The Stamford, Connecticut-based United Rentals, Inc. (URI) is a global force in the equipment rental arena. With a market cap of approximately $57.3 billion, the company supplies construction machinery, aerial platforms, power and climate systems, trench safety solutions, and modular spaces.

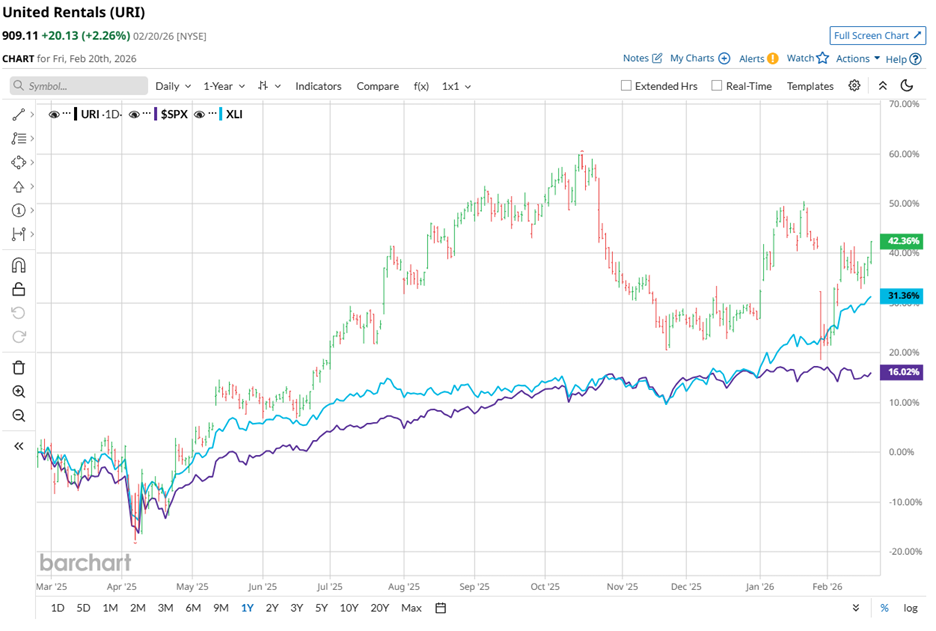

United Rentals has outpaced the broader market, reinforcing its relative strength. Over the past 52 weeks, URI stock has climbed 30.9%, and it added another 12.3% year-to-date (YTD). In contrast, the S&P 500 Index ($SPX) has risen nearly 13% over the same period and posted only a marginal uptick YTD.

A broader sector comparison adds a useful perspective. The State Street Industrial Select Sector SPDR ETF (XLI) has advanced 28.6% over the last 52 weeks, trailing URI’s stronger 30.9% gain. YTD, however, the ETF has risen 14.3%, placing it just ahead of URI’s 12.3% increase.

On Feb. 4, United Rentals rallied nearly 7% intraday after announcing the appointment of Alexander Taussig to its board of directors, effective immediately. Taussig, a Board Partner at Lightspeed Venture Partners, brings seasoned expertise in venture capital and corporate strategy.

His appointment meaningfully strengthens the board’s ability to scale technology-enabled platforms, including artificial intelligence (AI). With sharper strategic oversight, United Rentals can accelerate digital transformation, refine innovation initiatives, and convert technological investments into measurable competitive advantage.

Analysts project solid earnings momentum ahead. For fiscal year 2026, which ends in December, they expect diluted EPS to climb 11.5% year over year to $46.88. One thing to note is that United Rentals has missed EPS estimates in three of the past four quarters and surpassed expectations only once.

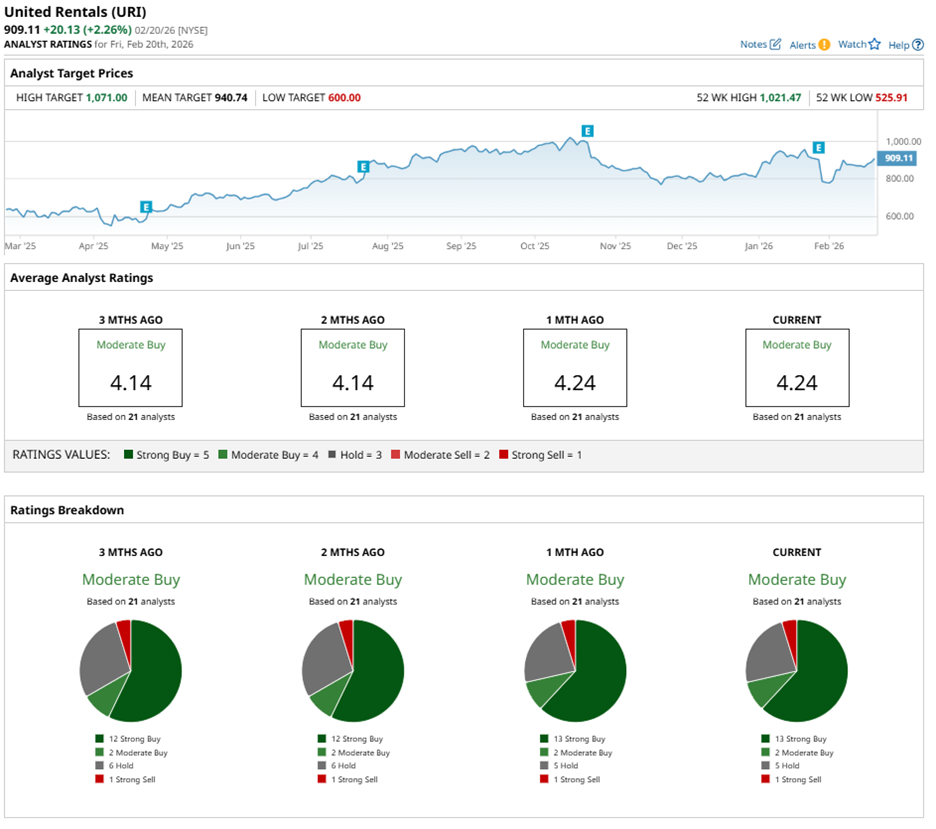

Wall Street nevertheless maintains a favorable stance. Analysts have assigned URI stock an overall “Moderate Buy” rating. Of 21 analysts covering the stock, 13 recommend “Strong Buy,” two suggest “Moderate Buy,” five advise “Hold,” and one issues a “Strong Sell.”

Notably, the current analyst sentiment has strengthened from three months ago, when 12 analysts carried “Strong Buy” ratings.

Even as analysts trim price targets, they have not abandoned conviction. On Feb. 2, Citigroup Inc.’s (C) Kyle Menges maintained a “Buy” rating but reduced his target from $1,090 to $950. On Jan. 30, JPMorgan’s Tami Zakaria reiterated an “Overweight” rating while lowering her target from $1,150 to $970.

Importantly, targets still point higher. The mean price target of $940.74 implies potential upside of 3.5%, while the Street-high target of $1,071 represents a gain of 17.8% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart