Value-focused investors often track what Warren Buffett and his firm, Berkshire Hathaway (BRK.A) (BRK.B), buy and hold. Even as Buffett passes his CEO hat to Greg Abel, his legacy endures (and he remains chairman). So, when Berkshire leans in, it usually signals confidence in businesses that generate steady cash and can ride out economic cycles.

In Q4, Berkshire added to three distinct positions: Domino's Pizza (DPZ), Chevron (CVX), and Chubb (CB). The filing shows Domino’s rising to about 3.35 million shares from 2.98 million, Chevron growing to roughly 130.2 million shares from 122.1 million, and Chubb expanding to 34.3 million shares from 31.3 million.

Taken together, these buys underline a simple thesis that durable consumer demand, predictable energy cash flows, and underwriting float with pricing power offer a balanced way for Berkshire to deploy capital, and for long-term investors, a useful list to examine more closely.

Berkshire Stock #1: Domino’s Pizza (DPZ)

Berkshire Hathaway added significantly to Domino’s Pizza in Q4. The investment firm clearly values the pizza chain’s resilient cash flow and global franchise model. Domino’s, with 20,000-plus stores and royalty-based revenues, fits Buffett's value and dividend style. It offers a modest yield of 1.9% and steady franchise economics.

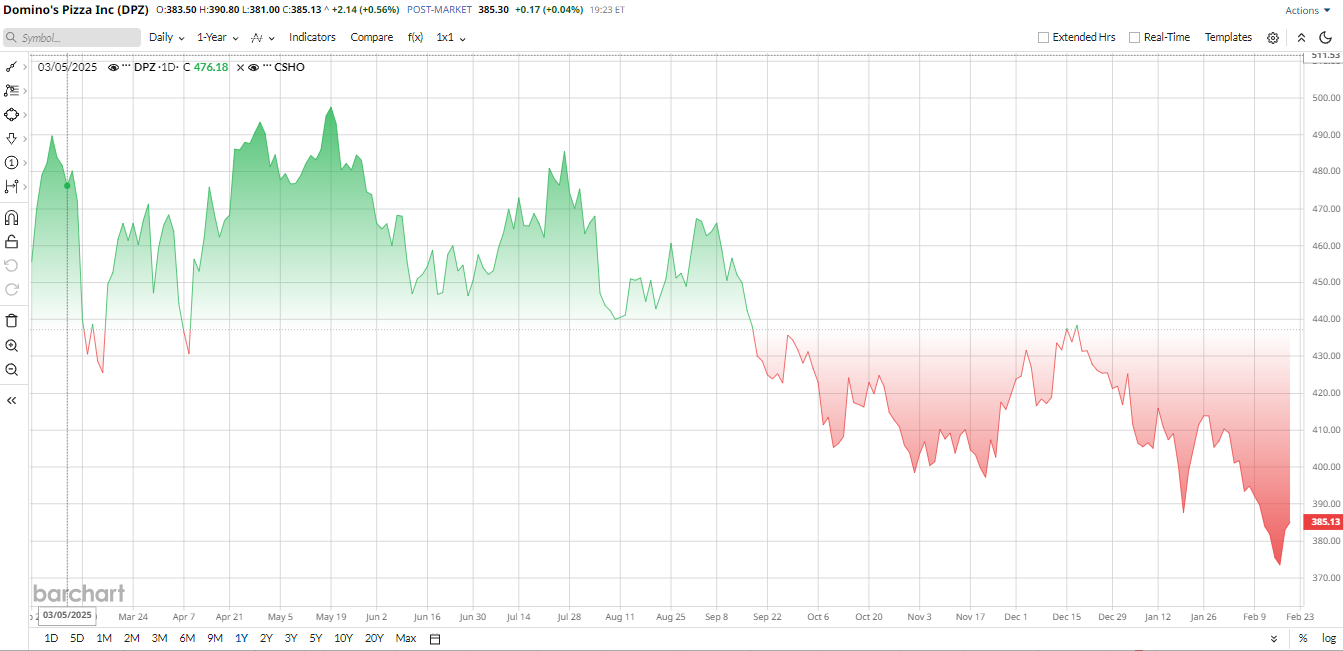

DPZ stock has underperformed the market, down about 19% over the past year. Weakening same-store sales momentum, especially in the U.S., and rising input costs for franchisees have dragged performance. Analysts cite softer consumer spending and intense competition as headwinds.

Valuation is rich for a quick-service restaurant. Domino’s trades around 22× trailing EPS. That forward P/E is higher than many peers, implying investors expect growth to improve. In other words, Berkshire’s stake hike suggests the firm is banking on an earnings rebound rather than a fire-sale valuation today.

In Q3 fiscal 2025, Domino’s delivered revenue of $1.14 billion, up 6.2% year-over-year (YoY). Net income reached $139.3 million, translating to earnings per share of $4.08. Even more telling, global same-store sales climbed 5%, with U.S. comps up a solid 5.2% and international growth of 1.7%.

Management highlighted strong franchisee economics and ongoing digital investments as key drivers. New menu innovations, including stuffed-crust pizza offerings, and loyalty program enhancements aim to keep traffic steady and boost repeat orders. Despite inflationary pressures, disciplined cost controls helped margins remain stable.

Moreover, Domino’s is actively innovating. It’s expanding digital ordering, upgrading its loyalty program, and experimenting with new menu items and promotions. These initiatives, part of its “Hungry for More” growth plan, aim to boost market share. Berkshire’s recent purchase suggests it sees these catalysts, along with a loyal customer base, driving a turnaround.

Analysts forecast a moderate rebound next quarter, pending 23 Feb. Consensus is for Q4 revenue of $1.52 billion, 10% YoY growth, and EPS of $5.36 vs $4.89 last year. That reflects the expected pickup in delivery volume and pricing. Overall, Street estimates imply low single-digit same-store sales growth and slight EPS gains.

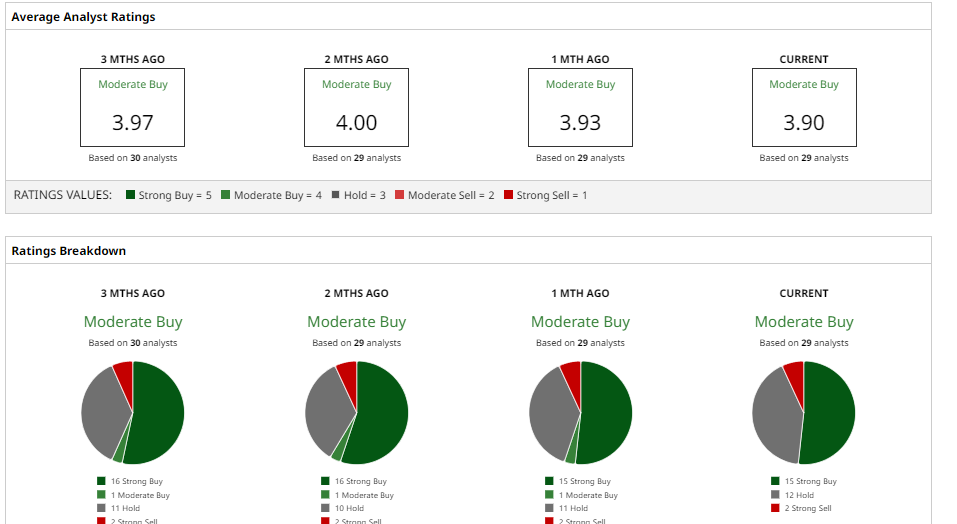

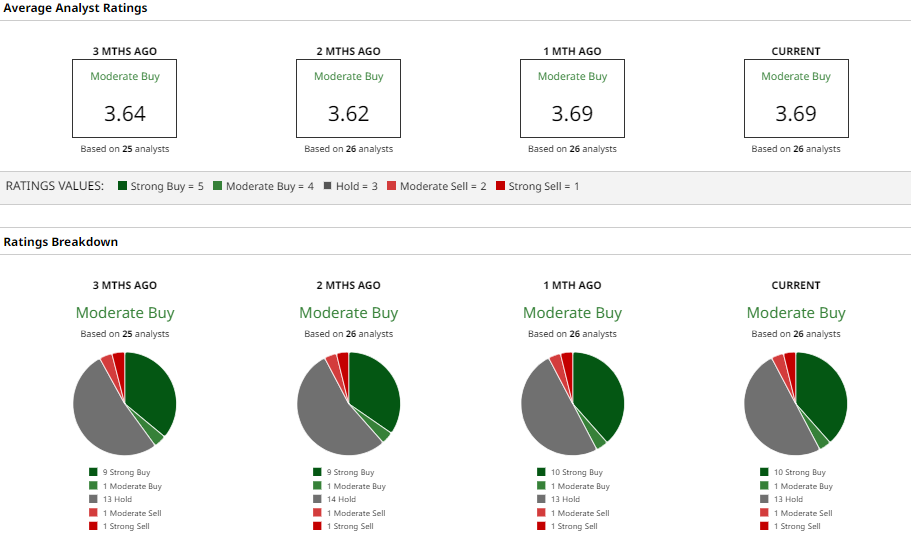

Wall Street is cautiously optimistic. Barchart data shows a “Moderate Buy” consensus on DPZ, with a mean price target of $486.76, roughly 27% above the current stock price. If Domino’s meets expectations, that implies room for further upside.

Berkshire Stock #2: Chevron Corporation (CVX)

Chevron Corporation is a core Buffett energy pick. Berkshire boosted its CVX holding in Q4, reflecting faith in the oil major’s cash flow and dividend. Chevron’s integrated business and low leverage fit Buffett’s criteria. The stock offers a 3.8% yield, making it attractive to dividend-seeking investors.

Over the past year, CVX has outperformed the booming S&P 500 ($SPX). It’s up 17% over 52 weeks vs. the S&P's 12% gain. Also, on a year-to-date (YTD) basis, it’s up 21%, easily outpacing the index. Volatile oil prices explain much of this, as Q4 2025 profit fell as crude prices dipped, though production rose due to the Hess acquisition.

Chevron’s valuation is reasonable for its sector. The stock trades around 16× forward EPS. That forward P/E is in line with peers and lower than some tech stocks Buffett holds. The ratio suggests investors expect stable earnings growth. In fact, analysts project CVX earnings will jump 17% in FY2026 to $12.59 per share from $10.79 last year. The dividend was recently raised by 4%, reinforcing Chevron’s income appeal.

In Q4 2025, Chevron reported adjusted EPS of $1.52, ahead of the $1.44 consensus but down from $2.06 a year ago due to lower oil prices. Upstream production was a record 4 million barrels of oil equivalent per day, boosted by Hess, and downstream margins improved, with a loss in the prior year turning into an $823 million profit. Chevron reiterated disciplined capital spending. It returned a record $27 billion to shareholders in 2025, $12.8 billion in dividends, and $12.1 billion in buybacks, signaling strong free cash flow.

Chevron is pursuing growth catalysts. It won new oil blocks off Greece and is expanding exploration in Libya. Notably, after the U.S. eased Venezuela sanctions, Chevron said it could double its oil output there within 18 to 24 months. Meanwhile, it plans to ramp up Guyana and Permian production. These projects, plus steady refining profits, are expected to support near-term earnings. Berkshire’s bullish stance suggests it expects higher long-term demand and cash returns.

Wall Street is quite bullish on CVX. Barchart shows a “Strong Buy” consensus, with a mean price target of $177.4, which offers about 13.5% upside from today’s level. For Buffett-style investors, Chevron still looks like a value play, high dividend plus growth from global energy demand, even if near-term results are choppy.

Berkshire Stock #3: Chubb Limited (CB)

Chubb Limited is a global insurance powerhouse where Buffett has long held a position. Berkshire increased its Chubb stake to 8.5% in Q4. Chubb’s conservative underwriting and underwriting profits make it a classic Buffett insurance pick. It pays a steady dividend yield of 1.2% and has returned substantial cash via buybacks.

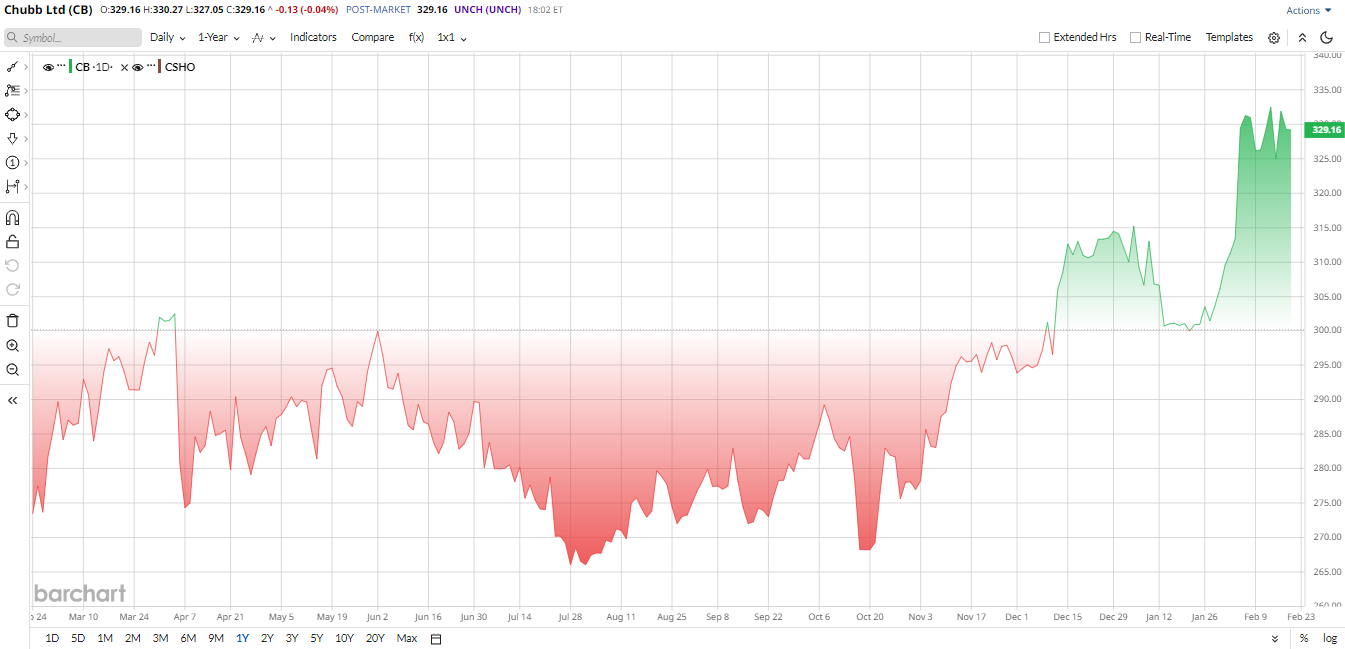

CB stock outperformed the market last year, up about 23% over 52 weeks. Favorable premium pricing, lower catastrophe losses, and strong investment returns drove this gain. On a YTD basis, Chubb is up 5%, again beating the broader market, which is trading nearly flat. In short, solid Q4 results and a strong balance sheet have lifted the shares.

Chubb’s valuation is reasonable. Forward P/E is only in the low teens, around 12× forward EPS, reflecting its steady growth outlook. The stock’s yield is modest, but Chubb offers consistent dividend growth and buybacks. In “Buffett terms,” Chubb trades more like a growth stock, implying confidence in future earnings.

In Q4 2025, Chubb reported record profits. Core operating EPS was $7.52, up 25% from $6.02 a year prior. Net income was $3.2 billion, up 25% YoY, fueled by higher investment income and fewer catastrophe claims. The insurer saw investment income climb to $1.69 billion and catastrophe losses drop sharply to $365 million. Premiums rose 8.9% across P&C and life, with combined ratios holding in the low 80s. Disciplined underwriting and steady risk management fueled the earnings jump, keeping Chubb in Buffett-friendly territory.

Besides strong earnings, Chubb is expanding its global footprint. It recently boosted its stake in Chinese insurer Huatai and launched a digital life insurance partnership with Brazil’s Nubank. These moves tap high-growth markets, diversifying beyond mature U.S. operations. Management also highlighted success in Speciality lines and Accident & Health segments. Berkshire’s buying itself is a catalyst, so the firm clearly trusts Chubb’s plan and sees value in its global expansion and capital allocation.

Analysts are upbeat on Chubb’s next quarter. For Q1 2026, the consensus forecast is core EPS $6.48, compared to $3.68 a year ago, a massive 76% jump. For context, last year’s Q1 was unusually soft, so this compares to a tougher comp.

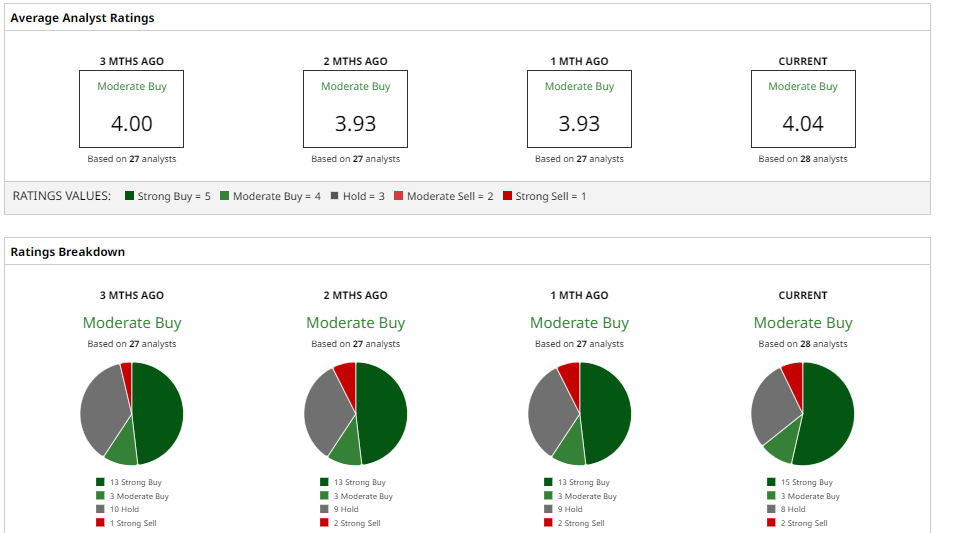

Wall Street consensus on Chubb is “Moderate Buy.” The mean target price is $338, roughly flat to current levels, implying little upside from here. However, the high target is $385, which still gives room for the stock to grow about 15.8%. Analysts see only modest gains in the stock, since much of Chubb’s improvements are already priced in. Buffett’s involvement, however, underscores Chubb’s qualities, which are a proven franchise with reliable growth, making it an attractive holding for value investors despite the modest near-term upside.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Nvidia May Have Dumped Arm Stock in Q4, But Should You Buy Shares Now?

- 3 New Stocks Billionaire Dan Loeb Is Betting on Now

- This Penny Stock Is Building a Strategic Silver Reserve. Should You Buy Shares Now to Bet on a Run in Silver Prices?

- 3 Stocks Warren Buffett and Berkshire Were Gobbling Up in Q4