2026 is shaping up to be quite a challenging year for several information technology, cybersecurity, and software giants, particularly as artificial intelligence (AI) continues to disrupt the status quo. The latest shake-up comes from AI startup Anthropic, which has begun rolling out innovations that threaten to unsettle the dominance of these legacy players. And International Business Machines Corporation (IBM) appears to be one of the latest casualties.

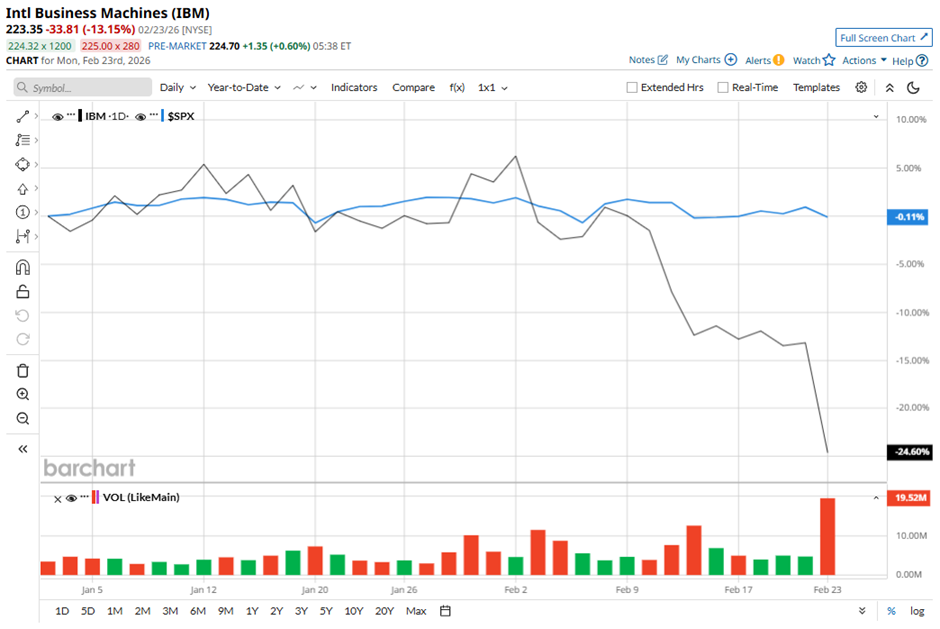

On Feb. 23, IBM shares recorded their steepest single-day drop in more than 25 years, plunging over 13% after Anthropic announced that its Claude Code tool could be used to modernize COBOL. The aging programming language, developed in the late 1950s, predominantly runs on IBM systems and is still widely used in business data processing, such as payment processing and retail transaction systems.

Traditionally, modernizing COBOL systems has been a slow, expensive, and consultant-heavy process, often taking years to complete. But Anthropic claims Claude Code can automate much of the exploration and analysis work that consumes the bulk of these projects. “With AI, teams can modernize their COBOL codebase in quarters instead of years,” the company said in a blog post. That statement was enough to rattle investors.

With IBM producing the majority of mainframes that run COBOL workloads, the prospect of AI dramatically reducing the complexity, and potentially the dependence on traditional modernization pathways, triggered intense selling pressure. Given this new development, is IBM stock a buy-the-dip opportunity or a red flag investors shouldn’t ignore?

About IBM Stock

New York-based IBM is a global technology company focused on hybrid cloud, AI, and enterprise consulting. Serving clients across more than 175 countries, IBM helps organizations harness data insights, modernize operations, improve efficiency, and manage costs in increasingly complex digital environments. Its customer base includes governments and major enterprises in critical infrastructure sectors such as financial services, telecommunications, and healthcare.

Many of these organizations rely on IBM’s hybrid cloud platform and Red Hat OpenShift to execute large-scale digital transformation projects. At the same time, IBM continues to expand its footprint in areas such as AI, quantum computing, and industry-focused cloud solutions, supported by a consulting division that assists businesses in integrating new technologies with legacy systems.

With a market capitalization of around $208.8 billion, this software giant is going through a rough patch on Wall Street as broader industry headwinds pick up. Software stocks globally have been under pressure in recent months, as investors grow increasingly wary of the fast-evolving capabilities of AI tools, especially after Anthropic rolled out new plug-ins tied to its Claude large language model in early February, a move seen as the startup’s effort to expand into the application layer.

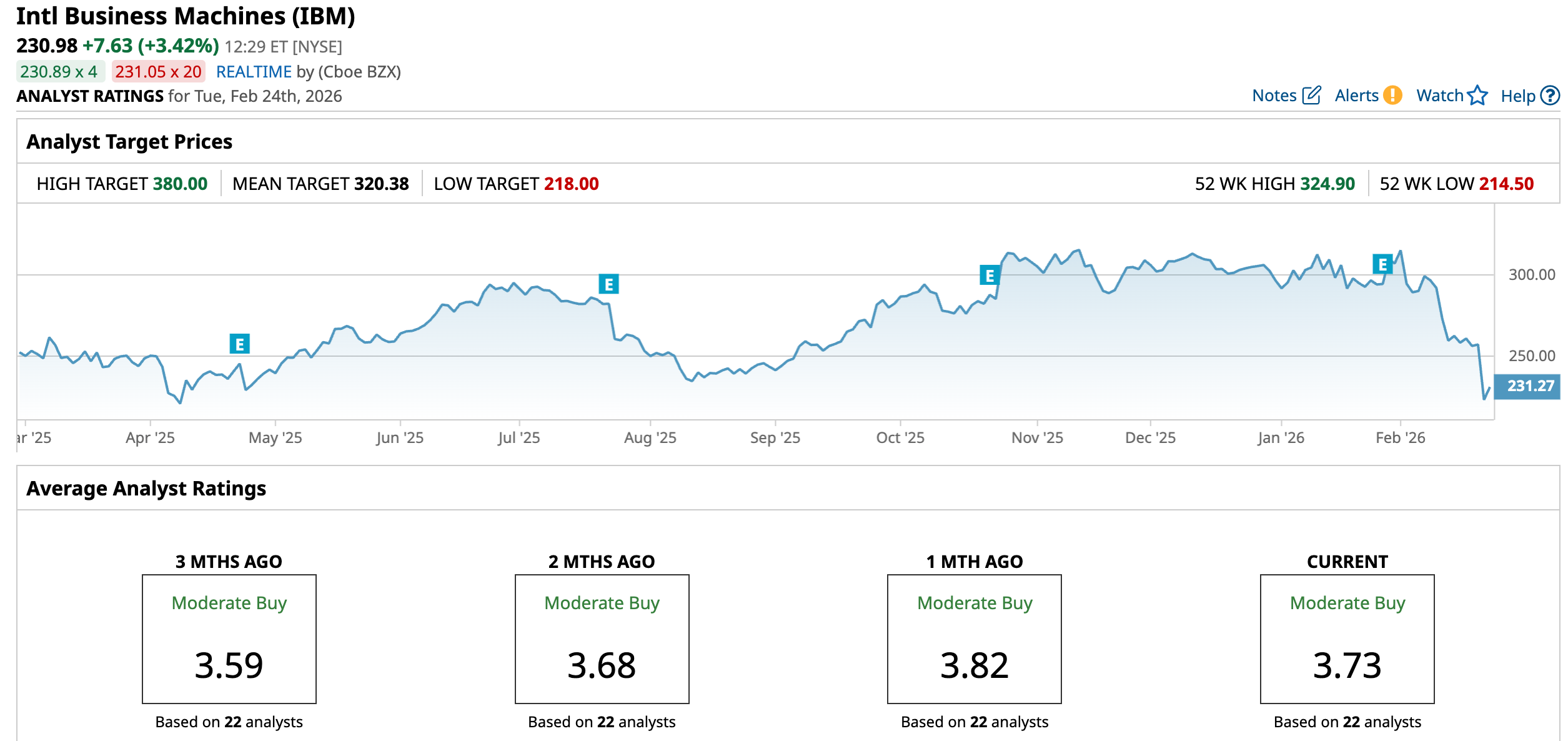

IBM’s sharp 13.2% selloff on Feb. 23 only added to the strain, leaving the stock down nearly 21.9% so far in 2026. That’s a much steeper drop compared to the broader S&P 500 Index ($SPX), which is only marginally higher year-to-date (YTD). In fact, after surging to a 52-week high of $324.90 in November, the stock has since given up significant ground, sliding nearly 40.7% from its peak, a steep pullback that highlights the dramatic change in investor mood.

IBM also stands out as one of the few legacy tech players that continues to reward shareholders with a meaningful dividend. The company has increased its payout for 30 consecutive years, earning its place as a Dividend Aristocrat. Most recently, IBM declared a quarterly dividend of $1.68 per share, payable on Mar. 10.

With that payment, the company will have delivered uninterrupted quarterly dividends every year since 1916, a track record that spans more than a century. On a forward annualized basis, IBM pays $6.72 per share, translating to an attractive yield of about 2.61%, offering investors a steady income stream even as the stock navigates near-term market volatility.

Inside IBM’s Q4 Earnings Results

While IBM continues to face investor anxiety around AI-driven disruption, its underlying financial performance tells a more reassuring story. On Jan. 28, the company delivered its fiscal 2025 fourth-quarter earnings report, and it comfortably surpassed Wall Street’s expectations on both revenue and earnings. Notably, AI is emerging as a key growth engine. IBM revealed that its generative AI book of business has now surpassed $12.5 billion.

Customers are leveraging IBM’s mainframes to run AI inference workloads, deploying its watsonx platform for AI governance, and using Red Hat OpenShift to manage AI applications across multicloud environments. Consulting is also proving to be a key catalyst, with the impact evidenced by the numbers. Fourth-quarter revenue rose 12% year-over-year (YOY) to $19.7 billion, beating Wall Street’s estimate of $19.2 billion.

Infrastructure led the surge, with revenue jumping 21% to $5.1 billion. Software revenue climbed 14% to $9 billion, while consulting revenue edged up 3% to $5.3 billion. On the earnings front, adjusted EPS came in at $4.52, up 15.3% YOY and comfortably ahead of the $4.29 consensus estimate. IBM closed the quarter with $14.5 billion in cash, restricted cash, and marketable securities, slightly lower than at year-end 2024.

Total debt rose to $61.3 billion, including $15.1 billion related to IBM Financing, reflecting a $6.3 billion increase since year-end 2024. Encouragingly, the company generated $7.6 billion in free cash flow, up a solid $1.4 billion YOY, underscoring its ability to convert growth into real cash. And IBM didn’t hesitate to share that strength with investors, returning a substantial $1.6 billion to shareholders through dividends in the fourth quarter alone.

Looking ahead to full-year 2026, IBM expects constant-currency revenue growth of more than 5%, with foreign exchange projected to provide roughly a half-point tailwind at current rates. Further, the company anticipates free cash flow will increase by about $1 billion YOY, a sign that, despite near-term volatility, management remains confident in its growth trajectory.

How Are Analysts Viewing IBM Stock?

While investors are rattled after Claude’s new innovation, Evercore ISI kept its “Outperform” rating on IBM and maintained a $345 price target, even after the stock dropped following Claude’s blog post about AI-powered COBOL modernization. Evercore pushed back on investors' fears. The firm noted that IBM already offers its own modernization tools, including watsonx Code Assistant for Z. More importantly, IBM’s latest z17 mainframe cycle is actually performing better than the prior z16 cycle in its first three quarters, a sign that customer demand remains solid.

Evercore also pointed out that clients have always had the option to move away from mainframes. Yet many continue to stay because of key advantages such as reliability, speed, ability to handle massive transaction volumes, cost efficiency at scale, built-in AI inferencing capabilities, strong security, and strict regulatory compliance. In short, while AI tools may create new options, IBM’s mainframe still plays a critical role for many large enterprises.

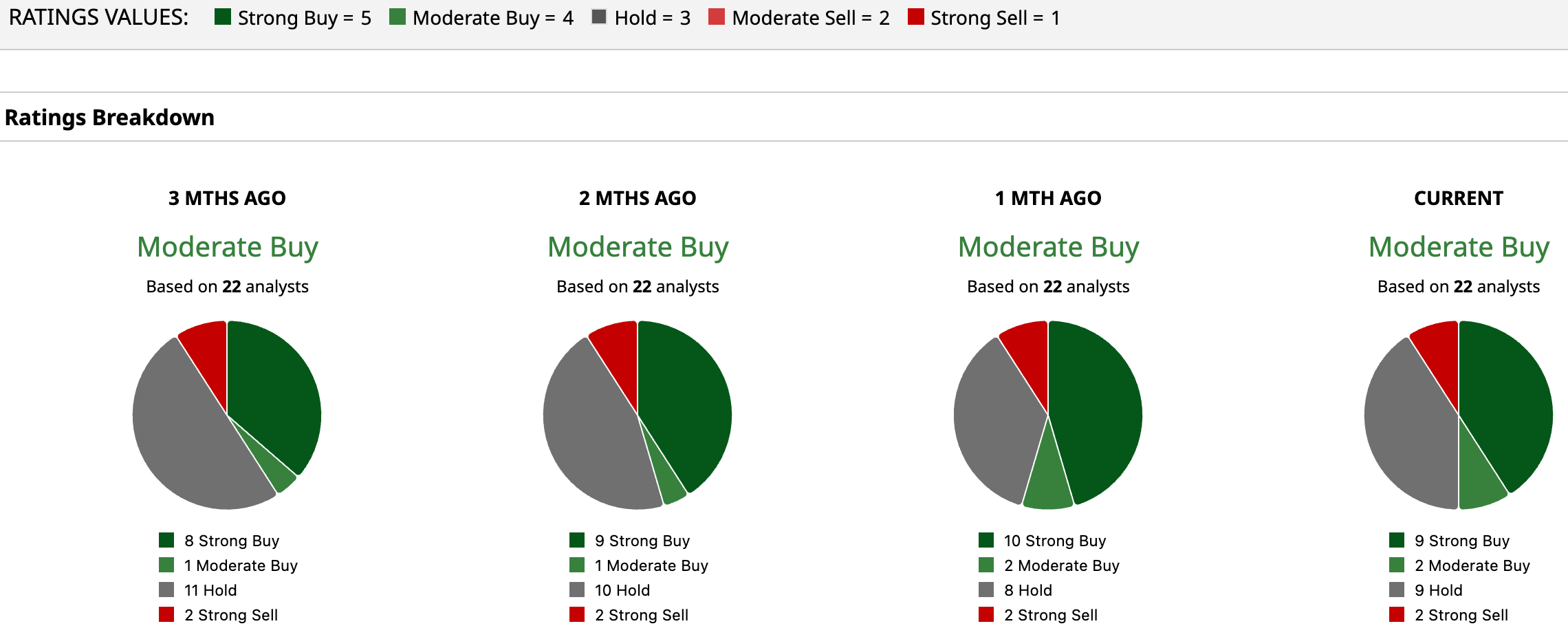

Even after the sharp pullback, Wall Street isn’t giving up on IBM. The stock still holds a consensus “Moderate Buy” rating, signaling that analysts see more opportunity than risk at current levels. Of the 22 analysts covering the company, nine rate it a “Strong Buy,” two assign a “Moderate Buy,” nine recommend “Hold,” and only two call it a “Strong Sell.” While opinions are mixed, bullish voices still outnumber the bears.

The upside potential is what really stands out. The average price target of $320.38 implies a possible 38.7% rebound from here. And at the high end, the Street’s most optimistic target of $380 suggests IBM shares could climb as much as 64.5% if momentum turns in its favor.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Claude Just Dealt Another Blow to IBM Stock. Will It Be Fatal, or Should You Buy the Dip?

- 3% Yield and 93% Upside: This Dividend Stock Could Offer a Lifetime of Income

- As Walmart Raises Its Dividend 5%, Should You Buy WMT Stock?

- These 3 Dividend Aristocrats Look Ready to Rebound in 2026. Should You Buy Them Now?