Nvidia (NVDA) will release its fourth-quarter financial results on Wednesday, Feb. 25. The chipmaker has a strong track record of revenue and earnings growth, driven by surging demand for its artificial intelligence (AI) accelerators. As hyperscalers and enterprises continue ramping up investment in AI infrastructure, Nvidia has remained a primary beneficiary of that capital expenditure cycle.

While the demand environment remains solid, NVDA stock looks cheap on valuation ahead of the earnings release, suggesting it could be a buying opportunity for long-term investors. Further, the stock’s 14-period Relative Strength Index (RSI) on the weekly chart stands at 57.4, comfortably below the 70 level typically associated with overbought conditions, suggesting the shares are not stretched and may still have room to climb in the near term.

The options traders are pricing in a post-earnings move of about 5.4% in NVDA stock in either direction for contracts expiring Feb. 27. That is higher than Nvidia’s average move of roughly 3.9% after earnings over the past four quarters. However, it is worth noting that Nvidia shares declined after earnings in three of the last four quarters, implying that even strong performance and solid fundamentals do not always translate into an immediate positive market reaction.

Nvidia Q4 Earnings: Here’s What to Expect

Nvidia is heading into its fourth-quarter earnings report with solid momentum, as demand for AI infrastructure remains robust. In the third quarter, the company generated $57 billion in revenue, marking a 62% increase from a year earlier and a record $10 billion sequential gain. Management indicated that demand remains exceptionally strong, with its installed base of GPUs across the Blackwell, Hopper, and Ampere architectures running at full capacity.

For the fourth quarter, Nvidia is guiding for revenue of $65 billion. This suggests 14% sequential growth, largely driven by continued strength in the Blackwell platform. Notably, the company’s outlook excludes any contribution from data center compute revenue in China.

The data center segment will continue to generate the majority of the company’s revenue. In the third quarter, the business delivered $51 billion in revenue, up 66% year-over-year (YoY). That momentum appears sustainable. Compute demand is expected to stay strong, supported by the rapid ramp-up of the GB300 series. At the same time, networking revenue could see solid expansion as cloud providers accelerate adoption of NVLink and increase deployment of Spectrum-X Ethernet and Quantum-X InfiniBand solutions.

The Blackwell architecture appears to be gaining traction faster than prior generations. The GB300 has already surpassed the GB200 and accounted for roughly two-thirds of Blackwell revenue in Q3. Shipments to major cloud service providers are underway, and the revenue contribution from Blackwell could expand further over the coming quarters as deployments scale.

Strong top-line momentum is expected to translate into substantial earnings growth. Analysts forecast fourth-quarter earnings of $1.45 per share, implying a 70% YoY increase. Notably, Nvidia has exceeded earnings expectations in three of the past four quarters.

Is NVDA Stock Too Cheap Ahead of Earnings?

While Nvidia is witnessing strong demand and its growth outlook remains solid, its stock is trading at an attractive forward multiple. NVDA stock trades at about 26.7 times forward earnings, which is low given its significant earnings growth potential. Analysts are projecting earnings growth of roughly 58.3% in fiscal 2027, indicating that the stock should command a higher multiple.

Overall, secular tailwinds and its low valuation indicate that NVDA stock is too cheap to ignore.

Is Nvidia Stock a Buy Ahead of Q4 Earnings?

Nvidia’s Q4 earnings report will reflect strong operating momentum. Its revenue and EPS are likely to grow at exceptional rates, driven by sustained demand for AI infrastructure and the rapid adoption of Blackwell. Moreover, with valuation looking compelling relative to its growth profile, NVDA’s risk-reward profile remains favorable heading into Q4.

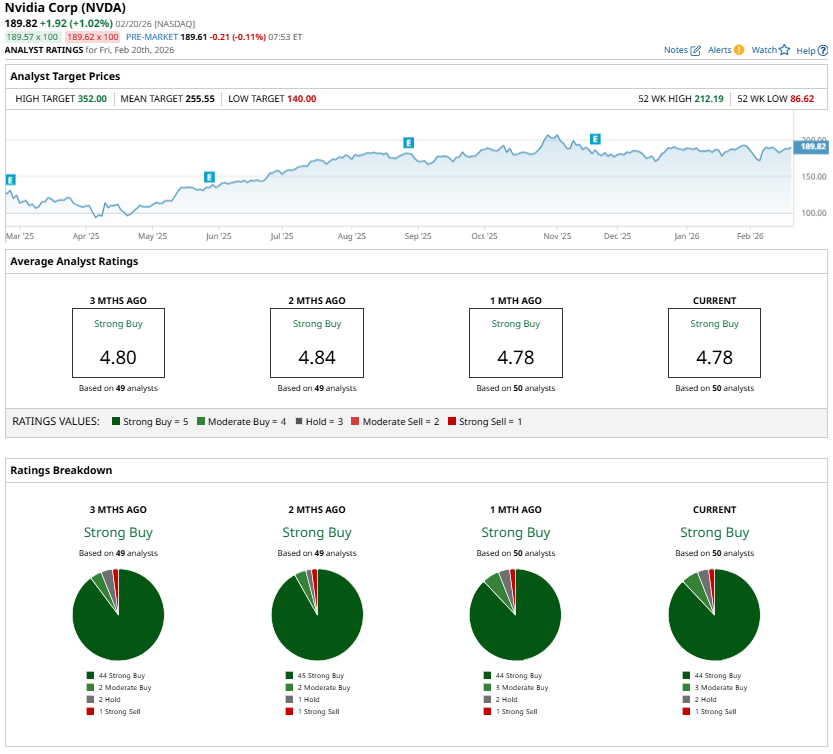

Wall Street analysts are bullish on NVDA and maintain a “Strong Buy” consensus rating ahead of earnings.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart