Trade uncertainty is back on the table after the U.S. Supreme Court struck down the bulk of President Donald Trump’s tariffs. The president responded by imposing a global tariff of 10%, which he subsequently raised to 15%. There have been reactions globally, and the European Commission has called upon the U.S. to honor the deal previously negotiated, while India has delayed trade talks in light of the new developments.

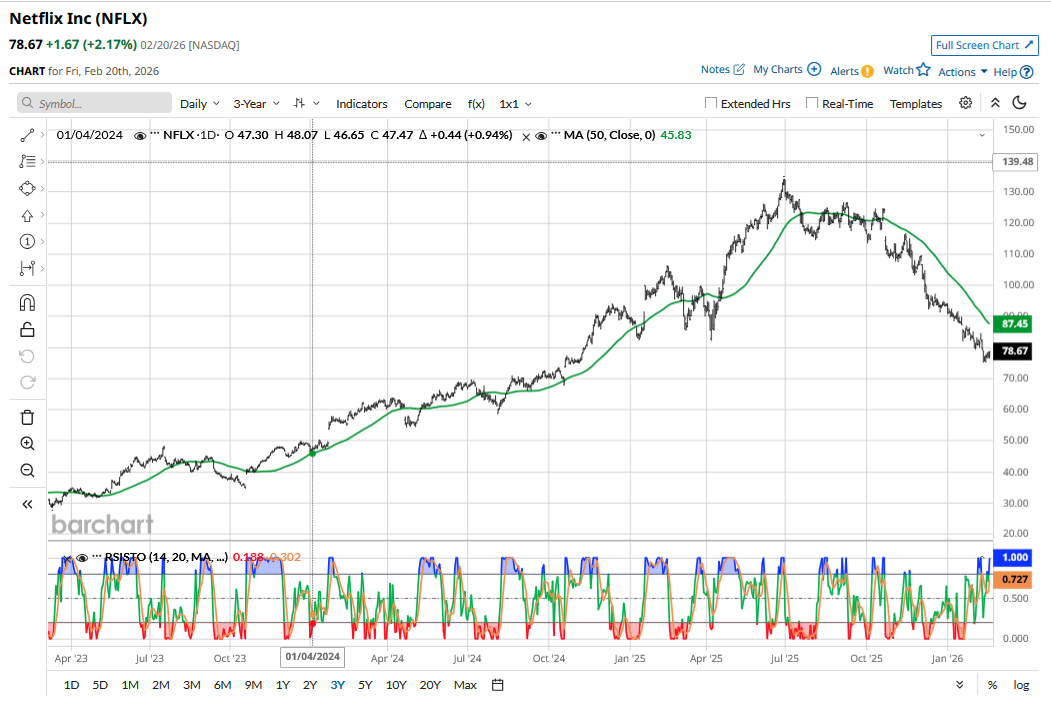

Netflix's (NFLX) stock outperformed markets in the first half of 2025 as investors saw it as a bastion of safety amid the trade uncertainty. With trade uncertainty once again back on the table and artificial intelligence (AI) bubble fears haunting investors, could NFLX—which is down over 41% from the record highs it hit in June 2025—regain favor with markets? Let’s explore.

Trade Uncertainty Is Back, But It Is Not As Severe

To begin with, the current trade uncertainty is not as severe as last year, and the 15% tariff would appear a lot more benign compared to the “Liberation Day” tariffs that Trump announced in April 2025. Moreover, markets have found a way to live with Trump’s rhetoric on the assumption that the president would eventually mellow down the rhetoric. However, names like Netflix could outperform if the trade uncertainty were to increase any further.

Netflix Is Firing on All Cylinders

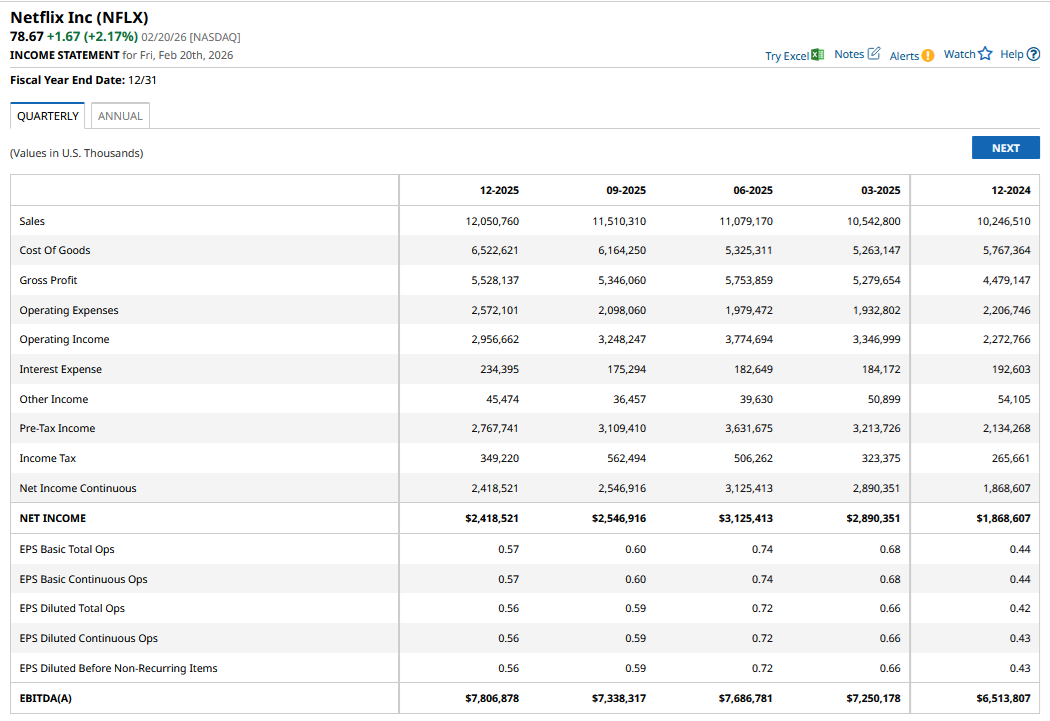

Netflix's business continues to do well, and the company added 23 million subscribers last year. While it is well below the 2024 and 2025 numbers, when it saw a bump in new members following the password sharing crackdown and launch of the ad-supported tier, it is still quite a healthy number. Streaming peers, particularly Disney (DIS), have been struggling to add new subscribers, and by continuing to grow its subscription base in high double digits, Netflix has yet again established itself as the undisputed king of streaming.

Netflix’s ad business continues to grow well, and revenues rose over 2.5x to $1.5 billion last year. The company expects revenues to “roughly double” this year as it capitalizes on a growing subscription base on the ad-supported tier.

Netflix’s operating margins expanded by 3 percentage points to 29.5% last year, and the company expects them to rise to 31.5% this year. Netflix expects its margins to keep expanding every year, which is not an unreasonable expectation, as it aims to keep content spending growth below the revenue growth.

The streaming industry has high operating leverage, as the content and technology costs are largely fixed. The cost to create new content is also agnostic of subscriber base, even as a rising global subscriber base would warrant higher content spending to retain members and attract new ones. The attributes are similar to the software industry, where incremental revenues largely flow to the gross profit level.

Netflix Stock Looks Attractive

From a valuation perspective, Netflix trades at a forward price-to-earnings (P/E) multiple of under 25x, which is quite attractive considering the kind of top- and bottom-line growth the company brings to the table. Moreover, even as Big Tech companies are staring at a tsunami of depreciation arising out of their burgeoning capex towards building AI infrastructure, Netflix’s earnings growth is expected to stay buoyant, with consensus estimates calling for over 20% growth in 2026 and 2027. I believe the estimates might be a bit conservative, looking at the expected revenue growth and margin expansion.

NFLX Stock Forecast

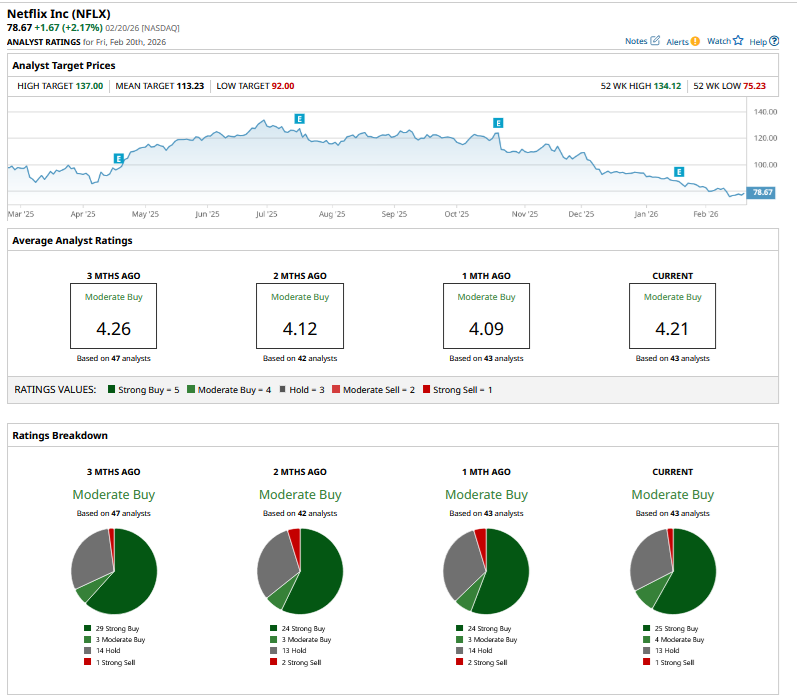

Sell-side analysts also see significant upside in NFLX stock, with its mean target price of $113.23 implying a potential upside of nearly 44%. The stock even trades below the Street-low target price of $92, while the Street-high target price of $137 is over 74% higher. While several brokerages lowered NFLX’s target price following the Q4 2025 confessional in January, Philips Securities upgraded it to a “Moderate Buy” later in the month while raising its target price from $95 to $100.

Key Risk That NFLX Investors Should Watch Out For

Meanwhile, the key risk that Netflix investors should watch out for is the bidding war for Warner Bros. Discovery (WBD). Netflix has sweetened its offer by making it all-cash, and it may need to offer an even higher price if Paramount Skydance Corporation (PSKY) further raises its offer, as the timeline for its “best and final” offer expires today. A bidding war for WBD’s assets would be the last thing Netflix investors would want, as the stock has been under pressure since the company announced the deal last year.

If the all-cash offer were to take place, it would mean Netflix raising an enormous amount of debt, which would put pressure on its free cash flows in the short term. The company has already discontinued its share repurchase plan and might need to get frugal with future content spending as debt servicing costs rise.

Or the Department of Justice (DOJ) could simply tank the entire deal.

All said, I find NFLX stock quite attractive irrespective of whether the company gets to buy WBD’s assets. The risk-reward is looking quite favorable, especially for those who can digest the interim volatility as the noise over the WBD deal persists.

On the date of publication, Mohit Oberoi had a position in: NFLX , DIS . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart