Shares of Dell Technologies (DELL) have pulled back sharply in recent months, falling more than 29% from their 52-week high even as demand for its artificial intelligence (AI)-optimized servers continues to surge. With the company set to report fourth-quarter results on Feb. 26, does the recent decline represent an opportunity to buy ahead of the earnings print, or is it a warning sign?

Dell has benefited from robust demand for AI servers as enterprises and hyperscalers accelerate spending on data center upgrades to support generative AI workloads. This structural tailwind has translated into strong order activity, supporting Dell’s growth.

Despite the revenue momentum, its margins have come under pressure. Over the first nine months of fiscal 2026, Dell’s adjusted gross margin contracted by 190 basis points to 20.4%, while adjusted operating margin fell by 10 basis points. Adding to the pressure are the competitive headwinds and rising prices of memory components.

Looking ahead to Q4, Dell expects solid year-over-year (YoY) growth in both revenue and earnings. A strong print could help restore confidence, especially if it shows stabilization in margins or improved operating leverage. Still, expectations for volatility are elevated. Options markets are pricing in a post-earnings move of about 10% in either direction for contracts expiring Feb. 27, a swing notably larger than the stock’s average 5.9% move following earnings over the past four quarters.

Investors should also note that DELL shares have declined after earnings in three of the last four quarters, indicating that even solid financial performance and upbeat guidance do not guarantee a positive short-term market reaction.

Dell Q4 Earnings: Here’s What to Expect

The solid momentum in Dell’s top line will likely sustain in Q4 despite competitive headwinds. Dell’s Infrastructure Solutions Group (ISG) is expected to ship approximately $9.4 billion worth of AI servers in Q4. That would bring full-year AI server shipments to roughly $25 billion, representing growth of more than 150% compared with the prior year. Demand trends appear solid. Over the past three quarters, the company has accumulated around $30 billion in AI server orders, signaling sustained enterprise and hyperscaler appetite for accelerated computing capacity.

Dell’s traditional data center portfolio is holding up well. Enterprises continue to modernize and consolidate infrastructure, supporting demand for both servers and storage systems. Within storage, Dell’s IP-based portfolio could continue to expand at a healthy pace.

Dell’s Client Solutions Group (CSG) is positioned to benefit from the ongoing PC refresh cycle. Further, solid execution will help drive market share gains.

Dell has guided for fourth-quarter revenue between $31 billion and $32 billion. At the midpoint of $31.5 billion, that would represent 32% YoY growth. Combined revenue from ISG and CSG is projected to increase 34% at the midpoint, with ISG expected to post mid-60% growth and CSG rising in the low- to mid-single-digit range.

Dell’s strong revenue growth, an improved product mix, sequential improvement in ISG operating margins, and continued storage momentum will likely lift Dell’s earnings. Management projects adjusted earnings per share (EPS) at $3.50, up 31% from a year ago.

Wall Street, however, is modeling a slightly more conservative $3.32 per share. Dell has topped consensus earnings estimates in three of the past four quarters.

Is DELL Stock a Buy, Sell, or Hold?

Dell is set to deliver strong double-digit revenue and earnings growth in Q4. Further, as the AI order book swells, the company is likely to sustain momentum in 2026.

Despite these favorable fundamentals, the stock’s performance over the past year has been relatively subdued. The muted market reaction suggests that investor sentiment toward the broader sector remains cautious, even as AI-driven spending accelerates. At the same time, margin pressure, memory cost challenges, and competitive headwinds temper the bullish case.

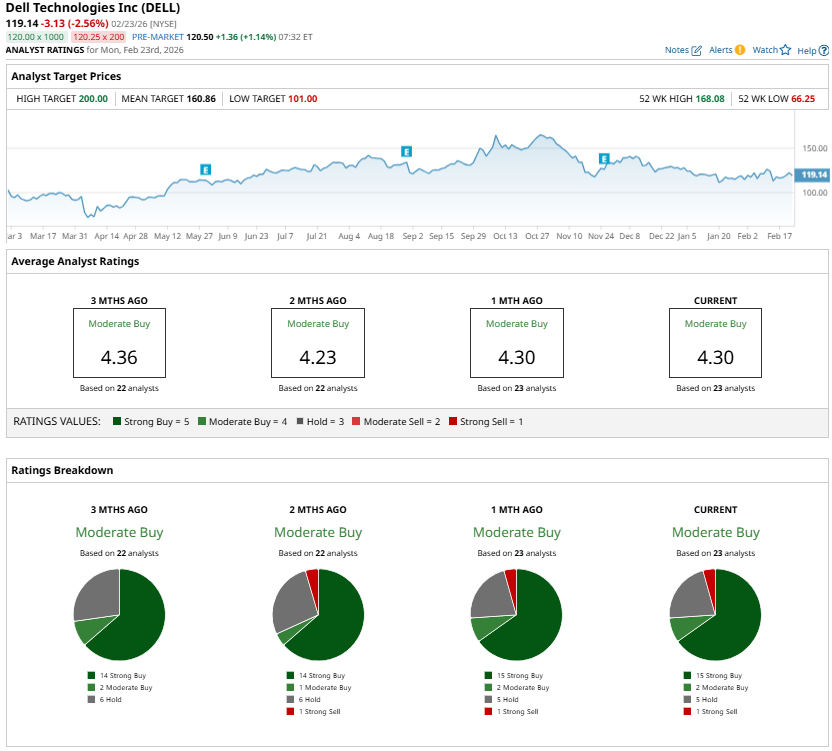

Heading into the fourth-quarter earnings report, analysts maintain a “Moderate Buy” consensus rating on DELL stock.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart