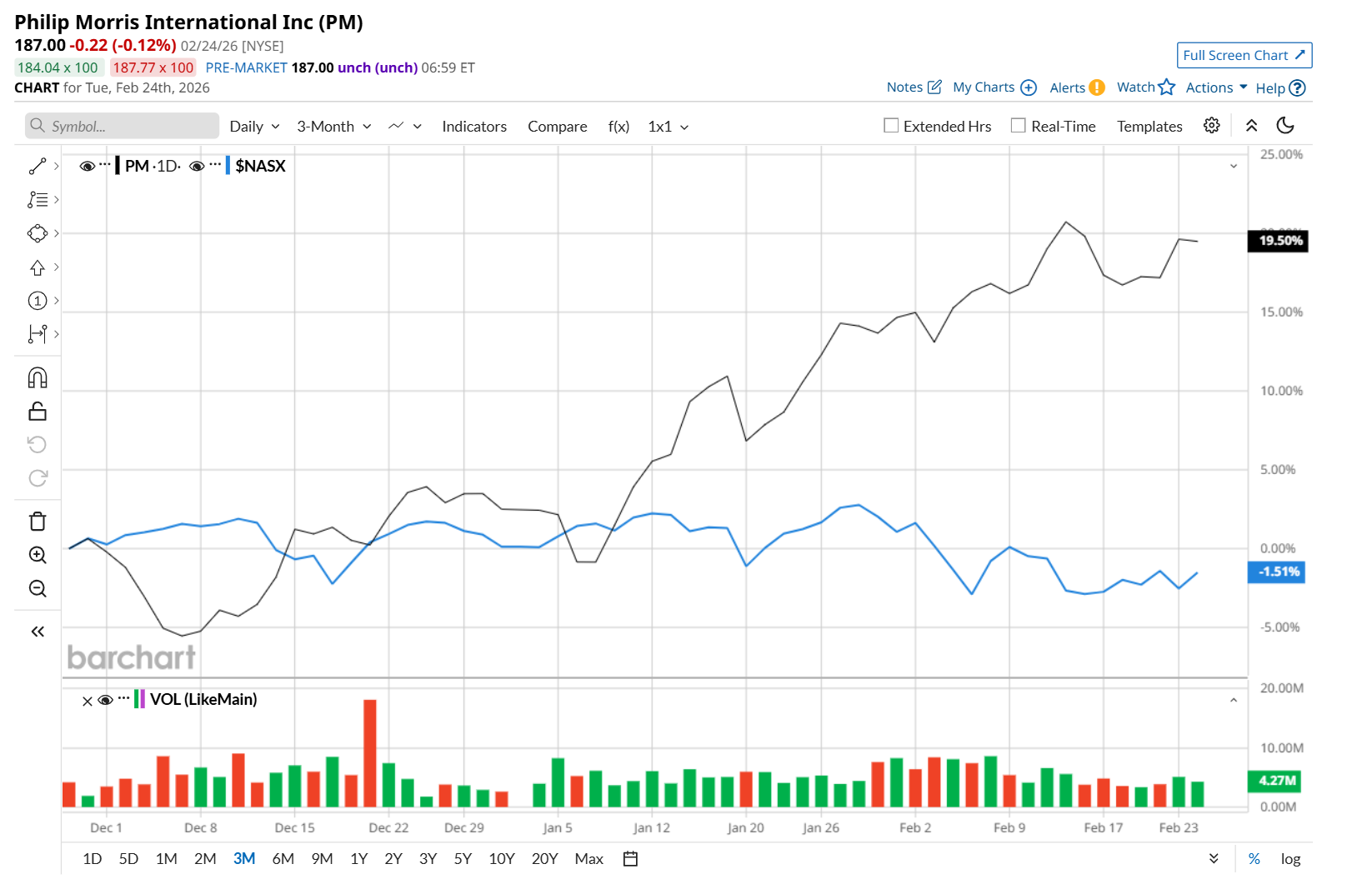

This tobacco giant is currently trading 2.1% below its 52-week high of $190.98, reached on Feb. 12. Shares of PM have soared 23.8% over the past three months, considerably outpacing the Nasdaq Composite’s ($NASX) marginal drop during the same time frame.

Moreover, on a YTD basis, shares of PM are up 16.6%, compared to NASX’s 1.6% drop. In the longer term, PM has soared 19.7% over the past 52 weeks, outperforming NASX’s 18.6% gain over the same period.

To confirm its bullish trend, PM has been trading above its 200-day moving average since mid-January, and has remained above its 50-day moving average since mid-December.

On Feb. 6, shares of PM closed up marginally after its Q4 earnings release. The company’s net revenue increased 6.8% year-over-year to $10.4 billion, driven by robust growth in both combustibles and smoke-free businesses. Moreover, its adjusted EPS of $1.70 advanced 9.7% from the same period last year, topping analyst expectations of $1.67.

PM has notably lagged behind its rival, British American Tobacco p.l.c. (BTI), which rallied 61% over the past 52 weeks. However, it has outpaced BTI’s 9.6% YTD rise.

Looking at PM’s recent outperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 14 analysts covering it, and the mean price target of $195.96 suggests a 4.8% premium to its current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Cathie Wood Is Buying Up AMD Stock. Should You?

- This Earnings Season, Remember Warren Buffett’s Message That ‘Beating Expectations’ Is ‘Disgusting’ and ‘One of the Shames of Capitalism’

- GE Aerospace Is Linking Up with Palantir. Should You Buy GE Stock Here?

- Okta Stock Is Down 20% in 2026. Can It Survive the Software Apocalypse?