CoreWeave (CRWV) will release its fourth quarter financial results on Thursday, Feb. 26. Investor enthusiasm has been building ahead of the earnings release. CoreWeave’s stock has climbed approximately 25% year-to-date (YTD), reflecting optimism around sustained AI infrastructure spending and the company’s expanding capacity footprint.

The company specializes in cloud infrastructure optimized for accelerated computing, supplying enterprises and leading artificial intelligence (AI) research labs with the high-performance GPUs, CPUs, advanced networking, and scalable storage required to train and deploy next-generation models.

As hyperscalers and AI developers race to secure computing power, demand for high-density GPU clusters remains robust, positioning CoreWeave as a key supplier in a constrained market.

With additional infrastructure capacity coming online and customer demand continuing to accelerate, CoreWeave is well-positioned to deliver strong revenue performance in Q4 and the quarters ahead. More importantly, management’s commentary on backlog, utilization rates, and forward guidance for calendar year 2026 will likely shape the next leg of the stock’s trajectory.

While the demand environment for CoreWeave remains solid, the stock’s 14-period Relative Strength Index (RSI) on the daily chart stands at 47.9, comfortably below the 70 level typically associated with overbought conditions. This suggests that the shares have room to appreciate if its Q4 financials and forward guidance beat expectations.

CoreWeave’s Q4: Here’s What to Expect

CoreWeave is in a solid growth phase, and the momentum is likely to be reflected in its Q4 results. The underlying drivers of growth, including the AI infrastructure demand, GPU scarcity, and enterprise adoption of accelerated computing, remain firmly intact, and the company’s order book suggests that momentum is unlikely to moderate soon.

At the end of the third quarter, CoreWeave reported a revenue backlog of $55.6 billion, nearly doubling from the previous quarter. That figure is poised to climb again as demand for Nvidia’s Blackwell platform and other GPU offerings across its portfolio remains strong. Importantly, the company has not relied solely on next-generation hardware to fuel growth. In Q3, it secured multiple agreements for prior-generation GPUs, onboarding new customers while recontracting existing capacity. This demonstrates both the depth of demand and CoreWeave’s ability to monetize assets across product cycles.

Importantly, CoreWeave has meaningfully reduced customer concentration risk over the course of the year. Earlier in the year, a single customer accounted for roughly 85% of revenue backlog. By Q2, that figure had fallen to around 50%, and by Q3, no individual customer represented more than approximately 35%.

In parallel, over 60% of the backlog now represents investment-grade counterparties. This shift materially lowers counterparty risk and strengthens the durability of forward cash flows. It also indicates that CoreWeave’s services are being adopted across a wider mix of enterprises.

Notably, the number of customers generating more than $100 million in trailing twelve-month revenue tripled year-over-year (YoY) in Q3.

While the company is witnessing strong demand, there are, however, near-term operational considerations. Temporary delays associated with a third-party data center developer may moderate the pace of Q4 revenue growth. Management has indicated that these delays do not affect backlog or the ultimate value of contracted revenue, but they could shift the timing of recognition.

At the same time, CoreWeave said earlier that it will bring online some of its largest deployments to date during Q4. These large-scale rollouts will pressure adjusted operating margins in the near term. Further, higher debt levels used to finance demand-driven capital expenditures could impact its bottom line.

The Bottom Line on CRWV Stock

CoreWeave’s Q4 will reflect solid ongoing momentum in its business. A $55.6 billion backlog, improved customer diversification, and a higher proportion of investment-grade counterparties materially enhance revenue durability and reduce counterparty risk. Further, the tripling of $100 million-plus customers reflects that adoption is broadening beyond early anchor clients.

Notably, the uptrend in CRWV stock ahead of earnings indicates that investors are already discounting continued strength in AI-driven compute demand. However, near-term variables, including deployment-related margin pressure, revenue timing shifts from data center delays, and elevated leverage, introduce earnings volatility risk.

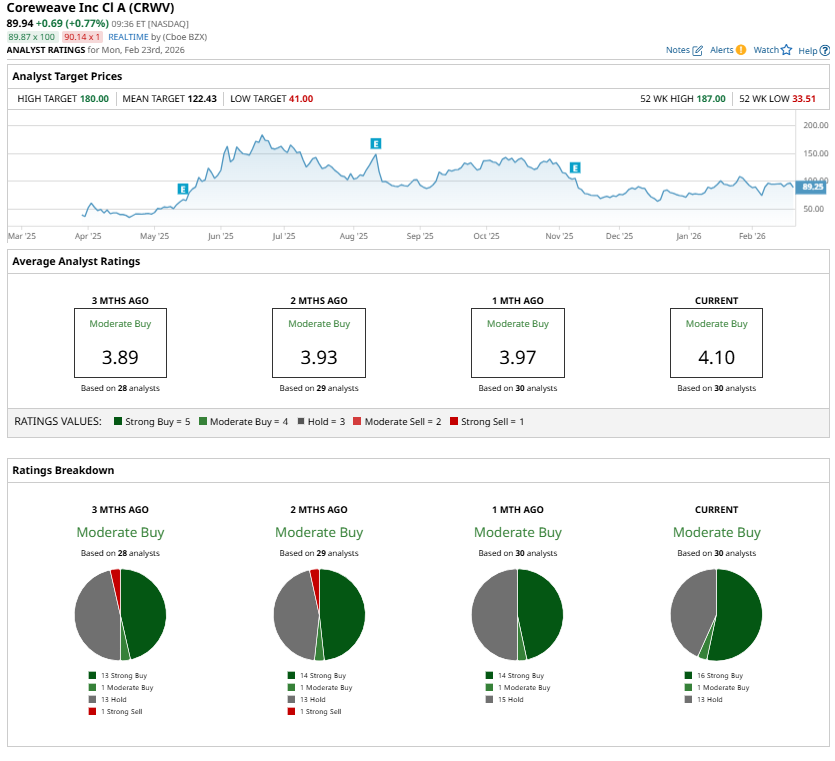

With the analysts maintaining a “Moderate Buy” consensus rating ahead of earnings, long-term investors may consider holding or selectively accumulating CRWV stock on weakness.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart